Help to Buy Scheme – Who has it helped?

The first part of the Help to Buy Scheme was launched in April 2013. One year on, we look at the impact this has had. Specifically, we focus on the particularly lucky Londoners who were the first adopters of the Help to Buy Scheme.

As a reminder, the first part of the Help to Buy Scheme is defined as follows:

- Buyers contribute a 5% deposit

- The government provides an equity loan for up to 20% of the property value

- A 75% mortgage provides the remaining funds

- Available only for new-build under a certain amount (less than £600,000 in England)

- The government loan is interest-free for the first five years.

- Also known as “phase one” of Help to Buy.

Impact on London house prices since the launch

The Help to Buy Scheme has widely been accepted to have had a significant impact on house price increases in the UK.

Between, Q1 2013 and Q1 2014, according to the Nationwide House Price Index, the average London house price increased by 14.0%.

In comparison, new build properties (those eligible for the help to buy scheme) in London increased in the same period by 20.7%.

This seems to suggest that the Help to Buy Scheme has had a direct impact on house prices in the period.

A Help to Buy Scheme example

As we highlighted in our guest post at The Property Hub, the power of leveraging makes these returns rather remarkable.

Imagine that we bought the average priced London new build property in April 2013, which was valued as £318,039.

Under the Help to Buy Scheme, our financing would have been broken down as follows:

- Deposit = £15,902

- Government deposit = £63,608

- Mortgage = £238,529

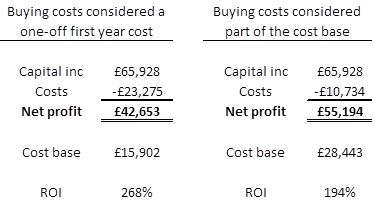

We would also have incurred costs of £9,541 stamp duty and other costs (surveys, legal and mortgage setup) of an estimated £3,000. During the first year, at 4.5% interest rate, the mortgage interest paid would be £10,734.

Effective returns

The property has achieved a capital gain of 20.7%, equal to £65,928 in one year. Depending on how we account for our costs and cost base, our returns for the year are as follows:

The annual return for the average new build home bought under the Help to Buy Scheme is a remarkable 268% ROI.

How does this compare to other returns in the same period?

- 1 Year Bond – 1.6%

- Easy Access Cash ISA – 1.6%

- Peer to peer lending – 5.7%

- FTSE 250 – 20.0%

Once again, I think this emphasizes that cash is not an investment.

Who has the Help to Buy Scheme hindered?

Obviously, the Help to Buy Scheme has helped these few people who were lucky enough to take advantage of the scheme in April 2013. However, what does it mean for the average first time buyer? Well, clearly its not good. In figures:

- In Q1 2013, the average first-time buyer property was £266k

- By Q1 2014, this has increased to £318k (20% year-on-year increase)

- According to ONS statistics, wages have increased by 1.9% in the period

- The average annual wage has increased from £24,440 to £24,908 in this time

The deposit

In Q1 2013, the 5% deposit was £13.3k. This represented 54% of the average annual wage.

In Q1 2014, the 5% deposit had increased to £15.9k (an extra £2,600). This is 63% of the average annual wage.

However, the increase in the deposit is only the first issue caused by the Help to Buy Scheme pushing up house prices.

Hidden extras – stamp duty

Also, when we buy a property of this value, stamp duty will be charged at 3%. In 2013 and 2014, this would have been £8K and £9.5k respectively. Therefore, between the deposit and the stamp duty, we need to save up an additional £4,000 to buy the same property one year on.

The government loan

The 20% government loan provided under the Help to Buy Scheme, which is eventually repayable and will start accruing interest after 5 years, increased from £53k up to £64k. £11,000 more in one year – that’s 44% of the annual average salary.

The mortgage repayment

The mortgage amount has increased from £199k to £238k. On a 25 year 5% mortgage, this increases the monthly payments from £1,178 per month to £1,410 per month. Based on the annual average salaries, this is clearly the biggest problem of all.

After tax, the monthly average take home pay in Q1 2013 and Q1 2014 was £1,787 and £1,818 respectively.

In Q1 2013, the mortgage repayment for the average first time buyer in London on the Help to Buy Scheme would have been 66% of their take home pay. It is suggested (and I would aim for less than this), that your housing costs make up no more than 25% of your take home pay. Therefore, this figure is clearly not sustainable.

However, in 2014, it got a whole lot worse. In Q1 2014, this percentage increased to 78%.

You might argue that people won’t get themselves into this situation. However, isn’t this exactly what the Help to Buy Scheme is designed to do: help the average first time buyer get on the property ladder.

With 78% of take home pay spent on the mortgage, and another 6% (£105pm average in London) being spent on council tax and 8% on utilities (£150pm average in London), this leaves the average earner with 8% of their take home pay, equivalent to £149 per month, to spend on everything else in their life (assuming that they save and invest nothing towards retirement or other savings). Clearly, this is not good!!

One year later, who has the Help to Buy scheme actually helped?

Well, its helped people who already owned property. Its also helped those lucky few early adopters.

However, it is tough to argue given the figures above, that the Help-to-Buy scheme has helped anyone who is looking to buy their first property today.

Ben Southwood, head of macro policy for the Adam Smith Institute, clearly agrees that the Help to Buy Scheme is not helping the people it is “designed” to help:

I find it interesting that they named the program a “Scheme”. That word is so similar to “scam” I’m surprised the public took interest in the program. It also sounds reminiscent of what happened in the US during our last housing bubble; banks were making it very easy for just about everyone to get a loan and it inflated our housing prices. It ended up out-pricing the average worker from most housing markets.