After signing up to Funding Circle 8 months ago, we take a look at our performance to date in our Funding Circle review. We also investigate the benefits of having a peer to peer NISA.

At the end of November 2013 – 8 months ago – we started our investigation into peer-to-peer lending and peer-to-business lending, specifically looking at the peer-to-business lender Funding Circle:

We previously stated that we would “put our money where our mouth is” and invest £1500 into Funding Circle to see what the experience was like and judge our actual results.

We previously stated that we would “put our money where our mouth is” and invest £1500 into Funding Circle to see what the experience was like and judge our actual results.

Today, we revisit this post with an update of our experience with Funding Circle.

Before reading on, I would advise you to revisit (or read for the first time), our previous article which outlines the theoretical benefits and potential risks of investing in peer-to-peer lending.

Peer-to-peer lending experiment

Let’s get straight into it then…

Funding Circle Review – gross yield

The gross yield that I obtain through Funding Circle is the annualized interest rate that I’m earning from my loans, before fees, bad debt and tax are deducted. This is effectively the average of all my loans that I’ve selected.

My gross yield for the first 8 months (annualized) is 9.6%. Whilst this number is interesting, it is more of a headline figure as it does not include fees and bad debt, and is therefore not comparative with other savings or investment rates.

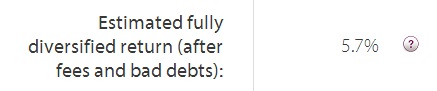

Funding Circle Review – estimated fully diversified retunrs

The second figure that I am provided is my “fully diversified” return. This shows the return I would earn if I experienced the average annual bad debt rate for each risk band, based on the investments I have selected.

It is calculated by taking my average bid rate, deducting the 1% annual investor fee and removing the average estimated bad debt for my portfolio. It is an estimated annualized return before tax and assumes you have a fully diversified portfolio lending to over 100 businesses.

With my £1500, I am currently investing to 92 businesses (with no single exposure to any business of greater than 2.4% of the total amount lent). Therefore, this is an important number to consider:

My estimated fully diversified return is 5.7%. This is the average return that I should be earning based on my selected loans. It’s an interesting figure for comparison, as it represents what should happen over the long-term. Its weakness, however, is that it is only an average rate and isn’t representative of what is actually happening in my portfolio.

Funding Circle Review – Annualised return

This is the key figure. The actual return is a percentage, calculated to show the annualized return I have earned after fees and bad debt, but before tax, since you started lending at Funding Circle.

Woohoo! My actual return rate is higher than the average. Is this luck? Maybe. However, in the tips below, I analyse some actions that I have taken which I believe are contributing to my higher rate of return.

6.2% annual return is impressive. A quick check of my actual figures show that this figure is representative of my actual returns.

After 8 months, I have £1,561.88 in my account, having started with £1,500.

The £61.58 gain over 8 months, divided by £1,500 and then multiplied by 12/8 to make it representative of a full year gives me 0.06188 or 6.18%.

Comparisons

6.18% is impressive. However, to determine just how good it is, we need to compare it to some other “savings” or “investments” rates on the market.

Easy Access Savings Rate: The best easy access savings rate on the market is currently 3%, with Santander 123 account. However, this is based on a minimum savings amount of £3,000 and monthly deposits of £500 per month. You also need to pay a £2 monthly fee. If we are trying to find a match to our Funding Circle account (a one off investment of £1,500), then the Britannia BS savings account rate of 1.4% is the best comparative. This requires a minimum investment of £500. Whilst our return with Funding Circle of 6.2% is clearly much more favourable than this, we need to remember that this account offers us easy access to our funds, whereas Funding Circle is a little more complex if we need to get our cash back in a hurry.

Fixed Term Savings Rate: Therefore, a more accurate comparison may be with a fixed term saving account. In fact, this is the closest comparison (in my opinion) to the Funding Circle investment. I am not able to see the average length of the loans I have selected, but based on my experience, I would say that it is somewhere between 24 and 36 months. To be conservative, I will say it is 36 months or 3 years. The best 3 year fixed savings rate is 2.7% with ICICI Bank with a minimum required investment of £1,000. Therefore, Funding Circle is currently returning over double that of its comparative account in fixed term savings (based both on my actual returns and the estimated average returns based on my lending selection).

