We believe in paying our “fair share” of tax and understand that tax evasion is illegal. However, we should always make sure that we’re not overpaying our taxes. Hopefully, the following analysis will show you how to avoid capital gains tax on property in the UK that you shouldn’t be paying if you plan properly.

Most of us will know the ins and outs of income tax as we all pay this on a regular basis through PAYE. However, “capital gains tax” is a lesser known tax which may impact those people investing outside of tax-wrapped investments. Avoiding capital gains tax through legal channels and appropriate planning is positively encouraged (even by the tax-man) and we’ll show you how.

What Is Capital Gains Tax?

Before we look at how to avoid capital gains tax on property in the UK, we need to make sure we understand exactly what capital gains tax is. I’ll let the HMRC do the talking here.

Capital Gains Tax is a tax on the profit or gain you make when you sell or ‘dispose of’ an asset.

It was first introduced in 1965 by the chancellor James Callaghan to stop people avoiding income tax by switching their income to capital gains.

When Do I Pay Capital Gains Tax?

You pay capital gains tax when you dispose on an asset, which is defined as being as soon as you cease to own it, including the following examples:

- sell it

- give it away

- transfer it to someone else

- exchange it for something else

- receive compensation for it – for example you receive an insurance payout when an asset has been destroyed

It’s the gain you make (simply the sales price less the purchased price) – not the amount of money you receive for the asset – that is taxed.

What Are The Capital Gains Tax Rates?

The first way how to avoid capital gains tax is to make sure you are maximising the “Annual Exempt Amount”. This means that the first £11,000 in the 2014/15 tax year (increasing to £11,100 in the 2015/16 tax year) of gains will not be taxed.

Basic rate income tax payers shall then pay capital gains tax of 18% on any capital gains over £11,100, with higher rate income tax payers paying 28%. See the section at the bottom of this article to show how this has changed as a result of the 2016 budget.

Capital Gains Tax Example

You bought some shares for £2,500 in June 1992. You sell them for £22,500 in May 2013.

You’ve made a gain of £20,000 (£22,500 less £2,500), which is subject to capital gains tax.

Therefore, the first £11,100 would be tax free, and you would have a taxable gain of £8,900. Assuming you are a basic tax rate payer, your capital gains tax bill would be £8,900 x 18% = £1,602.

How To Avoid Capital Gains Tax On Stock Market Investments

It is extremely important to understand the ways to completely avoid capital gains tax. In the UK, there are two significant ways to protect your investment returns (both capital gains and income from dividends) from tax.

The first of these is an ISA and the second is a pension/SIPP. Both of these options protect your investment returns from capital gains taxes, but in different ways.

Rather than going into too much detail in this post, I would recommend that you read the following to understand the tax benefits of these two tax wrappers:

Related Article: ISA vs Pensions (Moneystepper)

How To Avoid Capital Gains Tax On Property

However, most people run into problems when they try to avoid capital gains tax on property. Currently, residential property cannot be held in either an ISA or a pension. Therefore, it is not possible to wrap the investments from tax in this manner, making avoiding capital gains tax a little more complex.

However, there are still certain rules and regulations that we can take advantage of to help us avoid capital gains tax.

Firstly, it is important to understand that you should never pay capital gains tax on the sale of your own residential property. For many people, this is the most common cause of a significant capital gain, and hence this relief will be very welcome.

For buy-to-let property, your tax bill can be greatly reduced if you have lived in the property yourself. This is called PPR (Principal Private Residence) relief and it is applicable where you can prove that a sold property was, at any point during ownership, your home.

Essentially, the “final” 3 years (36 months) always qualify for relief. This applies even if you weren’t living there during the final 3 years. Instead, the rule is that the property must have been your only or main home at some point during the time that you’ve owned it.

You actually then can claim PPR relief on the actual time you were living in the property, plus the additional 3 years.

Unfortunately, in his autumn 2013 statement, the Chancellor announced that from 2014-15 this final period relief will only apply to the final 18 months of ownership. There will be an exception for people who are disabled or in long-term care. This measure became law in 2014.

How To Avoid Capital Gains Tax Through Letting Relief

Additionally, many landlords will also be able to claim letting relief when they sell their buy-to-let property.

The maximum amount of Letting Relief due is the lower of:

- £40,000,

- the amount of Private Residence Relief due, or

- the amount of gain you’ve made on the let part of the property

This relief can then be placed against any of your gains and you will not be required to pay capital gains tax on this amount.

How To Avoid Capital Gains Tax On Property UK – An Example

To bring all of these items together and give us a wider appreciation of how to aviod capital gains tax on property in the UK, an example will come in handy.

Say you bought a property in 2004 for £100,000, which you lived in until 2006. You then rented this property out until 2014, when you sold the property for £220,000.

Your capital gains initially seems like it will be payable on £120,000, which for the higher rate tax payer would lead to a bill of £33,600.

However, firstly we know that we can benefit from PPR. We owned the property for 10 years, so 1.5/10 of our gains are excused (as per the new guidance). However, we also get the time that we actually lived in the property tax free as well. Therefore, our 2 years living and extra 1.5 years PPR are tax free (3.5 years in total).

In this scenario, the total PPR would be £42,000 and the taxable gain would be the remaining £78,000.

Then, letting relief will also be available for another £40,000.

Therefore, our new taxable amount is £120,000 – £42,000 – £40,000 = £38,000.

After removing your annual exempt amount of £11,100, there would only be capital gains to pay on £26,900 under the new rules), meaning a final tax bill of only £7,532.

By understanding the tax exemptions available; we have completely legally and ethically avoided over £26k in capitals gains tax!

But, there are yet more ways that you can avoid capital gains tax on property in the UK…

Extra Tips To Avoid Capital Gains Tax – The Power Of Partnership

Each person owning any property can claim both letting relief and place their annual allowance against the sale.

Spouses can only use both partners’ reliefs and annual exempt amounts if they both own the property. Therefore, if you have a property which is solely held by one partner, it may save you thousands by gifting half of the property to the other spouse before selling.

As long as the property transfer is a “gift” – i.e. that there is no money changing hands and no change in who is liable for the mortgage – there will be no capital gains tax due on the gift between the spouses. Then, when the property is sold to a third party, the reliefs available will be much more generous.

Therefore, in the above example, if a husband and wife had bought and sold the property jointly, the taxable amount before annual exempt amounts would have been:

Gross gain £120,000

PPR relief (£42,000)

Husband letting relief (£40,000)

Wife letting relief (£38,000)

Taxable gain £0

Note that the wife could have used up to £40k letting relief as well, but this was not required. Additionally, if a taxable gain is due before annual exempt amounts, both the husband and wife can apply their annual exempt amounts to this gain.

For example, under the same example, with the only difference being a sales price of £260,000:

Gross gain £160,000

PPR relief (£56,000)

Husband letting relief (£40,000)

Wife letting relief (£40,000)

Taxable gain £24,000

Husband’s annual exempt amount (£11,100)

Wife’s annual exempt amount (£11,100)

Final taxable gain £1,800

Therefore, despite us starting with a taxable gain of £160,000. we actually only pay capital gains tax on a measly £1,800, which for a basic rate payer at 18% would amount to £324.

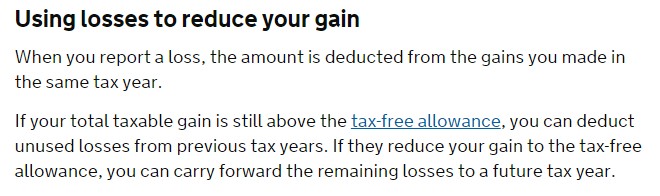

Extra Tips To Avoid Capital Gains Tax – Capital Losses

Whilst you are taxed on capital gains, it is also worth noting that you can “store up” any losses you make to place against future capital gains:

For instance, if I bought a share for £10,000 in 2012 and it went into administration in 2014 and I received nothing back, I would have a £10,000 capital loss.

