Investing my 2014 ISA allowance. Should I invest it all at once?

I recently posted an article on investing your entire ISA allowance in your stocks and shares ISA, and not only your cash ISA. If you haven’t checked it out already, I would encourage you to take a look:

Maximize your annual ISA contribution

The conclusion was that you should have maximized your ISA allowance. However, it unanswered one question. Should I maximize my ISA allowance as soon as possible or should I average my investment over the course of the year?

Why am I writing about this? Because:

- I’m in this position.

- I don’t know the answer.

If you have the full £11,880 ready now, should you invest it all at once on 6th April 2014? Alternatively, should you dollar average it over the year? The traditional advice is to split your investment by putting in a fraction 1/X every 12/X months. The X would depend on your current diversity, the amount you are investing in total and your risk tolerance.

However, I’m not convinced. My concern is the difference between returns in cash and in the stocks & shares ISA.

Essentially, the problem is that the UK market increases, on average, 10.9% (including dividends) each year. Therefore, imagine that I am receiving 2% on my ISA cash, and 1% on normal cash (taxed at 30%).

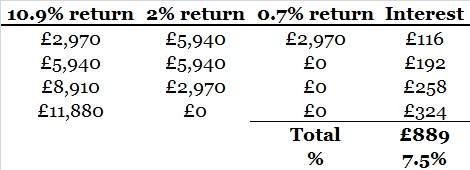

Imagine I split my investment over 4 quarterly investments as follows:

- Q1 – maximizing cash ISA contribution on 6th April 2014 (£5,940); invest 1/4 of my investment total into my S&S ISA; invest 1/4 of my investment total into a normal bank account

- Q2 – place the remaining cash from my normal bank account into my S&S ISA

- Q3 – transfer half of the cash ISA amount into the S&S ISA

- Q4 – transfer the remaining cash ISA into the S&S ISA

My returns would be as follows:

Therefore, the investment return would be 7.5% for the year. If invested the entire amount on 6th April 2014, my theoretical return would be the 10.9% average.

What about fees?

We should also include fees. Note that to invest four times in a cheap self-select ISA may cost around £6 each trade. The return in the first example would then fall to £865, reducing the returns by 0.2% investment points to 7.3%.

However, with only one trade at £6, our alternative once-annually investment would only fall by 0.05% investment points to 10.85%.

Therefore, in theory, it is beneficial in the long-term to invest the whole amount on day 1.

“Marge, I agree with you, in theory. In theory, communism works.”

The wise words of Homer Simpson. As you will know, I don’t like to rely on theory. Let’s have a look at some numbers: for ease, let’s look at historical data of the FTSE 100 since it opened (1985).

First, the easy part: we always put in the maximum amount on 6th April 2014 and we make two assumptions:

- The maximum investment amount is £10,000 each year. As long as we keep this consistent, it does not matter if this is the exact average over this period – it helps with a comparison.

- Dividends will be obtained proportionally over the course of the year at an annual rate of 2.5%. All dividends shall be reinvested.

Starting on 6th April 1985, our £10,000 annual investment on 6th April each year (or the following Monday), our investment would be worth £933,151.33 today.

As a side note, if you STILL are not convinced to be investing in the market in the long-term, you should note that the same amount invested in cash at an average of 4% would have returned only £529,662.86 – a full £400k less!!

What about if we invested in 4 equal proportions over the year? Using the same assumptions as above, and actual data from the FTSE 100, our investment would be worth £929.077.31.

So, using real data, we can see that we would earn over £4k less over the course of 30 years by dollar averaging four times each year.

Whilst this suggests that investing as a one-off in April is marginally better (although probably not statistically significant enough to make decisions upon), it is nowhere near the 3.5% per annum difference that we cited above (according to the theory).

Why is this? Well, there is a certain saying in the markets:

“Sell in May, go away”

This saying holds a lot of truth and is proven in the following article.

For example, the article notes that “if we had invested £10,000 at the start of October each year, withdrew from the market at the end of April and held our funds in cash in between…our returns would be 12.2% per annum, rather than 8.8% per annum.”

Therefore, by investing all of our funds in April, we are subject to the problems with reduced returns over the summer.

The conclusion thus far is that there is very little difference between dollar averaging and investing everything in April.

Let’s go on…

“But, the market is at a high. I’m scared to invest everything now?”

