How does inflation impact me – The Good, The Bad and The Ugly

“The rate at which the general level of prices for goods and services is rising, and, subsequently, purchasing power is falling.”

This is the Investopia definition of inflation. In layman’s terms, it is the fact that prices generally go up in the long term. Imagine that you earn £500 per month this year. A sofa also costs £500. You can buy this sofa with your month’s salary. In two years’ time, you still earn £500 per month. However, the cost of the sofa due to inflation has increased to £550. You can no longer afford this sofa with your month’s salary. This explains the fall in “purchasing power”.

Depending on how you structure your finances, inflation can be a good, a bad or a downright ugly thing!

How does inflation impact me – The Bad

Let’s start with the bad. People generally see inflation as a bad thing to their personal wealth and on their investment returns.

Say you have £10k to invest today. You earn 10% per year returns for 20 years. In 20 years, you would have a cash amount of £67,275. If a car cost £10k today, you would think that you could buy 6.7 cars in 20 years’ time.

However, inflation may have been at a 5% rate over this time. In this scenario, the £10k car would cost £26.5k. Therefore, you could only afford 2.5 cars with your cash.

Therefore, inflation generally has a “bad” impact on your investment returns and should be factored into your investment decisions and calculations when looking at future returns.

For information, here are the 1 year, 3 year, 5 year, 10 year and 25 year inflation rates for major economies:

How does inflation impact me – The Ugly

However, inflation is often a silent killer, which can really impact your long term financial future. There are two major ways that inflation can make people poorer:

- Inflation exceeding cash returns: In our article, What should I invest in, we investigated the long term returns of certain asset classes. It showed that the long-term return of cash since 1960 in the UK was 5.9%. However, over the same period, the average inflation rate was 5.7% in this period. This means that £1,000 placed in cash savings would only be “worth” only £1,083 after 40 years due to the effects on inflation. An investment in the FTSE 250 over the same period would be worth £7,600 after 40 years. Therefore, due to inflation cash is not an investment or a long-term store of wealth.

- Inflation exceeds wage rises: We have also previously written about real wages in the UK. This article investigated the average wage rises each year compared to inflation. Since the financial crisis in 2007, actual average wages have increased by 13% compared to inflation of 22%. This means that we may have more money in our pay packets, but when we come to buy something with it, we can no longer afford the same goods or services.

How does inflation impact me – The Good

However, inflation isn’t ALL bad. Like all things in our financial lives, we need to look at inflation and determine how to get it on our side. In my opinion, this largest benefit of inflation is the impact that it can have on our debts. This will be best shown through an example of property investment.

Let’s imagine that today we take out a loan of £100k to buy a rental property (100% LTV for the ease of calculations), with the following assumptions:

- The house value will increase by 7.6% per year – long-term UK average

- The mortgage shall be interest only over a 25 year period

- The average interest rate on the mortgage will be 5% per year

- We will earn £600pm rental income. £100 per month costs. Both shall increase each year in line with inflation

- We shall use the 2.8% UK 25-year inflation average shown in the table above

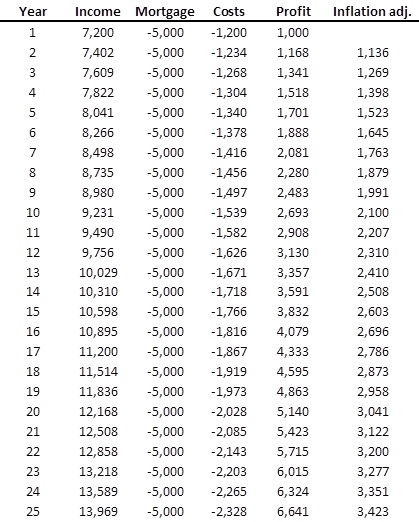

Therefore, let’s look at the impact that inflation has on our income per year is noted as follows:

Therefore, each year, our income and costs increases in line with inflation. However, our mortgage interest is always 5% on £100,000 and therefore remains the same in actual terms. This means that if we adjust our profit for inflation, our annual profit increases due to inflation.

Regarding our capital investment in the property, in 25 years’ time, our property is worth £624,175. Our capital investment increases faster than inflation.

We will also imagine that we earn £25k per year today. In 25 years’ time, if our wages increase in line with inflation, our actual wage with be £49,861. Our actual income increases with inflation.

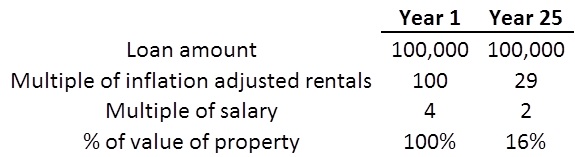

What doesn’t increase with inflation? The debt. Today, we take out the loan of £100,000. In 25 years’ time, we have to pay back £100,000. That cost is actual terms is the same. However, the following table shows the true “value” to us after 25 years:

Inflation isn’t just the “good” here, it’s the “wonderful”. When we took out the loan, we received the value of an entire house, 100 years’ worth of profits and 4 times our annual salary.

However, in 25 years’ time, whilst we have been earning a profit on our property after all costs are taken into account, we only have to pay back 16% of the house’s value, 29 years’ worth of profit or 2 times our annual salary.

Inflation can be a great friend, a foe, or a terrible enemy.

Why not make friends with it? It could help you on your path to financial freedom!

I think many overlook that dangerous part of inflation that has them lose money on their cash. They keep their money in the bank because it is safe – they never see the balance drop like it can in the stock market. But they are losing purchasing power due to inflation. It would be interesting to see what type of investment people would choose if they fully understood investing and inflation.

Ultimately, long-term investments such as stocks, mutual funds, and property, can increase more than inflation, but it’s a matter of choosing wisely and actively managing their money. Investing is something that is learned on the fly, and that’s why so many people are confused and ignorant. Finance should really be introduced in middle school and high school.