If in 2016, I sold a property for a gain of £25,000, I could then use this previous loss to reduce my capital gain by £10,000.

Always remember to use your Annual Exempt Amount before using any brought forward capital losses from prior periods.

For example, if you have a gain of £10,000 in the current year, you are covered by the annual exempt amount and therefore would not pay any tax. Therefore, you should not use any of your prior year losses.

Equally, if you have a gain of £15,000 in the current year (and £10,000 losses carried forward), you would only want to use £3,900 of your prior year losses to reduce your capital gains down to the tax free amount of £11,100.

What Rate Do You Pay For Capital Gains Tax?

After using your reliefs and allowance, the tax rate which you apply to your taxable gain can be a little tricky to work out. Effectively, the easiest way is to think of it as follows:

- Take you current income for the tax year (the amount on which you pay income tax) and subtract it from the high end of the “basic rate tax level”. For the 2015-16 tax year (see the government website for latest figures), this figure is £31,785.

- If the remaining figure is positive, you pay 18% tax on your capital gains up to that amount, and then 28% on the remaining capital gains.

- If the remaining figure is negative, you pay 28% on all of your taxable capital gains.

See the section below to see how this will change as a result of the 2016 budget.

Back to an example. In the latest example above, the remaining taxable capital gain after reliefs and allowances was £1,800. If in this example your taxable income (your salary) was £31,000 per annum, then you would follow the steps above:

- Take the current income of £31,000 away from the high end of the basic rate tax band (£31,785) to give £785.

- The remaining figure is positive and so you would pay 18% on the £785, and 28% on the remaining gain of £1,800 less £785, which is £1,015. Therefore, the tax bill would be £425.50 (18% x £785 + 28% x £1015).

- Not applicable.

Changes to Capital Gains Tax Rates in the 2016 Budget

In the 2016 budget, Mr Osborne has altered the rates of capital gains tax for capital sales made from April 2016 onwards. This effectively reduces the basic rate from 18% to 10% and the higher rate from 28% to 20%.

As per the government paper however:

This measure reduces from 6 April 2016 the 18% rate of CGT to 10% and the 28% rate of CGT to 20% for chargeable gains, except in relation to chargeable gains accruing on the disposal of residential property (that do not qualify for private residence relief), and carried interest.

Therefore, if you are selling a property that is not eligible for PPR relief, then you will still be charged rates of 18% as a basic rate payer and 28% as a higher rate payer.

The justification is that the government is trying to encourage individuals to invest in the stock market (into companies) rather than into property, presumably with the intention of slowing down the growth of the property market and helping with affordability for first time buyers.

How To Avoid Capital Gains Tax UK – Conclusion

Capital gains tax is simple for straight forward investing in stock markets. Invest in an ISA or pension/SIPP and you will completely avoid any capital gains.

If you cannot invest inside these tax wrappers (for example with property), it is essential that you understand the HMRC tax rules in order to greatly minimize any potential capital gains tax you would be paying.

You will hopefully find the HMRC capital gains tax section and the 2015/16 tax tables a great starting point to minimizing your tax bill.

Related Resource: Capital Gains Tax (HMRC)

Also, I find the following two books great resources for minimising taxes on your property (including income taxes, capital gains, inheritance tax and many other tax planning issues):

At only £20-25 each, if you only learn one tax saving tip, you’ll easily earn that several times over in saved taxes!

And, just think, if you do end up paying capital gains tax even after using all of these techniques, then you’ve probably made a lot of money on your asset and you should think about that!! 🙂

Thanks Monetstepper for a clear and concise explanation on capital gains tax.

I must admit I do struggle to get my head around the tax rules in the UK. They make it so complicated as half the time I don’t even fully understand how they have calculated my personal tax code!

I do keep all my savings and investments in ISA’s so I don’t have to worry about the tax implications and thankfully, this will be even easier since they are increasing the ISA limit.

That’s the easiest way to do it. Pop all your investments in tax free wrappers (ISAs, pensions, etc) and you’ll be alright!! 🙂

For saving tax best way to invest in properties and get extra limits to invest in this property. Because savings are coming in Tax free wrappers. If you want to more tax saving you have taken a consult form a CA.

Thank you for the very clear and concise information. I now feel much less worried about how much I am going to owe the taxman when I sell my buy to let. With grateful thanks.

You’re welcome Sue. There are a few different aspects involved with avoiding capital gains tax on property UK, so I hope this summed them up nicely for you.

I own retail property which is let. I want to sell a block of shops that I inherited and which has been in the family since 1932. The capital gain is horrendous, but what I would like to be able to do is lump all the property I have together, take my capital out (by selling the said block of shops) leaving the liability on the rest, as I will not have made a capital gain on the whole. Can this be done? I need to be totally legal, but find it hard to run my business with my hands tied.

Lynn – if you are unsure, you should speak directly to the HMRC.

If you inherited the property, your “base cost” for capital gains will be the market value at the date which you inherited the property, which should have been taken into consideration when working out the inheritance tax at the time.

If this was done, your capital gains tax shouldn’t be as significant.

Regarding your question, it is not usually possible to group the properties together for capital gains tax purposes as each sold property will be considered as an individual asset.

I would advise that you speak to a tax professional to discuss your options and to determine your potential tax liabilities upon sale.

Hi Moneystepper,

What a wonderful and informative site. I have a few questions regarding my situation.

I bought a flat on July 31st 1998 for £59,500, the current value is circa £200k. I subsequently moved in and lived there up until December 2012 ( 14 years and 5months). Upon moving out I moved overseas to Canada. I currently still own the property but have been renting it out since I left up until this day, minus 3 months void period. What tax liability would I be liable for? Also is there a legal and fair way to reduce my liability? I am sole owner of the property, although I am married to a Canadian Citizen.

Lastly, Can I offset my tax bill upon selling by deducting (capital improvements/essential repairs). I have approximately circa £15k in improvements/ repairs.

Many Repairs

Steve,

If you sold today, it’s highly unlikely you’d have any capital gains to pay.

With a profit of £160k, at present the 14 years and 5 months, plus another 18 months, would be liable to PPR. This means that you’d have PPR relief of £160k x (15 years 11 months / 17 years 9 months). This gives relief of £143.5k and leaves a taxable gain remaining of only £16.5k.

Then, you would be eligible for letting relief (minimum of £40k and your PPR relief) which would cover the remaining £16.5k and therefore have no remaining gain subject to capital gains tax.

Good news!

If required, you could have also deducted capital improvements (but not essential repairs as they are not “capital” in nature) and used your personal allowance, but neither are needed in your situation.

Hi Moneystepper

I have a situation fairly similar to Steve’s:

I bought a flat in London in June 1998 for 150k, lived in it till June 2002, moved to USA and have been renting it ever since with the exception of 10 months in 2011. Current valuation is 550k. Again what would my CGT liability be on a sale now?

I have about 30k of repairs.

Best regards, very helpful site.

Hi Oliver,

Have you lived in the property at all since 2002?

If you have, you can base your calculations on an “absence in the period of ownership” for PPR. If not, you’ll be subject to the standard PPR and letting relief as outlined in the article above.

Remember, repairs are usually not “capital” in nature, and hence they should have been used against your rental profits whilst being rented out rather than against your capital gains tax bill.

Hi,

My wife and I are wishing to sell our property in the UK. I am currently a non resident and will be working in the middle east for approx. 2 years.

