Is the Eurozone crisis over?

In April 2010, the Greek government debt was downgraded to “junk” status. This sparked the start of what people generally refer to as the “Eurozone crisis”. This questioned everything about the Eurozone. Was the European Union stable politically? How would its economy survive? Could the single currency (the Euro) stay in place?

For the months and years that followed, a week (and at certain times a day) would not pass without a headlines all over the mainstream media. Graphs showing the extent of the failing economy. Opinion pieces on the unsustainability of the single currency. The resulting political unrest. The high levels of debt across Europe. Another day, another article.

Then, economies in the UK and the US strengthened and their markets began to recover. All of a sudden, the headlines and discussion of the European currency died down. Does this mean we are out of the so-called Eurozone crisis? Absolutely not! The Eurozone crisis is NOT over. In fact, it is getting worse every day!

What was the cause of the Eurozone crisis?

The Eurozone crisis was a result of many conditions:

- easy credit conditions during the five to ten years leading up to 2009. This encouraged high-risk lending and borrowing practices (as was noted in the UK and the US);

- the impact of the “global” financial crisis of 2007–08;

- over investment and rapidly increasing real estate prices (the bubble) which built over the ten years leading to 2009;

- fiscal policy choices related to government revenues and expenses (especially in Southern Europe); and

- public pensions and public wages which were among the most generous in the world.

The sparking point for the Eurozone crisis is thought to lie in Greece. In 2009, a new Greek government revealed that previous governments had been under-reporting the budget deficit.

By 2010, it had been determined that the Greek debt exceeded $400 billion. Investors worldwide became hugely concerned that Greece would default on its loans. This fear spread to other Eurozone countries in Southern Europe (Spain, Italy, Portugal & Cyprus) and to Ireland (who suffered from a huge bubble in their Real Estate market).

Greece was bailed out in 2010 with a €110bn loan from the EU and the International Monetary Fund. After several months of fiscal austerity (which lead to a huge number of riots around Greece), another €130bn loan was granted.

Has the Eurozone crisis subsided?

During 2012 and 2013, the mainstream media have reported fewer major incidents and opinion pieces on the fate of the Eurozone. The general consensus worldwide is that the Eurozone is coming out of the other side of this tumultuous period.

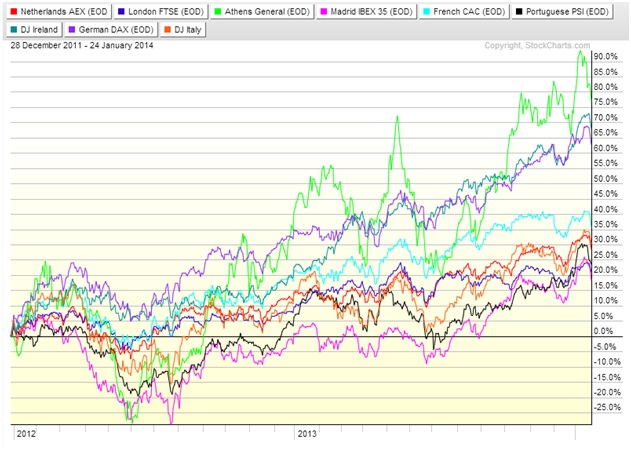

The financial markets and leading indices in Europe support this opinion. Markets are “forward looking” and precede an economic recovery. Since the start of 2012, European markets have significantly improved, demonstrating the subsiding of investors’ concerns:

Markets have increased anywhere between 20% (Spain & Portugal) and 80% (Greece) in this period, which shows that confidence is returning to the market.

However, the fact that Spain & Portugal have increased by the lowest amount is no coincidence as we shall see later.

So, the markets seem to think that things have significantly improved. Does the data agree that the Eurozone crisis is over? In short: no, not at all.

Unemployment

One significant indicator which would suggest that the Eurozone crisis is over would be a reduction in the unemployment rates (specifically youth unemployment rates). This was one of the resounding features of the Eurozone crisis. Every other media report seemed to contain an interview with an unemployed person or family struggling to get by. You would therefore assume that, in a recovering Eurozone, these levels of unemployment would have significantly reduced. They have not. In fact, quite the opposite is true.

Unemployment rates have fallen in the UK, US & Japan. In comparison, the unemployment rates in the Eurozone continue to rise. The EU in general has seen the overall rate increase from 10.2% to 11.1%.