NISA Savings Rate: Despite an announcement in the 2014 budget that peer-to-peer lending would be allowed in NISA accounts in 2014 (new ISAs introduced in the 2014 budget with an annual limit of £15000). However, this is not yet the case. Therefore, we need to currently pay income tax on our rates above. Assuming you are a standard rate tax payer, this will mean that the 6.2% return suffers a 20% tax reduction, leaving your actual return at 5.0%. Therefore, this is the rate that we should compare to ISA rates. The best easy access cash NISA account currently returns is 1.5% with the Halifax. However, once again, the better comparative to make is with the 3 year fixed rate NISA of 2.25% with Aldemore. Therefore, once again, the Funding Circle investment is over twice as attractive as the NISA equivalent. Once peer-to-peer lending is included within ISA wrappers (expected later in 2014) this will become even more attractive.

In conclusion, peer-to-peer lending rates are currently trumping the equivalent rates in the banks.

Peer-to-peer lending – The Risks

As the old investment saying goes: greater risk greater reward. Therefore, with returns of over double the equivalent bank savings rates, there must be some additional risks. Let’s consider them:

FSCS guarantee: This is a guarantee provided by the government through the Financial Services Compensation Scheme which means that your first £85,000 of savings is backed by the government. This means that if a bank goes bust, or otherwise runs into financial difficulties, you will not lose your money. Peer-to-peer lenders are not currently supported by the FSCS.

However, the good news is that if Funding Circle was to go down the pan, you probably wouldn’t lose your money anyway. When you lend money through Funding Circle, you are lending money to another business. Therefore, if Funding Circle went bust, then this other business still owes you your money. The only thing that has changed is that the intermediary (Funding Circle) who is collecting your cash would no longer be there. However, all the big peer-to-peer lenders have plans in place to take over the collection of funds of another peer-to-peer lender if they were to go bust.

Therefore, while there remains a risk that this could go wrong, in theory you should be fine.

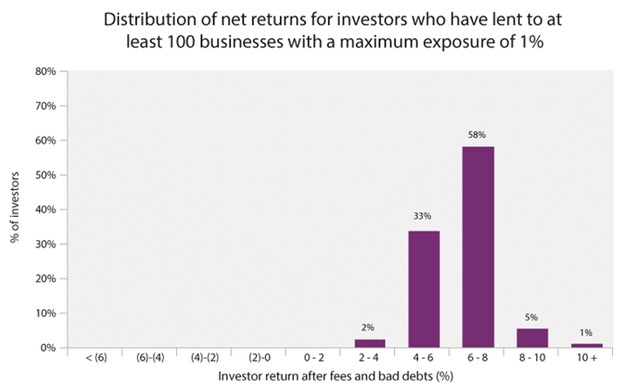

Guaranteed returns: In our banking example, our returns are guaranteed – we are always going to receive the headline rate of interest on our fixed term deals. This cannot be said for Funding Circle. However, with a diversified portfolio of loans, I don’t see this posing too much of a risk. Funding Circle has an excellent statistics page, outlining the long-term averages of everything.

This graph, the most interesting on the page, shows the investor return after fees and bad debt assuming that the lendor has evenly split their investment over at least 100 different businesses. 98% of all investors doing this will obtain a return of over 4%. The remaining 2% will obtain a rate between 2% and 4%, which is still better than the equivalent bank rates.

Therefore, whilst there is a risk that your return may not always be the advertised long-term average, it will always be better than the savings equivalent. With my £1,500, I am currently lending to 92 businesses, so I am fairly confident that my return will be positive.

Also, if you apply some of the tips below, you will be pretty guaranteed to find yourself in the 6%+ bands.

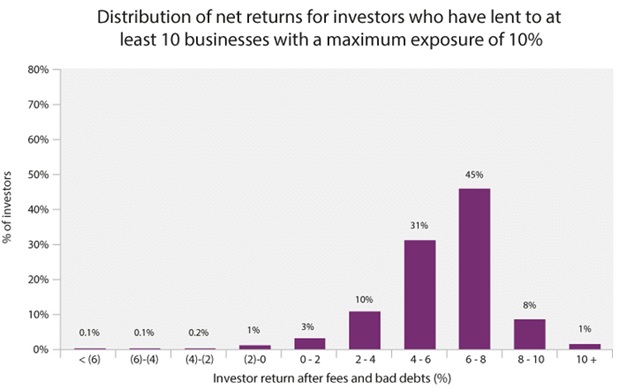

However, as always in investing, diversification is incredibly important. Just look at the equivalent graph if investors split their investment between only 10 loans:

Here, 1.5% of investors actually earn negative returns from their investments. Be warned – diversification is key!