My wife lives in the property with our children. We believe the difference in the purchase price and the selling price will be no more than 10K. We have never rented the property out or used it for anything other than a home.

Do we need to pay any capital gains tax on the property or any tax at all?

Regards,

Kevin

Kevin – you should check with a tax professional, or give the HMRC helpline a call. However, from the gov.uk website, you can see the following:

It sounds like in your example there will be no capital gains tax to pay.

Regarding other taxes, there will be stamp duty to pay, but this is paid by the buyer of the property and that’s it.

Hope that helps.

Hi Moneystepper and thank you for this article, how would the calculation of CGT on the sale of a property change if the seller, who has owned the property for 15 years, has been a non-resident for the last 6 years and is now considering returning to the UK before selling the property?

Tricky one Charles.

My understanding would be that you would pay Capital Gains tax as normal if you return to the UK and become a UK resident for tax purposes.

In this case, for the period you were non-resident, I assume that you were renting out the property. Therefore, you’ll need to work out the PRR and letting relief as per our example.

One thing to keep in mind in the calculation is the tax years in which you left and returned for the sake of PRR:

However, if you were to sell the property before you returned to the UK, because you have been non-resident for over 5 years, you would be exempt from Captial Gains Tax on the property for the period before 5 April 2015. Only the proportion of the overall gain which relates to the period after 5 April 2015 is chargeable and you have the choice of calculating the value of the property on 5 April 2015 and then working out the gain from this base. In this instance, it is unlikely that your taxable gain would be greater than your annual allowance.

Even in this instance, you can apply PRR for the last 18 months against the gain that you had after 5 April 2015 and hence this would reduce your liability to zero if you sell before October 2016.

Therefore, I’d recommend that you perform your calculations under the first scenario to work out if you would be liable to CGT if you are a UK resident after PRR, letting relief and annual allowances. If you are, then it could be worth selling the property whilst you are still non-resident.

Finally, it’s unlikely to be the case, but you’ll also have to check with your local tax system in the country you are currently living to see if there would be any taxes due there if you sold the UK property whilst being resident of that country.

Pffff, tax, hey…!! 🙂

Thank you for the insightful answers you have been most helpful 🙂

Hi Moneystepper, thanks for the great article.

Do I need to have a buy to let mortgage in order to claim letting relief?

thanks!

You don’t Andy. For example, if you don’t have a mortgage on a property at all, then you could still claim letting relief.

The conflict that may arise is that if you have a normal residential mortgage (for your own home) and then you rent out the property. This is not allowed as for most lenders you will need a buy-to-let or a permission to lease mortgage to rent out the property.

However, this logically shouldn’t have an impact on the letting relief from a capital gains tax perspective as having the residential mortgage suggests that you lived there and hence you’d get PRR instead.

thanks moneystepper!

I have rented out a property for 20 years and it has never been my main residence. I now wish to sell it and purchase another property to rent out. Although the original property(small flat) has increased in value over the 20 years. The property I want buy cost more, how do I stand regarding CGT ???

Hey Barrie,

I’ve addressed your question in today’s podcast. I hope you find it useful:

https://moneystepper.com/qandapodcasts/question-13-how-do-i-minimise-my-capital-gains-tax-bill/

If you are interested in the topic of avoiding capital gains tax on property in the UK, we have just released an episode of the Moneystepper Q&A Podcast which addresses a specific question from a reader on the subject. Enjoy!! 🙂

https://moneystepper.com/qandapodcasts/question-13-how-do-i-minimise-my-capital-gains-tax-bill/

Hi, I am a non tax payer and wish to sell my buy to let property. My profit would be approx £100.000. What would my capital gains bill be please?

Hi Joyce,

We’ve just recorded a podcast answering your question which you’ll be able to find at:

Q&A 23 – Do I Pay Capital Gains Tax If I Don’t Pay Income Tax?

Hope it helps.

Hello. I am selling a buy to let property which will have a profit of around £30k (purchase price £66k, sales price £100k, approx legal costs + improvements £4k). The property is currently in my name, but will it be worth putting in joint names with my husband prior to sale to double CGT allowance? He will be paying CGT at 28% whereas I will be paying at 18%. There would obviously also be costs involved for transfer of names (approx £500?). Many thanks

Hey Ros,

Thank you for your comment and your question regarding your capital gains bill.

“Gifting” half of the property (as long as there is no transfer of mortgage liability or consideration paid for the transfer) wouldn’t incur CGT or SDLT.

Then, with the property in joint names will mean that you get another £11,100 annual exemption allowance to take off your gain. At 18%, this would be £2,000. At 28%, it would be £3,100 saved.

The process to gift half the property has to be done with the land registry (and can be done yourself for £40 or so), but you may want to use a solicitor to make sure its all perfectly completed which will set you back up to £300-400.

Hope that helps.

Thank you this is really good help, but can you please explain how you get the 1.5/10 in your example.

Janet

No problem Janet – I’m pleased you found it useful. The 1.5/10 comes from the fact that you can claim your last 18 months of owning the property (was previously 3 years) tax free. So, 1.5 represents this 18 months, and the 10 represents the 10 years between 2004 when the property was bought in the example, and 2014 when it was sold. Hope that answers your question.

Hi, what a useful post, you have explained everything very clear, thank you.

So for non-residents, the CGT only applies on the difference between the market value on and after 5 April 2015? Say the flat was bought in 1990 at 100,000. The value on 5 April 2015 is 300,000 and now is 350,000. When the non-resident calculate CGT, if he/she was to sell the flat sometime this year, then it would only be 18% or 28% on 50,000 (350,000-300,000) and NOT 250,000 (350,000-100,000)?

The same applies if he/she was to gift the flat to his/her child?

Hi Karen,

Indeed. We haven’t covered non UK residents in the article, but my understanding is the same as yours. Non-residents calculate their CGT on property with a cost basis as the market value on 5th April 2015. So, if the non-resident sold the property for £350k and it was worth £300k on 5th April 2015, the taxable basis would be for £50k (less any improvement costs spent on the property since 5th April 2015 and any costs of disposal such as estate agent fees).

Non-residents still have a capital gains tax allowance (£11,100 for the 2015/16 tax year) and can claim PRR for the last 18 months of ownership, but only if they qualify under the following:

Finally, the same would apply if the non-resident were to gift the flat to their children, and the current market value at transfer would be used as the sale price and also as the children’s new cost basis in the future.

Hope that helps. 🙂

Hi,

Thanks again for the clarification, In fact, your article explains much much better than the HMRC website (unless one goes to the table provided and work out the numbers manually)! It was not clear to me if the CGT for non-resident is on the difference between original purchasing price and the selling price after 5th April 2015 or on the difference between the price on 5th April 2015 and a later date.

The bit under ‘overview’ is confusing

https://www.gov.uk/guidance/capital-gains-tax-for-non-residents-uk-residential-property#CGT-workout-gains

May I ask you a couple more questions? How to find out the value of flat on 5th April 2015? Does this have to be carried out by HMRC and how to do this independently?

The only tax liability when gifting to their children is ‘CGT’? Is there any other tax involved? Apart from fees to solicitor, any other fee you can think of?

If the parents do not need control over the property, is gifting better than setting up a trust? Does one pay less tax in the long run and fees if a trust is set up for this purpose? What about ‘non-resident trust’ and what’s the benefit of setting up a trust?

Thanks again for your advice.

Karen

No problem Karen. In response to your further questions, I would have to say that on tax planning for non-residents including setting up trusts is probably questions that you should be firing at an independent taxation specialist.

