A recent Q & A on moneystepper, discussed debt repayment. In this debate, we came across two different methods of debt reduction, both of which are supported by different finance professionals and advisers: snowball and avalanche. In my opinion, the avalanche method of debt reduction is superior to snowball. Here’s why.

Snowball Method Of Debt Reduction

The first theory of debt repayment is the “snowball method of debt reduction“. The snowball method is a debt reduction strategy, whereby if someone has more than one debt, they pay off the accounts starting with the smallest balance first while paying the minimum on larger debts. Once the smallest debt is paid off, the individual proceeds to the next slightly larger small debt above that, so on and so forth, gradually proceeding to the larger ones later.

This method has gained recent recognition because it is the primary debt-reduction method taught by many financial and wealth experts. The popular financial talk-show host Dave Ramsey is a well-known proponent of the method.

The benefit of snowball is the psychological benefit. Supporters argue that seeing results sooner (ie you can completely pay down one debt and cross it off your list) encourages the continued repayment of debt.

Avalanche Method Of Debt Reduction

The second theory of debt repayment is the “avalanche method of debt reduction”. The avalanche method is a debt reduction strategy, whereby if someone has more than one debt, they pay off the accounts starting with the highest interest rate first while paying the minimum on other lower interest bearing debts.

The adoption of this method can often lead to it taking longer to wipe out the first debt, but will always ultimately lead to a reduction in the interest repaid overall and the time to get out of debt.

Snowball vs Avalanche – Which Is Better?

In my opinion, as a mathematician, there is only one choice when it comes to debt repayment: avalanche. Our aim when paying off our debt is to reduce our money which we pay in interest, or “trash cash” as I like to call it. If reducing the money we are wasting isn’t incentive enough, I can’t see how the “psychological” advantages of snowball is going to help you.

A Comparison Of The Debt Reduction Methods

Let’s explain just how significant the difference can be. unbury.me is a very useful website to show the discrepancy between avalanche and snowball.

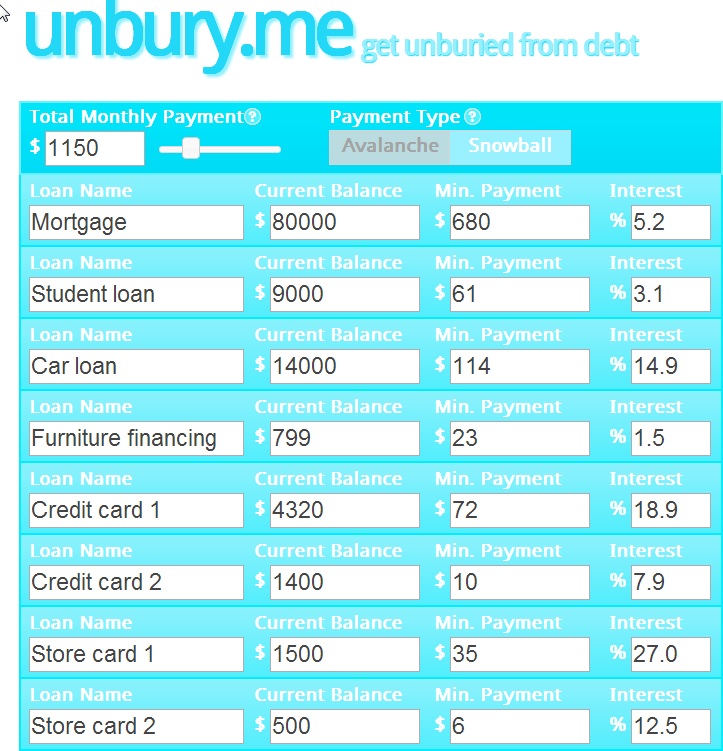

Imagine the following example. We have eight outstanding loans, as follows:

- Mortgage. Amount outstanding £80,000. Interest rate 5.2%. Minimum monthly payment £680

- Student loan. Amount outstanding £9,000. Interest rate 3.1%. Minimum monthly payment £61

- Car loan. Amount outstanding £14,000. Interest rate 14.9%. Minimum monthly payment £114

- Financing for furniture. Amount outstanding $799. Interest rate 1.5%. Minimum monthly payment £23

- Credit card 1. Amount outstanding £4,320. Interest rate 18.9%. Minimum monthly payment £72

- Credit card 2. Amount outstanding £1,400. Interest rate 7.9%. Minimum monthly payment £10

- Store card 1. Amount outstanding £1,500. Interest rate 27.0%. Minimum monthly payment £35

- Store card 2. Amount outstanding £500. Interest rate 12.5%. Minimum monthly payment £6

Total minimum payments total £1,001. After performing our fictional monthly budget, we have determined that we have £1,150 each month to pay against all our debts (ie an over-payment of £149 per month). For the purposes of this example, this is expected to stay consistent for the life of the loans.