Fair point. My initial thoughts on this would be:

However, I’m not a fan of trusting initial thoughts, mainly because I’m usually wrong. Instead, this is time for some more number crunching.

This time we perform the following strategy:

- If the market is at an historical nominal high in April, we will adopt the quarterly dollar averaging method

- If the market is not at historical nominal highs in April, we will invest the full amount on the first day of the tax year

In this strategy, our final investment amount is £936,535.13.

INTERESTING!!

By dollar averaging when the market is at historic nominal highs, our returns are £3,500 more than when always investing all our funds on Day 1 of the year.

These samples are quite small and the differences are minimal

The only issue with this analysis is that the sample sizes are extremely small. To improve the analysis, let’s look at S&P 500 data in the same way, going back to 1950.

In brief, if we invested $1000 every year in the S&P 500 index (again assuming 2.5% dividends) since 1950, we would have the following results:

- Invest all in April => $4,039,036

- Dollar average quarterly => $4,100,871

The difference is not huge at $61,834 (1.5%), but over this larger sample size, it becomes more significant.

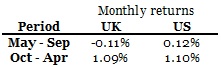

Again, if we investigate why this is the case, the seasonal difference between summer and winter has a large impact:

Returns from October until April return 1.15% per month.

However, returns from May until September only average 0.12% per month.

For these 5 months, even a 2% annual cash return would be 0.17% per month and therefore outperform the market.

And the same strategy if the US market is high

Using the same “dollar average if high, invest now if not” strategy in the US market would return us a total of $4,039,975, which is almost exactly the same as investing everything in April.

Time to summarize again:

UK: High vs low dollar average > April > Dollar average

US: Dollar average > High vs low dollar average > April

My overall conclusion to date is that neither of these strategies outperforms another to make it worthwhile the effort to work out when you should invest!

Is there a better strategy?

From the “sell in May, go away” theory, we have noted two important pieces of information:

Therefore, what about if we put out entire ISA allowance into the market on 1st October every year, instead of 6th April?

For the UK, we would have a return of £928,497 instead of £933,151; under-performing April.

For the US, we would have a return of $3,940,667 instead of $4,039,036; almost $100k less than investing in April.

Why? In both cases, the difference is that the period from April to September in the first year of investment was way above average (6.7% in the UK in 1985 ; 8.8% in the US in 1950). This skews the results somewhat, but raises a very interesting point…

The biggest impact is in the first year; then the second; then…

From these calculations, we can see the huge impact that the first year of returns has on our final outcome. This is because of the sheer power of compound interest has against these first year returns. The second most important year is year 2. And so on…

Therefore, my conclusion is that we need to reduce our volatility in the first few years, but after that it becomes much less important. In summary, I would recommend:

- For the first five years, you should dollar average your ISA investment quarterly

- After that, just invest on the 1st April – the returns will be very similar, the volatility will be around the same over the course of 20 years (I’m assuming you are investing for the long-term). Therefore, you might as well save 15 minutes work every 3 months!

This will also be impacted by your current financial position. All this analysis is theoretically based on the fact that you have the full ISA allowance available in your account today.

Usually, this will not be the case.Many people will receive a one-off bonus which will be used to invest in your ISA. Others will be saving a little each month towards filling the ISA. If this is the case, fine. Follow the rules above when you have the physical cash available to invest.

I hope that has helped you: it has actually helped me. From this, I am now confident that on 7th April this year (the 6th is a Sunday), I will be putting my full ISA allowance into my account, due to already being sufficiently diversified in the market. However, if it was my first year of investing, I would be dollar averaging across the year.

This brings me, finally, to my brand new investing motto (which applies to both ISAs and to matched pension schemes):

Max (your ISA allowance), trax (track leading indices – eg FTSE 250) and relax (don’t worry about your investment for 10-20 years). Easy….

Max, trax and relax!!

Update from the 2014 budget

Since this article was pubished, big changes have just been announced in the 2014 budget. They can be summarized as:

- The overall ISA limit is to rise to £15,000 from July from £11,520

- All of the new £15,000 allowance can be held in either cash or shares

- Savers can transfer funds freely between existing cash ISAs and shares ISAs

Whilst these changes are positive for short-term savers and long-term investors alike, they have very little impact on your method of investing your ISA. Therefore, all the rules above still apply, but you now can “max” £15,000 and this can be held in either a cash ISA (if you are saving for a short-term goal) or a stocks & shares ISA (if you are investing for the long-term).

Leave a Reply