As far as finding out the value on 5th April 2015, this is an estimate that you will make when completing your returns. It will be formed by looking at the value of your property when you sell, and flexing it for % movements in the local market. Additionally, you can compare this to sold house prices prices for similar properties in similar areas around that time. As long as you can honestly support your valuation when challenged, you should be good.

When gifting the property to your children, there will be CGT due and the gift may be subject to inheritance tax if you were to die within 7 years of making the gift and it forms part of your estate which totals over £325k:

https://www.gov.uk/inheritance-tax/gifts

https://www.gov.uk/inheritance-tax/passing-on-home

Stamp Duty may be payable if there is any transfer of money or of a liability (e.g. mortgage) on the property. Otherwise, a true “gift” does not incur stamp duty.

The only fees for the transfer would be solicitors fees (and/or land registry fees) for the change of title deed.

Depending on the value change on the property since April 2015 (and subject to your inheritance tax planning), there may not be any tax due on the gift. If this is the case, setting up the trust is of no benefit, other than if you want to add in extra stipulations of what happens to the property after you gift it. However, if you’ve got a tax bill due, it may be beneficial. As I say above, this is probably where you need to get regulated financial, taxation and legal advice.

Hi, I purchased my house in 2005 (189,000) and had no intentions to let it until my job (military) took me overseas for 3 years in 2012. I have now returned back to the UK and assigned to the same area my property is located in. My tenants contract ends in May 2016 therefore wish to continue to let it until then after which I want to sell and buy elsewhere immediately (worth 280,000). I have no plans of letting the property, my intentions would be to live there. Two questions – Would I have to pay the CGT for the 3 years I was serving overseas as well as the additional months remaining? Do I have to live in the property after letting it for 18 months before selling? Many thanks

Hi Maxine,

Thanks for your comment and questions on capital gains tax.

Your profit basis would be your sales price less (£280,000) less your purchase price (£189,000) less any costs related to the sale (estate agent fees, legal fees, etc).

Because it was your primary residence between 2005 and 2012, you can then claim PPR relief for the 7 years you were in the house before you rented it. You can also claim another 18 months on top of that, with no condition that you need to live in the property for the last 18 months of ownership.

Therefore, you obtain relief of 8.5 out of the 11 years that you’ve owned the property.

Assuming a profit base above of £91,000, this would give you relief of £70,318 leaving a taxable gain of £19,682.

However, you can then claim for up to £40,000 of letting relief, meaning that there would be no capital gains tax to pay on the sale.

Hope that helps Maxine.

Let me know if you have any other questions.

as Maxine is/was in the military it is possible that they have an entitlement to claim under the work related absence rules. Moneystoper has given the classic PPR and LR answer however where a person owns only one property which they intended to live in as their home at some point in the future but are not currently doing so because they have to live elsewhere for work related reasons the entire period of ownership could be exempt due to a combination of PRR and the period of absence rules. See a tax adviser for more details….

Great point John – thank you for the comment.

Thank you for a very helpful summary. Could I please ask for some additional advice?

We are selling our house which has been rented out for the past 2 years. We lived there ourselves for 2 years before renting it out. Whilst we were living there we had some extensive renovations costing in the region of £80,000 (side return, new kitchen/bathroom etc). I’ve heard mixed opinions on whether we can deduct the cost of the renovations as it was whilst we were living in the property not whilst it was rented out. Do you know which is true? The property in question has increased in value by £700,000 since we bought it so we are looking at a fairly hefty capital gains tax bill even with all the deductions!

Hi Lisa,

Thanks for your question.

My understanding is that the renovations can be deducted from your profit base any time while you owned the property (whether done when you are renting or living).

The key is whether they are truly costs to “improve the property”. For example, a new kitchen and bathroom may not be allowable if you just replaced like for like. However, if you extended the kitchen or truly added value through the replacement (rather than just replacing declined value from wear & tear) then they may be allowable.

Hi, Great article!

I was wondering about a situation where my dad owns a ground floor flat in his sole name. Last year he purchased the flat above his, the 2 properties were originally a single property. He was thinking of renovating the flat then gifting it to me and my sister. What would be the CGT situation here. He bought the property for £150k, is now possibly worth lets say £160k but needs about 10K to spend on it to make it properly habitable. After costs it could look like it would make a loss based on the original value. On disposal, does the flat need revaluing after the work has been done which will obviously increase the price of the flat or could it be a possible loss and offset capital gains made else where. May be a tricky one i know, hust some guidance would be great!

Hi Adam,

Thank you for your question.

Your father would need to value the property he his gifting to you at the market rate (which could be obtained from a survey valuation or from an independent estate agent). From that figure, he could then reduce the cost price (£150k) and the costs he has incurred to make it habitable (as this would be considered to be improving the property).

If this were to come to a loss making position, this could theoretically be placed (or rolled forwarad) against other gains of a similar nature. However, he may not be able to do this due to the following restriction on recognising capital losses:

Therefore, if he gifts it to you and your sister, he would not be able to use this capital loss against other capital gains or carry it forward to future years.

Hope that helps.

I purchased a second property in April 2014 for £220,000 and made improvements to the value of £25,000 without living in it or letting it. I sold the property in April 2015 for £285,000. Is there any Capital Gains Tax to pay?

Hi Francis – thanks for your comment.

First of all you will need to determine whether the improvements are allowable for capital gains tax purposes. They need to be capital in nature and be genuine improvements to the property (rather than replacements or repairs).

You can also deduct any other related costs from selling the property (legal fees, estate agent fees, etc).

If you’ve never lived in the property, you cannot claim PPR or letting relief.

Therefore, there will be capital gains tax to pay, based on your taxable profit and CGT tax rate (either 18% or 28%) on any profit over your (and your partners’ if the property is jointly owned) personal allowance for the year.

Hi, I would like to find out if I will incur any capital gains tax liability on my property. I purchase the property in 2004 for £245,000 – it is now under offer for a sale price of £480,000. I lived in the house from 2004 to 2012 – it was then rented out from 2012 to April 2015 and now being sold as vacant possession. I left the UK in 2014 and moved abroad to a non EEC country and became a non resident of the UK (I lived and worked in UK for 23 years but I am not an UK national) and still remain a non resident. I would like to know if I have any tax liability for Capital Gains on the profit I will make on the property if the sale is successful. Also I wanted to check if I remained a non resident of the UK for more than 5 years would this exempt me from having to pay any CGT. Many thanks.

A really helpful article. I ‘think’ I know the answer to my question but would sleep easier if I really knew!

My wife and I (jointly) bought a house in 1988 for £150,000. In 2010 we sold it for £395,000 but kept half of the garden. After 5 years we have now been granted planning approval to build on the site. Today we received an offer from a developer which we are tempted to accept. We lived in the house for the full 22 years that we owned it. What is our combined CGT liability likely to be?

Very many thanks

Hi

A family member is due to sell some land for in excess of £1m. wht tax would be payable on this as it has no residential property on it

Many thanks

Thanks for your question John. Capital Gains Tax is due on the sale of land as per the rules in the article above. However, because the land has no property on it, it is not anyone’s “home” and hence the PPR and letting relief will not be applicable.

The only relevant exception may be if your family member is planning to use the proceeds from the sale to buy new land. In this case, they can roll forward the capital gains tax (subject to meeting many requirements). For more detail, see this government guidance:

https://www.gov.uk/government/publications/land-and-leases-the-valuation-of-land-and-capital-gains-tax-hs292-self-assessment-helpsheet/hs292-land-and-leases-the-valuation-of-land-and-capital-gains-tax-2015

Hope that helps.

Hi,

I am an expat with non-resident status. I have a flat worth 180,000 pounds. I bought is years ago for 90,000. Can I sell it to my son for 180,000 and buy it back from him at the same price to lock myself in at that level to limit my capital gains should I lose my non-resident status in the future. I realize I will incur solicitors and stamp duty cost now.