Increasing your returns – top tips

With the bank savings rate, you will earn that rate whatever happens. The beauty of Funding Circle is that, with a bit of work, you can obtain returns better than the average. By applying some of these tips, I have been able to obtain an annualized return of 6.2% instead of the average of 5.7%. This is 5 percentage points higher, or almost 9% higher than the average.

1) Analyse the business: for every loan request, there is a mountain of information. Funding Circle provides a lot of key information on the business, including:

- Years trading: look for businesses with a long and successful history

- Loan purpose: ideally you want to avoid reasons which suggest that the company is struggling to meet debt obligations or having issues with cash flow

- Director guarantee: loans can be guaranteed by the company directors which makes it slightly more likely that you will get your money back if the company goes bust

- Asset security: loans can be supported by underlying assets, again increasing your chances of getting something back if something goes wrong

- Business profile: the company provides a business profile – this can often give you an understanding of what the business is about and why they need a loan

- Credit score: a positive credit score will mean it is more likely that the business meets their repayment obligations

- Financial summary: these businesses often provide the past 3 years of accounts. This can be fairly complex if you don’t know your accounting, but finding businesses with positive cash flows, and strong balance sheets will greatly reduce the chance of bad debt

- Q & A: want to know more? There is a section where you can ask specific question to the company directors – this is usually where you find the best info!

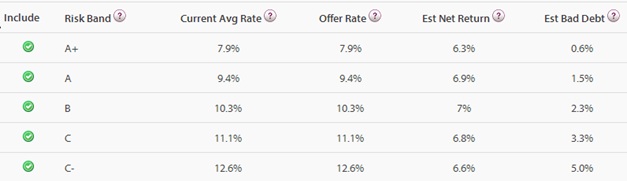

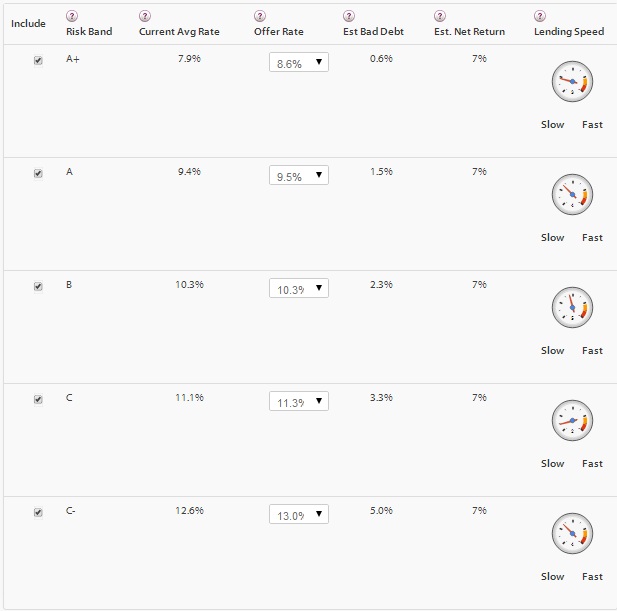

2) Higher risk, higher reward: Funding Circle follows the general rule of investing. Businesses are rated from C- to A+ based on some of the factors above, but principally on their credit score. The “Estimated Net Return” column is based on the Offer Rate, less a 1% fee, less the estimated bad debt rate:

From this table, we can see that the estimated net return for B to C- loans is higher than that for the A+ and A. But are they really more risky? The bad debt rates have already been applied to the gross yield, and the only other worry is variance. However, if you follow the aforementioned rules of diversification, you can easily minimize this variance.

3) Autobid: This can be both a way to improve your returns and a way to minimize your efforts. The table above is taken from my autobid page. The “Offer Rate” can be set at any individual percentage so that you will bid on all loans that have a rate higher that the level set. This obviously saves a lot of time selecting individual loans, but also overlooks the detail of the loans.

For example, if I wanted to guarantee a higher estimated return, I could only bid on loans which would provide me with an estimated return of over 7%:

However, as you can see on the right hand side, this will slow down the rate at which my funds are assigned (as I will only be bidding on certain, specific loans above the threshold I have set). Therefore, this is somewhat of a balancing act.

Increasing your returns – the hidden secret!

And now for the finale…

This is not a tip I have seen elsewhere, but is one that I believe really can lead to higher returns. It is possible in Funding Circle to sell your existing loans to another party. There may be a variety of reasons for doing so, but the most common is that the lender needs access to their funds and wishes to liquidize their investment.

