Credit cards can be a very dangerous thing. However, if you learn the right way to use credit cards, you can find that they are also a very useful tool in building long term wealth and moving along that path to financial freedom.

Many times in my Moneystepper lifetime, I’ve heard the following statements:

- Credit cards are evil

- You should never have a credit card

- Cut up all your credit cards

And, as a personal finance website, I do agree somewhat with what these statements are trying to get out. If, like Tom in Question 3 of the Moneystepper Q&A podcast, you have a £10,000 credit card balance and you are paying 24.99% APR, then credit cards are pretty evil.

The Right Way To Use Credit Cards

But, it’s not as simple as that.

I like to think of credit cards as a knife. Yes, if they are handled without care, they can be extremely dangerous and when gravely misused they can be fatal (to your finances).

However, credit cards also serve a purpose and they can be extremely useful when they are used correctly. That’s why the saying isn’t “like a spoon through butter”!

Therefore, I’d like to share with you today how I use my credit card, and some steps to avoid misuse.

Step 1: Set up a direct debit to pay your card in full

The key to successful credit card management is paying your card off in full every month. Credit cards are great for their owners as a form of paying for items (and delaying the cash payment by around a month). Beyond that, they just become a very high interest loan.

So, how do you do this? Well, when you take out your credit, then set up a direct debit to repay the balance each month in full. This is incredibly easy to do. In fact, it’s part of the application. There will be a section where you fill in your bank details to pay off the card, and there will be a box asking you whether you want to pay the minimum balance, the full balance or some other number each month.

Just click the “full balance” box and never change it.

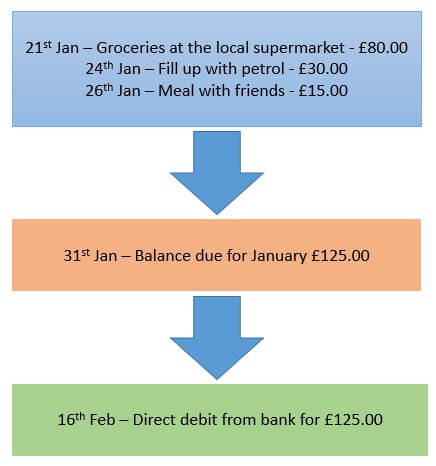

So, your transaction flow (dates are for illustration only) could be as follows:

You always automatically pay the full balance before it is due, and then you’ll never have to pay any interest on your credit card.

Your only exception when you may not want to pay the full balance each month is 0% balance transfer or 0% purchase credit cards where you enjoy a prolonged period of 0% interest. In these cases, you’ll set up a minimum payment each month throughout the 0% period, but then you MUST make sure you pay the balance in full the month before the 0% period ends.

Step 2: Benefit from deferred cashflow

At first, this seems like it does it doesn’t have any benefit. You are just paying for your goods.

However, in reality, anything you buy in one month doesn’t actually get paid for until you pay your direct debit the following month.

This deferred cash outflow is actually a nice hidden benefit of credit cards. Let’s say on average you spend £1,000 per month on your credit card, and we’ll assume that on average your direct debit is one month after the date of purchase.

Then, also say that you earn 5% interest on your cash account (which is currently possible in certain current accounts).

Then, by using a credit card instead of a debit card for your transactions, you will have earned extra interest of: £1,000 * ((1.05^(1/12)-1) * 12 = £49.

Therefore, you’ve earned an additional £49 a year just from paying your credit card down in full. But, it doesn’t stop there.

Step 3: Use a “rewards” or “cashback” credit card

There are many credit cards on the market which will offer you a % cashback of your bill each month or provide you with airmiles, supermarket vouchers or other incentives.

I’ve been using the Avios Duo Credit Card from TSB for a few years now. When you sign up, you receive two cards: one Amex and one Mastercard.

You collect 1 Avios point on the Amex card for every £1 you spend, and in establishments that don’t accept Amex, you can get 1 Avios point for every £5 you spend on the Mastercard.

You can then exchange your Avios points for flights and other rewards. I personally use mine for return flights to Marseille, where I used to live, to see friends there.

Say I want to fly for a long weekend in December, I can get a return flight for 8,000 Avios points plus £35. This flight is usually £215 return. Therefore, my 8,000 Avios are worth £180 to me.

With my Amex, I need to spend £8,000 to earn 8,000 points, and hence for each £1 I spend, I get £180/£8000 = 2.25p back. Therefore, I get the equivalent of 2.25% cashback as this is expenditure that I would have otherwise incurred myself.

Many personal finance gurus often say “no one ever got rich through credit card points”. I say “everyone can get rich quicker by accepting free money”!!

Step 4: Reap other benefits

There are also other benefits to having a credit card that you pay off in full each month. The most important of these is that it helps build up your credit rating/score/history. You will find that this is very useful when you come to taking out a mortgage on your home – which the vast majority of people will need to do in their lifetime!

Additionally, credit cards can be a vital lifeline in the case of an emergency. I actually use the available credit on my cards to act as my emergency fund, which means that I can invest the 3-6 months of expenses I would usually keep in cash in case of emergency. When a big emergency hits (which with proper planning it won’t too often), you can pay it with your credit card and then have a few weeks to liquidate any investments you need to cover the balance.

Finally, you actually receive much better financial protection when paying on a credit card rather than a debit card. Say you buy a product or service on your credit card and the vendor turns out to be a scammer, then you are protected with a credit card, whereas many debit cards wouldn’t carry the same level of protection.

So, there you go – the right way to use a credit card. And there’s basically only one thing to remember – never fail to pay your balance in full each month!

Any questions, let me know in the comments below.

Wow, I didn’t know about that dual Amex Credit card deal! I use the Amex BA card and find it’s often not accepted so having a mastercard back-up card would be awesome.

I missed out on the bonus period as I didn’t use it until around six months had passed, however I now have a good chunk of points I’ve yet to use.

I’ve heard you can now use the points to book hotels as well?

Sam

I always wait for the right timing when it’s best to use rewards. Last year, I was able to get 3-day free stay at San Francisco Marriott Marquis. This year, I am hoping to get another one or as good as what I got from last year. By the way, I am proud that I haven’t had overdue bill because I always pay in full and prior to the due date to maintain my credit rating.

These are all excellent points. Credit cards can be very beneficial financially if you use them properly. The only thing I would advise is to be careful with the automatic payments. If you use them, still be sure to review each statement for suspicious activity or errors! They do happen.