Many thanks

I’ll be honest Tony – I’m not sure. You should consult a non-resident tax specialist. If the sale and buyback is deliberately completed to evade tax, then the HMRC will probably view it as just that: tax evasion. However, you should consult to see if this is correct!

I purchased an ex local authority buy to let property in 2001 for £80K. In 2012 I gifted a 10% share, value £16K (via land registry) to my partner. We are unmarried and this is the only property she has ever owned. I assume this transfer would have been subject to CGT but was below the threshold. The local authority now wants to redevelop the estate of 800 properties and wants to compulsory purchase our property in a few years….the property is worth around £200K. Is CGT charged for compulsory purchases? How do we calculate our CGT liability? Will my partner have to pay CGT? If so what is her base cost? How can I minimise CGT in the next few years….perhaps by further transfer to my partner who is a lower tax payer?

Thanks for your question David.

CGT is indeed charged as usual for compulsory purchases. If you have never lived in the property, you will currently be charged capital gains tax as per the article.

As it stands, your basis will be 90% of the proceeds less your £72k purchase price (90% of original cost) less related sales cost. If you are a higher rate tax payer, you will then be charged 28% on everything above your personal allowance.

Also, as it stands, your partner’s basis will be 10% of the proceeds less than £16k “purchase price” less related sales cost. That will probably be less than the personal allowance given the info in your question.

Therefore, you are correct in your thinking that you could be saving future tax liabilities by transferring more of the property to your partner, specifically given that her capital gains tax will be 18% for a proportion of her gains.

Hi

Fascinating site, so concise and helpful.

Forgive me if this has been covered I have tried to read the comments in the thread that are applicable but may have missed relative points!

My query is that I live in a property owned by my parents. They bought it so I would have somewhere to live as my original property that I had a mortgage on was now rented out.

I have lived in the property for almost 14 years (the entire duration that my parents have owned it).

I am going to move out and rather than continue letting it they may wish to sell. If they “gifted” the property to me and I sold it, would this mean no capital gains tax would be due as it has been my only residence since it’s purchase?

The property was purchased for £52k and is worth about £130k now.

Your comments would be much appreciated.

Many thanks.

Hi Trish,

Thanks for your question and your kind words.

The property has been owned by your parents with you living in it for 14 years. When they gift the property to you, they will be transferring a property which is not their primary residence. As such, CGT will be due on the sale.

Assuming that your parents have never lived in the property (it sounds like this is the case), they would have to pay CGT on the basis of the value now (£130k) less the purchase price (£52k) less any costs related to the transfer (legal fees) and capital improvements. If it is jointly owned by them, they can then also deduct their personal allowances of £11k each.

There will be no stamp duty due as the transfer is a gift. However, as mentioned in other comments, you need to make sure that it is a full & genuine gift and hence no consideration is paid by you to your parents, and there is no transfer of liability related to the property (e.g. a mortgage).

Then, if you were to sell the property, your base price would be £130k, it would be your primary residence (and hence you could claim relief in the future if required). However, if you were to sell it soon after purchasing, then the gain would fall below your personal allowance anyway.

Hope that helps.

Hi,

My dad transferred his gain of about £30000 to me , with no money exchanged, can i claim gift hold over relief?

Thanks

Ravi

Sorry Ravi, we’d need a bit more detail here to work out your capital gains tax.

If he gifted you a BTL property which had £30,000 of gain, then as per the reply to Trish’s previous comment would apply. Your Dad would need to pay the capital gains tax based on the market value when the property was transferred.

However, without more detail on the property type (BTL, his own home, etc), I cannot give you a definitive response.

I have a property which the mortgage is in my name and is my sole residence. I have no other properties. I purchased the property for 200k in 2007 just before the property crash. My partner moved in 2010 (my partner has no other property) we are unmarried but has contributed informally to running the property since then. We are now intending to re-mortgage the property in joint names (as tenants in common unequal shares), the property has been valued at £188,000 by the new mortgage company and I have reduced the existing mortgage on the property down to £135,000 using solely my own savings (the existing mortgage is interest only.) My partner has paid me £5,000 to reduce the mortgage down to £130,000. The new joint-mortgage (repayment mortgage) is for £130,000 to repay the existing loan, we will be contributing 50:50 to the mortgage payments. I will be giving 20% share in the property to my partner, I will retain 80% share. I’ve received conflicting advice. Are either of us liable for CGT as I am gifting some of the equity I have in the property to my partner?

7Hi Steve,

Thanks for this question on capital gains tax (which is also linked to Stamp Duty Tax as well).

I’ve made it into a Q&A episode of the podcast, for which I’m currently a long way ahead in recording. As such, it will be released on Wednesday 3rd February 2016 and will be Q&A Podcast Episode 74.

In the meantime, I’ll fire you an email with the shownotes as they’re a little lengthy to put here. The conclusion is that, in my opinion, you’ll have no capital gains tax to pay (as it’s your primary residence and you’ve actually made a loss) and no stamp duty because you fall below the lower limit for Stamp Duty.

Hello,

I brought a property with my wife 35 months ago for 1,400,000 and we are to sell it for 2,700,000. There is a current mortgage on the property for 1,100,000. Currently the property is divided into two. Half is rented to a business whilst the other half is rented to our business where me and my wife are shareholders. I have personally stayed at the premesis in the past, so would this be classed as a residence? What would be the capital tax liability on the above assuming that both me and my wife are higher rate tax payers?

Could you please help?

Hi Aaron.

Thank you for your question, and congratulations on the property almost doubling in value in under 3 years! Got to be happy with that!! 🙂

If you and your wife own the property as individuals, and then you let it to two businesses (even though one half is yours) then I don’t think it can be considered to be your residence.

Whilst you lived there, do you also have another property? Or, did you otherwise “elect” this property to be your primary residence with the HMRC?

Subject to the questions above, you’re going to have a pretty substantial capital gains bill on the property. If you both own the property, you will have a gain of £1.3m, less your annual exempt amounts of £11,100 each, and less the “related selling costs” explained in the article. Then, because you are both higher rate tax payers, you’ll pay a 28% tax rate on the taxable gain after you sell.

Given the value of the gain, it will certainly be worth speaking with a tax accountant (specialising in commercial property) to determine if there are ways you can structure the sale to reduce this taxable gain.

Hi,

I was gifted my home by my parents 7 years ago, but have lived here for 16years,

The property at the time was valued around 80,000 but it is in 2.2 acres as a whole,

I am selling part of the land attached to it for 50,000 what relief can I claim if any,

I am investing some so the money into an asset for my sons business, but it is machinery and it is a depreciating asset to the value of around 25,000 plus VAT

How am I fixed for capital gains tax please

Hi Margaret,

Given the complexity of your situation (and the specifics of the land and gifting), I would recommend that you speak to a registered tax specialist for your specific situation.

Apologies that I can’t be of more assistance, but I wouldn’t want to suggest anything that was misleading or inappropriate for your specific case.

Hello moneystepper I bought a house for £175,000 which was my home for a year. I then moved to a new house and rented the property for four years. Now am selling the rented house for £275,000 meaning a capital gain of £100,000. I am a high end tax payer so expect the 28%. I know I can deduct the £11,100 but can I also deduct the ‘PPR’ & ‘LETTING RELIEF’ you spoke about earlier?? If so what does this mean I should be paying in capital gains tax considering I’m on my own (no spouse)?? Many thanks

Yes Barry. Thanks for your comment and well done on the juicy capital gain!!

As it was your own home for one year, you can indeed obtain PPR and Letting relief for that 12 month period and for the “final 18 month period” as shown in the examples in this article.