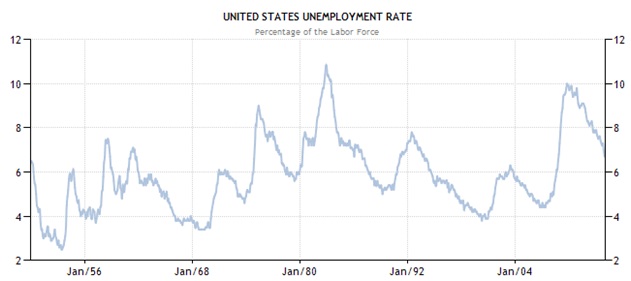

11.1% is significant. To understand how significant, we need to put it into context. For example, the US unemployment rate has not been higher than 11.1% since the Second World War:

The unemployment rate in Cyprus is up 7.4%, Greece is up 6.2%, Spain and Italy are both up 3.2%. To put that in perspective, Cyprus’ rate increased between the beginning of 2012 and end of 2013 by almost twice that of Japan’s unemployment rate!

And, if those numbers were not concerning enough, it is not just the change in percentages that are worrying. The actual unemployment rate percentages in certain countries are now the highest they have ever been.

According to the Bureau of Labor Statistics in the US, the highest ever recorded unemployment rate in the US was 23.6% in 1932. This was during “The Great Recession”, which is considered to be one of the worst (if not the worst) periods in economic history. In the UK, the worst ever rate (recorded in the same year) was 17%.

Therefore, Spain and Greece both have unemployment rates that are higher than those EVER recorded in the UK and US.

As far as unemployment is concerned, the Eurozone crisis is FAR from over. This is especially the case in those Southern European countries (Greece, Spain, Cyprus, Italy & Portugal).

Government debt

One of the very concerning graphics you would see in mainstream media was the amount of government debt as a percentage of GDP. Depending on your opinion, this is a very significant or not at all significant factor.

The easiest way to think about debt vs GDP is to equate it to your own personal debt vs your annual salary. For example, if you have no other debt, dividing your outstanding mortgage amount by your annual salary will give you your equivalent percentage.

With government debt, as with the personal debt figure you have just calculated, there are two schools of thought:

1) Debt is bad – having a high percentage of debt means you are in serious trouble

2) Debt can be good – as long as we are using that money to earn cash elsewhere or it is cheaper than the alternative (mortgage vs rent), then this isn’t too much of a big deal (as long as the repayments remain affordable).

With government debt, as with personal debt, one thing is for sure – a higher debt to GDP % definitely provides additional risk. And if your economy is in trouble, risk is NOT something you want!

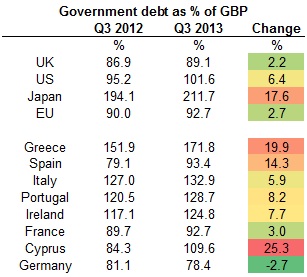

What is the current ratio of debt to GDP for some European countries?

Again, the numbers (specifically in Southern Europe) are high. They are not the highest (as we can see that Japan’s government debt is over 200% of GDP). However, the key difference is affordability.

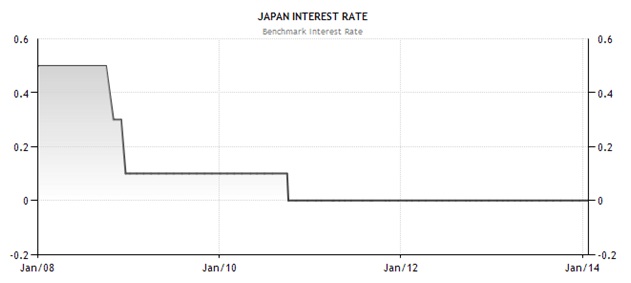

Take the mortgage example, you might be happy with a 2x annual salary mortgage and this might be affordable (your percentage debt to GDP would be 200%). However, if interest rates doubled, then you would suddenly find yourself in a lot of trouble.

The same thing is true for countries. Here is a graph of Japan’s interest rate since 2008:

In comparison, here is a graph of long-term interest rates of Eurozone countries since late 2009:

Going back to the debt to GDP ratio table shown above, the other worrying trait is the rate of these increases. Germany shows a slight decrease, whereas the UK has increased its borrowing by around 2%.

In comparison, Cyprus has increased its debt to GDP ratio by 25%, Greece by 20% and Spain by 14%. These levels of increase in just one year do not seem to suggest that the Eurozone crisis is over; quite the opposite in fact.

Real Estate

Do things look any better from a Real Estate perspective? Real Estate prices across Europe plummeted during the financial crisis. The same occurred in the UK and the US. The bubble was unsustainable. However, it is generally believed that an increase in property prices is a good indicator of a strengthening economy.

