Should I pay down debt or save for retirement?

A million dollar question! Maybe even in reality if retirement contributions are substantial each year!

Paying down debt is the number one priority of many people. I’m not going to argue that this is a bad thing. Its certainly better than not prioritizing it at all.

However, many prioritize paying down of debt (whatever its form, value or associated interest rate) over saving towards retirement. Quite often, this will be a large (and costly) mistake!

Let’s look at the options at face value. For many average people, the following options may be at hand:

- Pay down your credit card debt at 15% APR

- Pay down your mortgage at 4% APR

- Save in a savings account at 1% APR

- Save in a cash ISA at 2% APR

- Save in a stocks & shares ISA in a diversified risk adverse portfolio at 4% APR

- Save in a stocks & shares ISA in a FTSE 100 ETF at 8% APR

- Invest in property/business/etc at an unknown APR

Easily, the highest APR option on this list is paying down the credit card debt. Therefore, this is the best to do. Right? Well, bizarrely, perhaps not.

Save for retirement

Moneystepper is a personal finance website. Therefore, it isn’t going to criticize anyone who is focused on paying down a 15% APR credit card.

However, we are also committed to demonstrating the “optimal” strategy from a financial mathematical standpoint. This is clear in our firm standpoint on “avalanche” being way superior to “snowball” as a debt repayment method – check out our article on the matter if you have no idea what I’m talking about!

In doing so, we run into a factor which we must consider – saving for retirement.

The majority of employers (soon to be all employers) offer some form of “matching” to your retirement contribution. This is often limited to a % of your salary. What does this mean? Well, it means that we effectively obtain a 100% return on investment in year one. Furthermore, it means that the APR you are earning on your pension (for example the 8% FTSE 100 ETF) is applied to a larger capital figure and your ROI on the interest also doubles.

Therefore, the retirement option shoots to the top of our list above.

Comparison between debt and retirement

What impact does this have in reality. Well, a lot! As ever on moneystepper, we thought this best to explain through the use of an example.

Let’s say that we can contribute 2,000.00 towards our pension in 2014 and our employer will match this amount. Also, we have a 15,000.00 loan to pay off, on which we have to pay the interest only.

Firstly, we shall take a prudent approach and assume that our pension will be invested in a diversified risk adverse portfolio at 4% APR return.

The following graphs represent the difference between…

- The balance on our retirement account (including interest received) if we contribute to retirement; LESS

- Interest paid on the full loan amount (15,000.00); LESS

- The remaining balance on the loan; LESS

…and…

- Interest paid on the loan amount if we paid our contribution towards the loan instead of retirement (13,000.00); LESS

- The remaining balance on the loan.

i.e. the benefit of applying the 2,000.00 to the matched retirement account rather than using it to pay down the loan balance. If the resulting figure is positive, this represents the benefit of contributing towards retirement. If it is negative, it shows that paying down the debt would have been a better decision.

We have also plotted 4 lines based on the application of the 2,000.00 to four different possible loans as follows:

- Mortgage @ 4%

- Car Loan @ 8%

- Credit Card @ 16%

- Horrible Credit Card @ 24%

The x-axis on the graph shows the number of years from today.

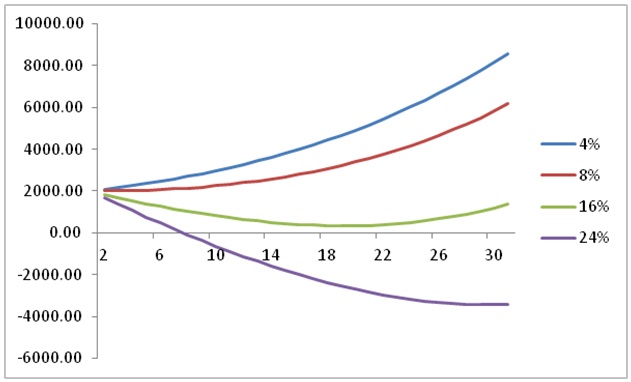

Saving at 4%

Firstly, we can see that at interest rates on the loan of 16% or below, contributing to retirement is more profitable than paying down the loan (for always and forever!!).