Hi there,

Great website! Thanks for all the info.

We are considering buying a second property to renovate within 12 months. We would plan to live in our existing house whilst the renovation is taking place.

We would then sell our existing home and briefly move into the renovated property before selling that too.

We wondered if you might know if there is a minimum time period we would need to be registered at the renovated property as our main residence, to be eligible for capital gains tax relief?

Many thanks

Hi Rich,

Thanks for your comments.

As far as I know, there is no minimum period of occupation required to prove that a residence was someone’s primary residence.

However, where the period is short, you may find it difficult to have the evidence (a record of change in address on the electoral register, HMRC correspondence and utility bills , etc) to substantiate the property being your primary residence if it were to be required.

Hi Graham,

Fantastic sound advice.

Many thanks

HMRC are notified of all property sales in the UK. Tax law says that where a property is purchased from the outset with the sole intention of refurbishing and then selling on you are to be treated as property developers not property investors. Therefore you would be liable to income tax not CGT. Whilst the above relies on HMRC catching you out Moneystopper should have pointed that out.

If you do try to claim CGT then the rule re occupation of PR purposes is one of quality over quantity. It is necessary to demonstrate that you really lived in the property as your actual home – there is a list of factors considered when assessing that on the HMRC website

Hi – very interesting and helpful site.

Perhaps you can advise – my wife and I jointly own second property with current potential chargeable capital gain of £40,000. We want to gift a part-share of the property equally to our 4 children so that the chargeable gain would fall below £22,200. Then the following year gift another share with similar effect.

Could our children gift all or a share of the property back to us in say 2 years time with potentially no capital gains charge?

Many thanks

Thanks for your capital gains tax question James.

If you and your wife gifted 50% of the property to your children in the current year, you would both have a £10,000 taxable gain on the sale, which would fall under your annual exempt amount of £11,100 each.

Then, you could do the same next year, thereby gifting your property without paying capital gains tax.

However, if your children were then to gift the property back to you, HMRC may decide that the “sale & buy back” was done solely with the objective of avoiding tax, which would mean that you were skating on very thin ice.

However, if your plan was to gift the house to your children, and a significant change in circumstances meant that they needed to gift it back to keep you financially secure, then the reason for the second transaction wouldn’t have been to avoid tax, but to keep you financially healthy.

As I say, it’s a very thin line between tax avoidance and evasion here. I’d recommend that you take your question to a registered tax advisor.

Hi Moneystepper. I own a property in the UK which I rent and pay UK tax on. I am a non-UK resident. My husband is a UK resident. If I transfer the property to my husband (we are not seperated), is there any UK GGT liability? Many thanks.

I don’t believe so Claire, but you should check this with an independent international tax expert who could quickly confirm or deny our thoughts.

Hello.

My parents own their house and bought a second house 14 years ago for me and my children. There is no mortgage on my house. Their house is re-mortgaged on an interest only mortgage and my rent is the interest payment each month.

Now I want to properly own my house to free it, and me, from being tied to my folks house, so it is to be transferred to me, and I will get a mortgage to pay off their loan. I will not be paying any more than what it cost 14 year’s ago and after taking off both my parents’ exempt amount and improvement costs (for an extension I put on) there will be 5-6k of cgt owed.

Is there any way to reduce it further? As no-one is actually making any profit or I feel aggrieved at what is for me, a huge bill, which would have to be added to my mortgage. I realise technically it is my parents’ bill, but as they have done this to help me out I will not let them pay it.

Any advice will be appreciated.

Hi Lynda,

If you are buying the house for the cost price from 14 years ago, there will be no capital gains tax due as your parents have the same sales price as purchase price.

However, when you come to sell, there will be a much larger tax bill due as your base cost will be the cost from 14 years ago.

A better option may be to set the sales price at an amount which allows your parents to include the cost of the conservatory and their personal allowances to reduce the capital gains tax bill to 0. Then, when you come to sell in the future, you’ll have a much higher base cost.

The transfer of ownership of Lynda’s current home is a transaction between “connected persons”. Therefore the value of Lynda’s house to be used in the parent’s CGT calculation will be its current market value at the date of the transfer, not an “agreed” figure from 14 years ago.

You cannot manipulate / set a sales price when there are “connected persons” involved

Hi, very interesting information, but I hope that you can help me on my question.

I bought my house for £41,000 with an additional £7,000 loan, then an additional £10,000 to improve the house which I lived in from 1993 to 2001. I then got married and rented the house out and changed the mortgage to a buy-to-let mortgage.

I completed my self assessments every year since. After renting it through an estate agent since 2001,

I have now sold the house Dec 2015 for £120,000.

Firstly, it was my sole house at the time. I then added my wife onto the mortgage in 2008, but it was solely my details that I entered on the self assessments each year.

Now that I have sold the property, would I be liable for Capital gains as I need to complete my 2014/15 tax returns and I am lost in what I should enter on the self assessment following the information above on relief and PPR.

I still had a mortgage for £58,000, thus selling the property with a profit of £62,000 (excluding estate selling fees, solicitors fees).

Thank you. I am so pleased I found this website. It offers clear and concise answers.

Along with my retired parents, in 2003 I bought one third of a property (Tenants in common) that they have lived in as their only home. I have never lived there as mymain home. I lived next door but one until 2007. I frequently stay overnight when my Father is very unwell (recently caught sepsis whilst at hospital). They have never paid rent or given me any consideration whatsoever. I sold a rental property (and paid capital gains) to afford my third share. I have paid for all the improvements, windows, fences, etc… Father has had parkinsons for 20+ years and requires regular care which has increased to the point I now need to sell the property to release funds to pay for his 24 hour care. My Mother cannot cope. I appreciate I have made a gain. It will be around £60,000.00 (less whatever I can offset for improvements, allowances, etc…). I don’t think I will be able to claim any relief as I think dependent relief finished around 1988. My main objective was not to make a gain. I would have made much more income keeping my rental property. As care costs are extortionate, any ideas how I can reduce my Capital Gains Tax would be appreciated. I don’t earn anything although I still submit a Tax return every year. I have no shares and little savings. I am a housewife and a carer. My Mother is the main carer (and gets carers allowance), I get nothing.

HI Moneystepper,

Firstly, a big thank you for putting together such a valuable article and answering everyones questions, excellent service!

I wanted to clarify a previous statement as I believe we are eligible to pay 15k in CGT:

Non-residents still have a capital gains tax allowance (£11,100 for the 2015/16 tax year) and can claim PRR for the last 18 months of ownership, but only if they qualify under the following:

“

As a non-UK resident you will only get Private Residence Relief on a UK residential property if you or your spouse or civil partner were either living in the UK for that tax year, or stayed overnight at the property at least 90 times (or the pro-rata equivalent if owned for less than 12 months in the tax year).”

We do not qualify for PRR does this mean we are also not entitled to CGT allowance of £11,100. I think not but just wanted to be 100%

Maybe not related to this forum but thought I’d run it past you. I am trying to understand if I should have enrolled for tax returns to pay the CGT. I found this site that states:

http://www.gmexpattax.com/index.php/do-you-need-to-lodge-a-uk-tax-return/

individuals with the following circumstances should take active steps to enrol in the UK’s Self Assessment regime, and to lodge a UK tax return for the previous UK tax year:

– You received £2,500 or more in the form of untaxed income after allowable deductions, such as from renting out a property, or in the form of dividends or interest from savings and investments

We do not receive more than 2.5k in untaxed income a year as any profit we make on the property is spent on mortgage, freehold fees and maintenance costs. So does this mean I didn’t have to be enroll?