This has been seen (and much welcomed) in the UK (annual price increase between Q3 2012 and Q4 2012 of 3.8%) and in the US (an 8.4% increase over the same period).

Once again, the Eurozone (and specifically the Southern European countries) do not fare as well:

Global house prices are increasing. In 2013, Global Property Guide reported “World housing markets’ strongest performance since the boom years of 2006 and 2007”.

Unfortunately, this does not seem to apply to Southern Europe. Italy, Portugal and Spain are all posting annual house price changes that would make newspapers in the UK and US cry out “burst bubble”. The situation is even worse in Cyprus and Greece.

This Eurozone crisis certainly does not appear to be over when we look at the data!

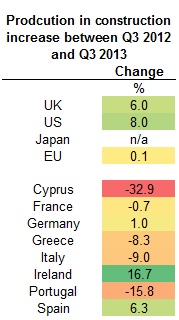

Production in construction

So far, analysis of unemployment rates, government debt and property prices have all suggested that the Eurozone crisis is getting worse by the day.

Maybe they are building their way out of the doldrums? Eurostat recently released their latest figures on production in construction.

You guessed it – another failure in the Eurozone:

The UK and US have again ticked the box for this indicator of economic growth. The Southern European countries failed miserably, with Portugal, Spain and Cyprus all performing horribly. A notable mention for Ireland here who seem to be (with the aid of their controversial tax breaks) rebuilding their economy, quite literally, brick by brick!

Inflation / deflation

Another concern across the global economy is deflation. With the significant economic stimulus from central banks and bailouts, the devaluation of currencies is a significant risk.

The UK and US are currently avoiding this risk and maintaining reasonable levels of inflation.

Oh dear. Deflation has already taken hold in Cyprus and Greece in December 2013. France, Italy, Ireland, Portugal and Spain all have inflation rates below 1.0%.

More worryingly is the direction and the speed of the change. Many countries (the Southern European countries being the worst culprits) have year-on-year falls of around 2.0%. If this rate of change continues, they will all be in deflation by mid 2014.

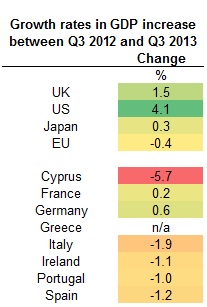

GDP growth rate

Perhaps the most used and well understood indicator of economic strength and improvement is a country’s GDP.

Whilst the UK and US are both growing at an impressive rate, the Eurozone is falling:

It’s those Southern Europe countries again – Spain, Italy, Portugal and Cyprus all have GDP decline. Greece has not reported data since 2012, but I can assure you that if it was plotted, it would be highlighted well and truly in red!

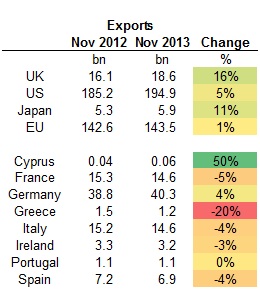

Trade balance

The only positive shift (other than stock markets) that I can see is the Eurozone international trade in goods.

Between November 2012 and November 2013, the goods balance with the rest of the world changed from a €4.0bn deficit to a €6.5bn surplus. This seems like a huge improvement.

When we dig into the figures, we see that of this €10.5bn improvement, €2bn was contributed by Germany, €5bn by the UK and €2bn by the Netherlands.

This figure is greatly impacted by changing exchange rates. Moreover, an increasing net balance is not necessarily a good thing.

Yes, it could be caused by an improving economy. However, it also could be caused by the decrease in exports not falling as rapidly as the decrease in imports (due to a lack of domestic demand).

You guessed it – Italy, Spain and Portugal all have a trade balance improvement, but in each case their exports have fallen year-on-year. This is simply because their inhabitants (people & companies) can no longer afford to pay for the types of goods which would be imported.

Is the Eurozone crisis over? No!

We have analyzed the Eurozone recovery over seven key economic indicators. In each one of them the Eurozone performs poorly. There are countries which are doing well, particularly Germany. However, the overriding theme is the terrible (and continually deteriorating) state of the Southern European countries:

The mainstream media seem to have become bored of reporting about it, but beware all Eurozone investors, employees, governments and inhabitants. The Eurozone crisis is NOT over. In fact, it is getting worse every single day!

good visuals and interesting findings!

We are in the same boat here in the U.S., or at least a similar one, and it amazes me how so many people are believing the hype and getting back on their consumerism bandwagons, spending like banshees. We’re not out of the woods, not by a long shot!