A new breed of “robo-advisors” are popping up and have been a great success in the US. Now, they have made it over to this side of the pond and InvestYourWay have teamed up with IG to bring you a reputable and impressive investing service.

Through my work at moneystepper, I speak to a lot of personal finance bloggers and advisors in the US. From a personal finance perspective, the US has a LOT of problems and issues that we would not want to copy (but unfortunately we seem to be copying them in many of these areas).

For instance, the average household carries more than $15,000 in credit card debt, equivalent to just under £10,000. The UK equivalent is less than £6,000 in the UK.

The total in the UK it is only £55,000, equating to £28,900 per person, which is approximately 116% of the average annual earnings per person. This seems pretty bad, right? Well, it’s nothing compared to the US. The overall total debt per household in the US is over $200,000.

However, the US personal finance world does have three things that I wish we had over this side of the pond:

- Fixed rate mortgages over 15 years at 2.99% APR or over 30 years at 3.8% APR. Yes, the interest rate is locked at that rate for the entire mortgage period!

- com – mint is an excellent free website and series of apps which allow users to manage their finances in a remarkably efficient and effective way. I’ve not yet found anything that matches it in the UK.

- Wealthfront. Personal Capital. FutureAdvisor. These are better known as “robo-advisors”. You put your savings into an account, set a timeframe and risk tolerance, and they propose a diversified series of investments with analysis on how they have previously performed and all manner of other information. You can then invest, diversify and rebalance all within minutes.

The first of these isn’t coming to the UK anytime soon. We saw some 5 year fixes on mortgages, but these have absurdly high fees and are fixed at rates well above the 2-3 year fixes.

For the second, I recently found “Toshl” as part of my personal finance apps review, but this still doesn’t really cut it.

However, for my third wish, it seems that the genie has granted it! Let me present: InvestYourWay.

What is InvestYourWay?

Essentially, InvestYourWay is an online account where you can deposit money and then use their program to determine how you would like to invest this money. You can build one, or several, “funds” which are individual and unique to you. You can then very easily rebalance your portfolio at no extra cost at a simple click of a button.

What are the fees?

This is always the most important thing about these types of products. The fees almost always determine whether these services are worthwhile. Luckily, the fees and minimums are very clear at InvestYourWay. You are charged a one-off management fee of 1% of any money that you have in activated funds. This is split between both InvestYourWay and IG.

You are also charged a spread on transactions, but this is unavoidable in investing. InvestYourWay strive to keep this to a minimum and is simply a pass through of costs incurred, so they have no incentive or way of profiting from this.

1% initially may seem quite high when compared to ETFs (the lowest of which charge in the region of 0.1-0.2%). However, when you think about the range of ETFs which go into your “fund”, to find the equivalent, you may have to pay around an average of 0.5% if selecting the individual ETFs. Also, you do not incur any trading costs (most online platforms will charge a one-off fee for making a trade) with InvestYourWay. Not only do you pay this elsewhere for buying/selling, you would need to pay it to effectively rebalance your portfolio.

Therefore, the 1% fee (especially give the facts in the “is it safe” section below) may be worth it to you.

Who can invest with InvestYourWay?

Anyone. The minimum investment amount is only £2,500 (€3,000 or $4,500). This is much lower than you will often find elsewhere.

Who should invest there? My advice would be beginners who need help diversifying their portfolios (and want to benefit from the FSCS guarantee) and anyone who rebalances their portfolio on any basis less than annually (which should be most people).

Is InvestYourWay safe?

Very. All client money is actually not held by InvestYourWay, but by a much more well-known company, IG, who trade on the London Stock Exchange and have a market cap of £2.35bn. Not only this, but your investment is held in segregated funds and is protected by the Financial Services Compensation Scheme (FSCS), which means that your first £85,000 of investment is guaranteed.

This actually makes it safer than investing directly in ETFs as these are not protected by the FSCS scheme.

Other perks of InvestYourWay?