It also states:

– You made a capital gain from selling investments such as shares, a second home or other chargeable assets of an amount in excess of the Capital Gains Tax Annual Exemption

I believe the second statement means that we do need to enrol, to declare our profit and pay the CGT?

Thanks for your time

Damian

Hi I am purchasing my parents main residential property, (they part own another one which is let out). The property is valued at £300,000 and I am obtaining a mortgage for £110,000 as they are giving me £190,000 which is the rest of the value of the property.

Would they be subject to Capital Gains Tax

They would not be subject to Capital Gains Tax if it is (and always has been) their primary residence.

However, you may have to consider your stamp duty liability further. I would imagine that you fall under the threshold as the £110k is effectively the “sale”. However, this is something you should look into in further detail.

Thanks for your answer. The sale price is the full £300,000 and the £190,000 is part of the exchange so I have been told by my solicitors I will have to pay the £6,000 stamp duty. I just wanted to clarify there will be no capital gains tax as they currently live there and it has always been there residence apart from when the sale is completed and they will be moving in with their son to help with child care.

Hello

Our GCT problem is that my wife has my parents house in her maiden name, at present, we are in the process of changing it to our married name (AP1,TR1 ID1) to make use of both our Annual Exempt amounts (my father has since passed away since he gifted it to her) would it be a good idea to gift back one third share to my Mother so we each have a third, she was originally on the deeds before the transfer to my wife took place or under the terms of Mother’s will the house is due to be split 4 ways myself, sister and our two step sisters.

At transfer house was £47K now £160K any advice to help us reduce a future large GCT would be appreciated.

Regards Rob

Hi Rob,

Thanks for your question on capital gains tax. You may need to take professional advice on this one. Transferring to your mother is different to a spouse and would incur capital gains tax at the point of transfer. However, that could be something you do in this tax year, before a sale in the following tax year, which would make better use of your personal allowances, especially if you wait for the transfer to your wife to be completed first and you both transfer some of the property to your mother.

However, you will need to justify that these transactions aren’t solely being carried out to avoid taxation, or you may get in a little trouble with the tax man…!

Hi Monetstepper, What a great site. I have owned a flat for 15 years which I lived in briefly the value has increased by about 200k in that time and I pay top rate tax, I am now thinking that I am liable for a huge tax bill as I would like to sell to pay off some of my main residence mortgage, I have a partner and we have one child, I would like to limit my tax liability, would it be a good idea to gift the flat to my partner and then she could dispose of it when she wanted and have no tax liability?

Hi Stuart,

It’s not quite that simple I’m afraid!

If you have the property 100% in your name, you would save some capital gains tax by gifting part ownership to your partner. This is because, when you sell, you will both be able to use your personal allowance for capital gains.

However, you are mistaken in your assumption that your partner would have no tax liability when she comes to sell. The recipient of the gift (your partner) takes on the donor’s (your) cost base of the property. This is why no capital gains tax is due when you make the gift. However, when your partner comes to sell, they will have the same “profit” of £200k on which the tax will be based.

To determine the optimal tax structure for the sale, you will have to do the maths based on you and your partners capital gains tax rates and then gift ownership of a certain amount to minimise your tax liability. However, you also need to make sure that there is absolutely no consideration in exchange for the transfer, and that there is no outstanding liabilities on the property. In these cases, this would no longer be considered a “gift”.

Hope that helps.

Hi Moneystepper,

Thanks for the article.

I inherited a property last year valued at the time 179K. I have been using it as a weekend/holiday getaway but also let out a room. I am now thinking of selling it, current value 215k. I had to replace the boiler and get the gardens cleared at a cost of 4k, would that be deductible so my CGT bill is lower?

Thanks.

Hello Irene,

Due to the use of the property, this will not be eligible as your primary property. As such, you will incur capital gains on the property. If you sold for £215k, you could reduce that taxable profit of £36k by including costs related to the sale and inheritance process against this profit. However, the clearing of the garden would not be considered a capital improvement and hence could not be offset against your gains.

the cost of the boiler and the gardening work should have been claimed as “revenue” related expenditure against the rental profit on the income tax return as they are legitimate expenses in respect of the letting of the room. As it is not the main residence then obviously claiming rent a room allowance against income tax would be invalid, let us hope that has not been done. Neither costs is “capital” in nature so as moneystepper says cannot be claimed against CGT

Hi Moneystepper

I have two clients (husband and wife) who own their own home plus another property. They are thinking of moving into the rented property and selling their home. Where do they stand capital gains wise. The father of the husband has been living in the rented property rent free.

Hi Justine,

Given that they are selling their own home (the primary residence), this will not incur any capital gains tax. The issues with the rented property (and the husband living there rent free) will only be applicable if they plan to sell the rented property.

Thank you for your question.

Hi Moneystepper,

I’d be very grateful for some advice. I own a small flat which I bought in 2001 as my only residence. I lived in it for some time, but since getting married I have rented the flat out for around four or five years (i.e. five out of 15 years). The property was bought for £137k and is now valued at around £400k so the profit is good, implying the CGT will be astronomical?

Any ways around this? The property is currently in my name only – can I gift half of it to my husband so he can use his CGT allowance too? I also have a two-year old child, can I put some of it in her name also?

Another idea is to move back to the flat to make it our primary residence, but I fear that this loophole no longer exists?

Any thoughts you have at all on how to minimise the dreaded CGT would be very much appreciated. Many thanks.

Hi Frances,

Gifting half to your husband will help as you can both use your personal allowances to reduce the bill. However, remember that this needs to be a true gift – and therefore no consideration can be made and no liability transferred.

Gifting to children doesn’t lead to a tax liability, but children inherit the original value of the property (£137k) as their base cost, and therefore isn’t really beneficial.

You can move back into the flat and from the date that you do this, it will once again become your primary residence. However, for 4-5 years, the flat was still rented out.

Thinking about the numbers, you may not be too bad. Assuming a sales price of £400k, cost base of £137k and associated selling/buying fees of £8k, if you transfer half to your husband, you’d have a combined profit of £255k.

For PPR, it was your primary residence for 10 out of the 15 years of ownership. Therefore these 10 years (plus an extra 18 months) fall into PPR. This means your new tax basis would be £255k x (15 – 10 – 1.5)/15 = £59,500.

You will then also be eligible for letting relief up to a maximum of £40,000 (see the rules in the post above).

This leaves a gain of £19,500 which is actually lower than the combined total of your personal allowances and therefore you may have no capital gains tax due at all in your situation.

You’ll need to run these figures accurately for values, dates, costs, etc, but they’ll probably not be a million miles out given the information you provided.

I hope that helps.

where a married couple gift a share of a property which was once the main residence of one of them the person receiving the gift “inherits” the giver’s claim to PRR. This aplies only to married couples. Therefore in this case both husband and wife would be able to claim PRR and hence LR along with each having a personal allowance. See HMRC website

Great point John. When both parties’ PPR and LR are taken into account, you should almost certainly have no CGT to pay in your example.

Thank you so much! Very helpful.

Hi,

We have a rental property in my wife’s name. We want to sell it this year. To reduce the CGT liability we want to put the property into joint names with the Land Registry as this article suggest.

Please can you tell us if we have to inform or get permission from the mortgage company? We’ve tried speaking to them a number of times and they just don’t understand what we are trying to do. We’ve engaged the services of a firm of solicitors and they say they can’t do anything until we have permission from the mortgage company.

Does anyone have any experience of this and and advice regarding how to get permission from the mortgage company (Nationwide Building Society).

Many thanks in advance for any assistance.