Firstly, let’s look at snowball method of debt reduction.

This method would pay down the debt based on the smallest balance, starting with Store Card 2, followed by financing for furniture, etc etc.

Our loans have been entered as follows:

Our repayment of each individual loan is then detailed:

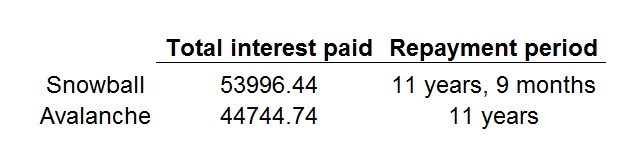

This tells us that in total, we pay approximately £54,000 in interest and become entirely debt free by May 2025.

Now, let’s have a look at what happens if we make exactly the same monthly payment of £1,150, but do so using the avalanche method of debt reduction:

So, our total interest paid is approximately £44,750 and we pay our debt in September 2014.

A Final Comparison

So, in our realistic example above, we have the following split as a result of our debt repayment:

Wow! Our monthly payments do not alter between the two methods.

However, we have saved a remarkable £9,221.70 simply by changing how we pay off our loans.

Avalanche vs Snowball Method Of Debt Reduction – Conclusion

The credit union of Ohio summarise the two methods nicely in a youtube video which you can watch below:

So, for me, whether we look at it from a mathematical or psychological perspective, the avalanche method of debt reduction far outperforms the snowball method of debt reduction!!

This is a great example! In this instance I would have paid the store card and credit card #1 first as they have the highest interest rate. So yes, generally speaking I support the second method as it makes more sense in terms of paying less interest.

However, despite the fact the avalanche method is more cost effective in the long run and some people (including yourself) support it fully, I think the first method works best for other people. There’s really no right or wrong. Yes, you pay more in interest but if this method works better for you (i.e. you are happier seeing your smaller debts disappear one after another and this helps you going), then why not keep doing what works for you. There is a reason why Dave Ramsey’s approach is so popular, it works for a lot of people. Also, there’s always a chance you change methods as you go along. Whatever keeps you motivated.

My only concern is that people do the snowball method because it is “in trend” and they have read it through Dave Ramsey without actually considering the monetary impact.

I worry that a lot of people in the above example are losing £9k because they have only read what is in the popular media without properly considering avalanche.

-> The only argument for the snowball method is a psychological one. However, in this example,

-> surely almost £10,000 of additional savings is a much better incentive than simply being able

-> to cross one debt amount off a list!

I think you are missing the point, if someone was able to think logically about their money, they would not have the dept problem in the first place! Maybe switch from snowball to avalanche once all the very small depts have been paid off.

Hi Ian,

Thanks for the comment.

I think it is important to distinguish these different periods in someone’s life.

In period X, the individual didn’t focus on their money and their long-term wealth well and they took out debt.

Once someone starts paying off their debt, they are making a conscious decision to be better with money. This is a new period Y in their life. In period Y, they will start thinking logically about money. If they start period Y by adopting the snowball method, they are making a financially sub-optimal decision.

Instructing people to start their new period Y by doing something financially sub-optimal (specifically if they don’t know why it is financially sub-optimal) is, once again in my opinion, not a positive thing to do and a quicker path back into period X.

Great post summarizing the snowball vs the avalanche. I’m a supporter of the avalanche as well but there is value in the snowball method to some people. Though I do favor the avalanche, I have used a combination when I started paying off my student loan debt. I had a bunch of smaller loan balances which were on the HIGHER END of my interest rates, not necessarily the highest. I decided to pay these off first in order to free up some income for various things going on in my life at the time, but that also freed up income to put towards the highest interest rate loan.

Now I’m 100% avalanche all the way! Awesome post.

Thanks Syed – really appreciate the comment. Thanks very much.

Sometimes when there are small loans which you can pay off in a very small time frame, I can see the benefit of getting rid of them if they are at the higher end of the interest spectrum, as not dealng with them may save admin burden etc…

Glad you enjoyed the post.