Additionally, even at 24% interest paid on the loan, the net position of contributing to retirement is positive for the first 8 years and hence this may be a beneficial option if you think you can pay down the debt in other ways within the next 8 years.

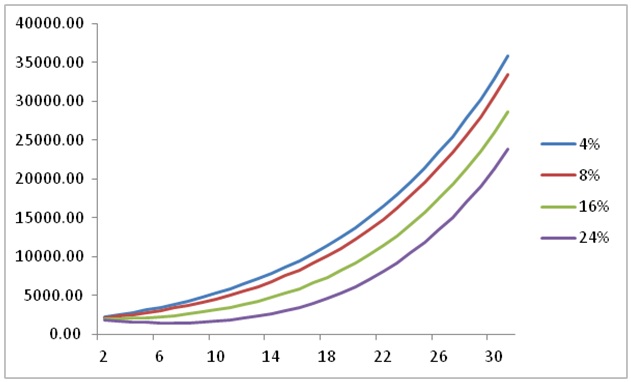

Saving at 8%

What about if we run the same figures with an 8% APR return? I use this figure as this is the average return (including dividends) of the FTSE 100 over the past 20 years. Therefore, in my opinion, it is a reasonable ROI to be using in our analysis.

Wow!

Yeah, you are reading this right. It even surprised me when I made the graphs. In fact, I checked it about twenty times over to check if it was actually true. It is.

On only a 2,000.00 contribution, having a matched contribution to a pension rather than paying down a loan will leave you over nearly 25,000.00 better off in 30 years time, even with a crazy credit card interest rate of 24%.

If we consider the retirement accounts instead of paying down the 4% interest loan (a mortgage for example), we would be 35,000.00 better off over the same period.

I hope you are wondering, like I was, the interest rate on the loan required to make the graph go below the x-axis (i.e. to make it a better decision to pay off the loan instead of investing).

Well, I’ve played with the figures. We would actually have to be paying 33.3% interest to make the graph ever touch the negative, which it only does for one year!

When should I pay down debt?

There is always an exception to the rule.

Despite the numbers clearly showing that it is beneficial to contribute to a matched retirement account, there are some times where paying down debt may be preferential.

If you are struggling to meet your monthly payments each month

In this case, paying the 2000.00 towards the capital will reduce your monthly interest (and capital) repayments which may make them more manageable.

To determine if this is the case for you, you will have to create and maintain a VERY detailed budget for all your income and expenditure. Let’s say you are servicing the interest of a loan of 20,000.00 on a credit card which is charging you 16% annual interest. Therefore, your monthly interest payment is £267 every month.

After all of your other payments, meeting this interest payment is getting difficult. By placing this one-off 2,000 against the loan capital, the monthly interest would fall by £27 each month.

Firstly, my advice would be to sort out your budget and reduce other expenses in order to meet this £27 payment and start paying down the capital, so that it falls a little in the future.

Secondly, and perhaps more importantly, I would recommend working your ass off to earn extra income, to make this reduction in the capital amount, therefore reducing further payments.

Whatever you do, you should only be sacrificing your retirement fund in the place of paying down debt in the very short-term if you have some cash flow issues. Otherwise you should be addressing the larger issues you are facing, rather than just placing this one-off amount against the loan without thinking.

If the debt is psychologically impacting you

Many people struggle with the pressures of debt and if this is weighing you down, then maybe you should consider paying down the debt to improve your health. Debt (if not properly managed) causes stress. Stress causes illness. If paying this 2,000.00 can you eliminate your debt which is worrying you (and is the only way to do so), they maybe it is a good idea to forgo some of the financial benefits of contributing to your pension in exchange for the physical and mental benefits of paying down the loan.

