What are payday loans?

For those of you who aren’t in the know (and that might be a very good thing!!) a payday loan is a short-term unsecured loan. The loans are also sometimes referred to as “cash advances” and often rely on the consumer having previous payroll and employment records.

How much do they cost?

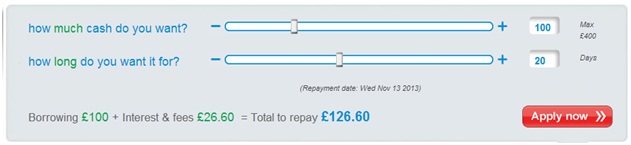

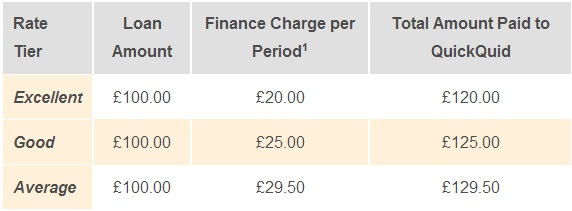

Well, here comes the sickening bit. “Short-term” loans, just enough to get you through to the next payday should be cheap, right? Wrong. Oh my, so very very wrong! Let’s look at some examples of payday loans and how much it costs to borrow £100 for 20 days at some popular payday loan sites in the UK:

Wonga

Moneyshop

paydayUK

quickquid

Equivalent APR

At face value, these payday loans seem expensive. Then again, you may say, its only £20 or £30 to get me out of this pickle nice and quickly, so its money well spent. Well, overlooking the fact that it was this attitude that got you into this pickle in the first place, this £20 or £30 isn’t cheap at all. The most expensive of these payday loans shown above would equate to an APR of 2716%. Compare to the 0-2% APRs currently available on savings accounts, and we can see how expensive this really is!

Is your overdraft a better alternative?

It depends. At Barclays, for instance, if you agreed the overdraft up front, the same lending would be:

So this would only cost £1.02 instead of £20-£30.

If you do not have an agreed overdraft, it costs 19.3%, but you have to pay an £8 per transaction fee. Therefore, if you need to pay 2-3 separate bills to make up that £100, then this could be more expensive than the pay day loan.

Other alternatives – pay advance at work

If you need a small amount to get you to your next paycheck, maybe you could discuss this with your employer or HR department. Advances in pay are not that common, but are possible so it may be worth finding out from HR what the rules are.

Bank of Mum & Dad (friends and family)

How about lending from friends and family? People are often worried about doing this and negatively impacting the relationship. However, let’s say that you are 100% confident that you are paying this£100 back in 20 days (because you wouldn’t be considering a payday loan otherwise). Let’s say you offer to pay them £5 to do so. This would save you £15-£25 if compared to the payday loan, and will save an application form or two.

This is clearly a good deal for you, but what about your friends and family? Well, this represents a 5% ROI to the lender over 20 days, equivalent to a 233.5% APR. So, as an investment decision for your friends and family, this would be a good business deal!

Peer-to-peer lending

Still don’t feel company asking friends and family and the agreed overdraft isn’t an option. Well, peer-to-peer lending may be an option. At zopa.co.uk, for example, you can borrow from other peer lenders from 4.8 %. Although these are not designed to be a short term alternative (minimum loan period is 2 years and the minimum loan amount is £1,000). However, there are no early repayment charges or terms, so if you need a short-term loan borrowing a little more cash, then this could be your option.

Credit unions

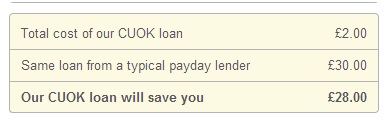

Credit unions in the UK have started to fight back against the pay day loans. Cuonline (London Mutual Credit Union) for instance:

Even cheaper than the made-up friends and family option, but still 26.8% APR!

There is one very small issue!! You must live or work in Southwark, Lambeth, Westminster or Camden in London!

However, you can search for your local credit union as more and more of these are popping up all the time.

So, there are plenty of alternative options. And there is certainly NO excuse for taking out a payday loan. EVER!

What are your thoughts on payday loans? Can you think of any reason why anyone should ever use this service? Should they be banned to, in the words of Ed Miliband, “protect the most vulnerable people in our society from exploitation”.

I think Payday loans should be avoided at all costs – the interest rates are generally horrible. We are lucky to have an overdraft line with our credit union that costs just a few cents a day. Although I hate paying them a buck or two for interest when we use it, it’s sure better than giving them 30%. Great post!

I see NO REASON to use them, I’d stay away from them as much as possible. I’d rather borrow money from friends/family than take such a loan.

I would personally never use them, but I have options – cash, credit, overdraft, friends, family… I can see how payday loans are attractive to people who don’t have any other resources to fall back on, but they’re such a bad option.

Using payday loans is among the worst financial decisions you could make these days. The interest is just crazy

These Payday Loan outfits are real shysters. No one should fall for what they offer.

I used payday loans twice and never again!! I think here (in Canada) the rates are even higher! 🙁

Banned for good! I’ve never even thought of taking out a payday loan. Luckily, my family has always been there for me. Whether it’s a good thing or a bad thing I don’t know, but it’s way better than considering a payday loan. An APR of 2716%? Are they for real?!?!

Payday loans are a recipe for financial disaster! Credit cards are a way better option since they give you a bit of flexibility and their rates aren’t as usurious as those of payday loans shylocks.

If all goes south…eat the humble pie, Mom & Dad bank is a better option, and more often than not they are interest free!

I am so glad you posted this because many people think a payday loan is a good fix when you are in a jam. Most people fail to realize it actually cost you way more to pay it back. Great post.

Payday loans are not a solution to money problems, and can often leave people in a much worse situation. They take out a payday loan, then have to use another to cover the repayment, leading to a vicious cycle that they can’t escape.

There is another alternative to payday loans though – Smartloan are much more affordable and allow people to pay back in monthly installments, which is much better than having to pay it all back on the next payday. It’s a cheaper alternative, and helps stop people getting into trouble.

I have tried using payday loans and my experience was not good because of my credit scores and lots of documents needed. I think credit union is better because it has has no annual fee credit cards with cashback rewards and it is easy to qualify for their fee waiver and highest tier of checking services.