Cheers,

Jules

This is a fairly regular transaction Jules and so is definitely something Nationwide would have come across before. You’ll need to ask to speak to a different member of staff and they should understand. If you have the mortgage on the property, you definitely will need this permission. Either:

– you gift the property (no consideration, no transfer of mortgage liability) and in this case you will have to be reassessed on whether the existing mortgage is acceptable. For example, if the house was worth £200k and you had a mortgage of £150k, then the bank would clearly have a problem if you gifted half to your wife, as you now have an asset of £100k personally, but your mortgage is still £150k.

– you “sell” half the property (either there is a consideration or transfer of mortgage liability). In this case, things may be easier with your mortgage lender, but you may now be liable for capital gains tax and/or stamp duty on the transfer.

Something to think about before calling Nationwide back…

do you get CGT on your only property? even if you buy it and sell it within 6 months?

Two questions here Alisdair. If you live in the property (and it’s your only property), it is considered as your “primary residence” and capital gains tax will not be due.

However, if you are buying property with the sole objective of “flipping”, i.e. selling the property in a short time frame for a profit, then you may actually be liable to income tax on the transaction as the HMRC view it as a short term transaction and therefore akin to income rather than long term capital gains.

Hi i bought a property for £95,000 due to circumstaces i never lived there and i rented out , i am thinking to sell the price increased to 115,000 , i just want to know please how much in capital gain tax i have to pay? I would be grateful for your kind reply,i have no mortgage

Hi Ruth,

Based on your figures, you’ll firstly need to reduce any expenses related to the purchase/sale of the property (including legal fees, mortgage arrangement fees, etc etc).

So, you’ll have £20k minus those amounts. You can then reduce that amount by your personal allowance of £11,100. The remainder will then be charged at 18% or 28% depending on your income tax band as explained in the article above.

Hope that helps.

Hi Moneystepper,

Thanks so much for a really helpful article.

I have a quick question with regards to a property asset that I’m looking to dispose of in the 2016/17 tax year. My Mum purchased a BTL property in April 2008 for £250k. In approx May 2010 50% of this property was gifted to me and I was added onto the BTL mortgage. Neither of us have ever lived at the property.

We are now looking to sell the house at an estimated value of £375k. My question is will my CGT be 50% of the market value in 2010 to point of sale? And what values will be used on my mum’s CGT bill?

Also, can we both claim the lettings relief of £40k as we have been joint landlords of this house?

In addition, I will be getting married this year, and so if I get married before the sale of the property can I gift half of my 50% share to my spouse? Is there a certain cut of period of this ie. X amount of months in advance so that it doesn’t class as tax evasion?

Thanks ever so much for your help in advance 🙂

Hi Kelly,

When the property was gifted to you in 2010, your Mum should have paid capital gains tax on the difference between 50% of the value of the property at the time of sale and 50% of the purchase price.

When the house is then sold for £375k:

Given that the property has never been lived in by either of you, you will not be eligible for PPR relief, and therefore you won’t be eligible for letting relief either.

For the last question, before the sale, you can gift 50% of the property to your spouse (but cannot transfer liability, etc) and then he will inherit your cost base (the 2010 value) and you can both use your capital gains allowance of £11,100 each.

Hope that helps Kelly.

Dear Moneystepper.I have not found any example of the situation that I find myself in.I inherited a property along with my brother and my father’s partner in 2000.In his will he wished her to stay living in the property until she died or had to go into care.She has now vacated the property and gone into care and we are free to sell it and divide the sale price.

Do we have to pay the same CGT as owners who have not lived in their property?We obviously could not sell it or live in it during the last 16 years so have not benefited from it at all during that time,apart from the increase in value.

Hi Rita,

Do you, your brother and your father’s partner all own 1/3 of the property each?

No Moneystepper,us brothers have 4/10ths each and Dad’s partner has 2/10ths.

Thanks

I have since found out from our Dad’s will that the property has been held in a trust until it was vacated by his partner.Does this make a difference?

Hi

My wife and I currently have our own PPR and a rental house that we have rented out for a couple years. We would like to sell our current PPR and move into the BTL and use it as our PPR.

Once we move into the BTL and use it as our main PPR, if we sell it in a year or two to purchase a larger PPR, what would be our CGT liability.

Hi,

I have have owned a property for ten years. It is the only property I’ve ever owned, however, due to my working circumstances, I have never lived in it.

It has been let out on occasion during that time.

Am I liable for CGT as it isn’t a second home, and was not bought on a buy-to-let mortgage?

Good question Steve. Given that you’ve never lived in it, you may struggle. I’d recommend reading the following section on “period of absence”, and speak directly to the HMRC to see if that applies if you’ve never actually lived there:

https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/323679/hs283.pdf

Can you help please – I am hoping you can help us to answer a question…. If my daughter and i purchase a house together and become joint owners on the deeds – Me being the main person who puts money in at say 95%-99% me and 1-5% her (my will also wills my house to her and not to my sons) If we became joint owners and we both lived there in that way – I am a pensioner in case that makes a difference

Thank You

Hi Wendy,

You can definitely do that, but I’m not sure what your actual question is. Happy to help if you would be able to clarify exactly what you are asking.

Many thanks,

Graham.

Hi,

My husband and his business partners own a workshop premises purchased for £220000 and now worth approx £450000. It was a wreck when they bought it and a lot of work has been done to improve it.They own half each. If they sell it would they benefit from each transferring half of their half shares to their wives ? Could all 4 of us use the £11000 relief? They run a small Limited Co from the premises and rent the premises to their Co. Does that make any difference? If we used our shares from the sale to buy another property to let out for an income would that affect CGT? Also as part of the value would be from selling the ongoing business itself together with the premises is there a way of selling it in parts in the way that shares can be sold? Are there any ways to reduce CGT in these circumstances?

Hi,

I am about to sell my home which I have lived in for 12 years. I will then move into a rented property until the right house becomes available onto the market. While waiting for the right property I might invest some money into buying a house which can be upgraded and sold for a profit. Will the profit be liable to Capital Gains Tax, bearing in mind that this property would be the only property that I actually owned at the time of selling?

Thanks

Lou,

It should not be liable to capital gains tax if you can prove that it is your PPR in between selling your current home and buying a new one.

However, it does depend a little on timeframe as, if you are in the property for under 6 months say, then transaction may be deemed liable to income tax as it is a trading transaction.

This can get a little complex, so I’d recommend that you put some time aside for some additional reading on this!

Hi moneystepper,

My mother owns a plot of land with planning permission for a 3 bed house worth around £110000. She wants to transfer the land into my name for nothing for me to build a house for my family. Will she be due capital gains tax on this, how much will it be if so and are there any ways round this?

Thanks in advance.

Rob.

You are treated as a connected person, and hence CGT will be due on the transfer. This will be at the “market value” at the time of the transfer, and this value will also be your “purchase price” if you ever came to sell the land/property in the future.

Dear Moneystepper,

Great site with clear answers in this minefield of a subject ! thank you

I am wondering how it is advisable to reduce CGT in the following scenario.

I have a property that I bought (A) and have lived in from the beginning (and still am) for the past 5 years.

I have a second property (B) that I purchased in Nov 2014 and have been doing up from the outset (staying over a few nights) with a view to moving into it. My circumstances however have changed slightly (split up) and I will probably no longer move into B.The gain hopefully will be fairly substantial – around £100,000

Can I reduce the gain made on it by moving into it for say 2 – 3 months whilst it is on the market ?

When B sells – I would then either revert to house A or purchase another one to live in and rent out house A.

To further complicate things I made a loss on a commercial property 2 years ago. Can this loss be offset against the CGT that I hope to make when Property B sells ? If it can is there any advantage from a CGT perspective of moving into B unless I want to?

I hope that that all makes sense.

Kind regards

Victoria