Furthermore, I have just been informed on my BBC Business Daily Podcast that being poor makes us less intelligent, as our brains become preoccupied with the business of just getting by. Essentially, being in debt makes us dumb!

Professor Sendhil Mullainathan, of Harvard University, explains that having to worry about where your next meal is coming from, and having to pour resources into simply making ends meet, leaves the human brain’s capacity for intelligent thought significantly reduced. This is supported by some interesting research from Indian farmers you are paid yearly and how their health improves before and after they receive their annual payment.

In brief, being in debt makes you dumb. And no-one wants to be dumb, do they?!

However, this is only the case if your debt is a problem. If you are happily meeting the monthly payments and you have a fixed and solid plan to dealing (or maintaining) your debt, then making that contribution to the retirement account is still the better option.

If your interest rate is crazy

We’re talking about the impact of payday loans. Just to emphasis a point, I’ve remade the first graph based on what would happen if you kept revolving a payday loan (in reality, this may not be possible, but this emphasizes the point!):

Try it yourself

These are all good examples, I hope you agree. However, the figures I have used may not match your personal circumstances. Not to worry. You can try it out yourself!

I’ve attached a file whereby you can just update the cells in yellow and see whether contributing to your retirement accounts beats paying down your mortgage, car loan, credit card, etc etc.

Pay down debt or save for retirement

Let me know what numbers you got? Do these figures surprise you? Are you going to maximize your retirement contributions rather than paying down the mortgage?

I suppose the best solution is to do both…is that’s possible, of course! I would focus on paying off that really high interest debt first personally.

I agree with Holly. Why not do both and see what happens, right?

Because you might be losing out on 25,000 in 30 years time by doing so! I think that is enough to make it worthwhile calculating the actual numbers if you have a matched pension scheme with your employer…

We are focusing on paying down debt, primarily because we have WAY too much, and we’ve got a semi-nice cushion in our retirement funds right now. We’ll definitely increase our retirement savings once the debt is gone, though.

Do you have a matched pension scheme with your employer Laurie? If so, what numbers did the spreadsheet give you?

I put most of my extra cash towards debt and contribute a small amount to retirement each month. Even with the debt, I would hate to not save anything for my future. I look forward to the day when I can allocate much more to investments.

Do you have a matched pension scheme with your employer Erin? If so, what numbers did you get in the spreadsheet?

It is advisable to save for retirement and maintain a balance in your finances

Thanks for posting about this. I have wondered this many times. I recently consolidated my CC debt into a personal loan at 8.99% which is much better than the 22% I had with the card. I did it at the same place I had my car loan (already paid off). I also have student loans at 5.25% and one at 3.25%. I hope to pay off my cards within a year, and after that start investing more in my retirement. As I work for the US gov, an automatic portion already goes out to my pension each month (I have no say, and must stay for 10 years to be vested).

My current goal was to pay down all my debts within 5-6 years, but now I’m not so sure. I want to save more for retirement as well. I have some other federal loans, but as a gov employee, they will be forgiven in 10 years. I’m not as concerned about them.

I have to do some investments on my own, and I see that you mention ISA many times. I don’t think that this is an option in the US. Do you have suggestions for comparable high interest savings in the US? It seems like I’d have to be creative with a Roth IRA.

Thanks for any advice.

I’m not an expert in US finances, however it would seem that a Roth IRA is the equivalent of an ISA here in the UK.

The first key step is to run your figures in the spreadsheet attached in this post and determine if returns on the extra contributions to retirement will exceed the debt repayments. This is usually only the case when your retirement contributions are matched by your employer.

Then, if you determine that you want reduce your debt repayment in favour of contributing more to retirement accounts (remember: this should only ever be considered if its financially beneficial), you can look towards your Roth IRA and “investing” in the long-term through equity market investments.

Thank you!