To do so, the lender must sell each of their loans individually through the “loan parts” menu. The seller can charge a premium, and most do. However, people in need of their funds often forego this premium in order to make a quick sale.

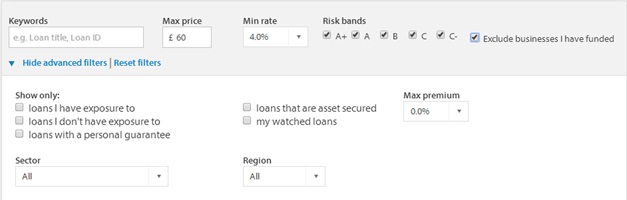

There are filters you can apply to find these types of loans. Let’s say I have £60 to apply to one loan. I add £60 into the filter, leave all risk bands (A+ to C-) selected and set the “max premium” option in the advanced menu to 0.0%. I will also exclude businesses I have already funded, so that I keep my diversification:

This then provides all loans available for this filter. I sort by rates available and note the following for each rate band:

We can then compare these to the current average return rates:

- The C- loan is equal to the average return

- The C loan is above the average return

- The B loan is below the average return

- The A loan is below the average return

- The A+ loan is above the average return

However, there is also another key indicator which you must investigate. Notice that for the A and A+ loans, there are 428 and 708 parts available. In my experience, any number greater than 10 usually indicates that there is currently an issue with the lender.

Finally, notice the number of months remaining. If you can select a loan which has a repayment history of at least 6 months, this is likely to reduce the chances of the business not meeting their repayments.

So, my criteria for selecting loan parts are:

- Rates available less the premium should be higher than the average for that band

- The parts available should be less than or equal to 5

- The repayments left should be between 1-6, 13-18, 25-30, 37-42 or 49-54.

Out of the examples above, I would probably opt for the C as there is only one part available, the return is favourable compared to the average. The only downside is that it only has 3 months of repayment history. However, the detail (which you can review by selecting the loan) has nothing to indicate that it will not be repaid.

Peer-to-peer NISA

The first, and in my opinion, the most significant change is the possibility of placing peer-to-peer lending into New ISAs (NISAs). This will mean that any interest earned from your investments will remain tax free. This effectively increases your investment returns by either 20%, 40% or 45% depending on your current income tax rate. For my current investment, I’m earning 6.2% returns on my peer-to-business lending. However, after tax this falls to only 4.2%, which whilst still attractive compared to current saving;s rates, but less appealing than if this wasn’t taxed. Additionally, you will save the hassle of filling out a tax return:

Currently, we are not 100% sure when NISAs will begin to accept peer-to-peer lending, but it is expected to sometime in early 2015. Equally, we envisage that you will be able to simply transfer your existing peer-to-peer investments into an existing ISA and it will form part of your total £15,000 allowance:

Peer-to-peer lending conclusion

This is a innovate sector of saving/investing, which is becoming more and more regulated and increasingly “mainstream”. I greatly favour lending to businesses compared to individuals (again, see my introduction to peer-to-peer lending post for an explanation why).

My returns have been 6.2% annualized for the first 8 months, which greatly exceeds any other saving product on the market (fixed term or easy access, ISA or non-ISA) and I would judge that the level of increased risk is more than compensated for by these higher returns.

If you are interested in saving with Funding Circle, you can visit the site directly via this link or via the banner below to sign up today:

If you found this information useful, I would be hugely grateful if you could share with your friends and colleagues on social media:

[cunjo layout=”inline_buttons”]

An excellent and informative post – thank you! I wasn’t sure how the loan parts of Funding Circle worked but you’ve made it really clear. I currently have two peer to peer loans out, with Ratesetter and Lending Works – average rate is 4.6%, which isn’t as good as the rate you’re achieving but still beats the banks/savings accounts.. I intend to invest in Funding Circle later on in the year, using repayments and interest from my other p2p loans.

I can’t wait for them to be part of NISAs so interest received is tax-free!

Great review! I’ve been looking for some more insight into Funding Circle and this is by far the best article I’ve found. Thank you!

Point for investors: according to the law Companies paying any form of interest should deduct tax at 20% (declared via a CT61) before paying investors any money. Funding Circle see this as a grey area at the moment and are not enforcing their borrowers to do it. With the figures increasing HMRC is bound to act soon to recover these monies and will no doubt look at the borrower and lender. Buyer beware

Mr. A. Thanks for stopping by, and really appreciate the comment.

What impact would this have on the lender? Is this not just a difference between having tax deducted at source and declaring it at the year-end?