There are many. When I first came across this service, I scoured the terms and conditions to find something that would trip them up. Some hidden fees. Some minimum terms. But, all of what I came across was actually positive:

- No minimum investment period

- Possibility to hedge currency risk with accounts in GBP, EUR and USD

- Check your investments on the go with their apps

- Same day withdrawals.

What are the downsides?

For me, there is only one. Unfortunately, it might be a bit of a biggie for new investors.

Whilst Betterment in the US allows investments from 401k accounts (equivalent of pensions) and IRAs (equivalent of ISAs), InvestYourWay offers no such service. Therefore, it is not possible to invest your stocks & shares ISA with InvestYourWay.

What is the impact of this? Well, it means that you will be paying income tax on dividends and capital gains tax on the growth in your fund at your standard tax rate.

Therefore, whilst we would highly recommend the service, we only think it’s suitable for people looking to invest their money into stocks, shares, bonds, etc after they have already maximised their £15,000 contribution into their stocks & shares ISA.

Can I get a sneak preview of InvestYourWay?

You certainly can. InvestYourWay offers a free demo of their service (where you have £50,000 imaginary pounds to create your funds), so you can see exactly how the product works. Check it out by visiting InvestYourWay and all you have to do is enter your name and email. I hope you are impressed as I was.

You’ll see some screenshots below of a demo fund that I created in under 2 minutes. First set your name of your fund, investment amount and number of years you wish to invest over:

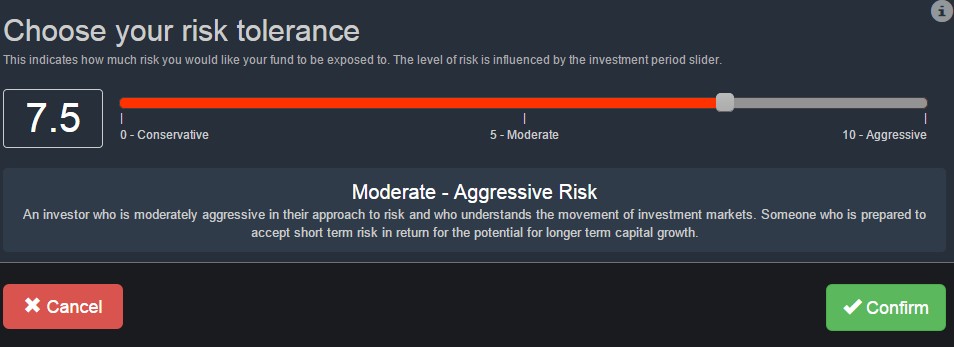

This will set a limit on your risk tolerance. For instance, if I choose 2 years, it would only let me select a very conservative risk tolerance. I chose 10+ years and hence had the full scope to select from:

This will set a limit on your risk tolerance. For instance, if I choose 2 years, it would only let me select a very conservative risk tolerance. I chose 10+ years and hence had the full scope to select from:

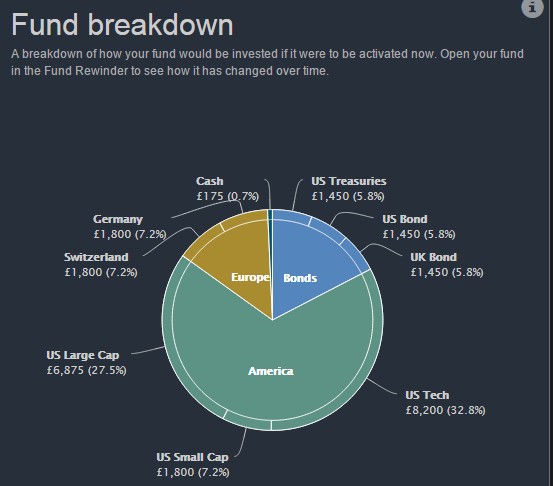

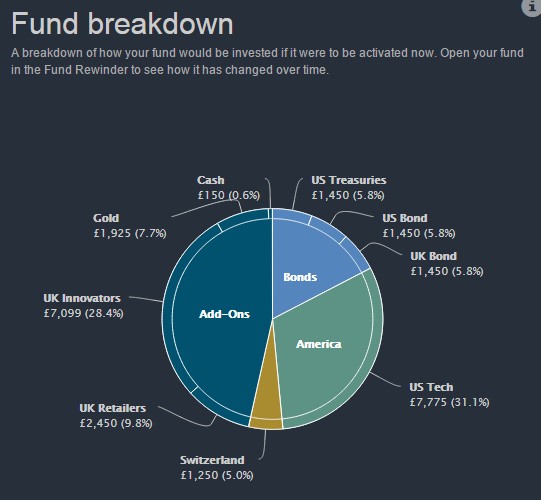

InvestYourWay then proposes a breakdown of funds:

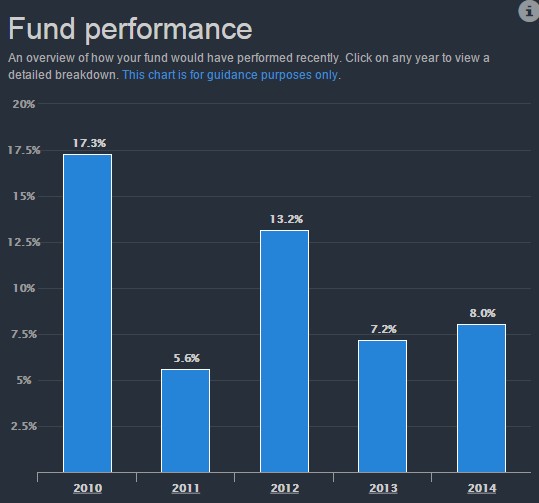

You can see this includes American stocks, European stocks, US treasuries (cash), US and UK bonds. We can also see the performance of these investments in the past:

Think you are missing something? Then you have the option to “add-on” specific investments, commodities or sectors:

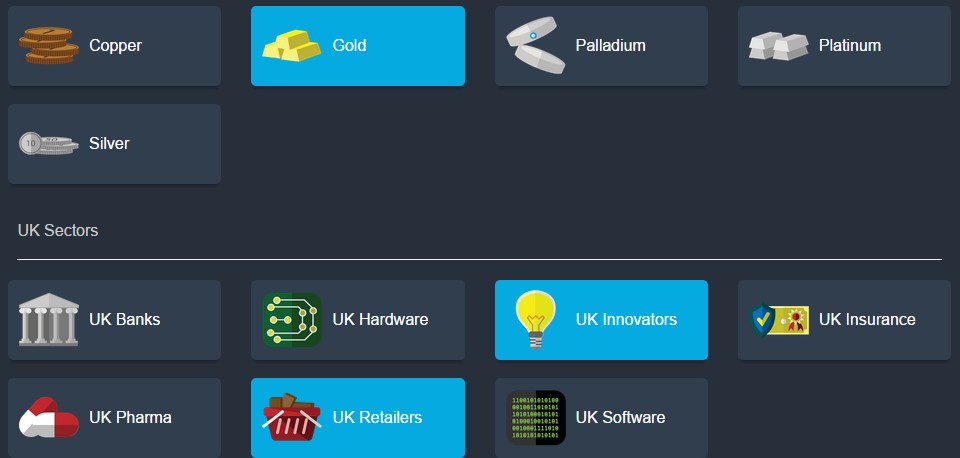

We decided that we are missing some UK equities (and want to increase our risk profile a little so select UK innovators, UK retailers) and we also want some exposure to gold – PLEASE NOTE THAT THIS IS FOR EXAMPLE PURPOSES ONLY AND IS NOT INVESTMENT ADVICE:

This then changes our split of investments and it’s historical performance:

As I say, the demo is completely free, so feel free to have a play around and create some sample funds. If nothing else, you might learn something about historical performance of certain commodities or funds.

Enjoy!

[cunjo layout=”inline_buttons”]

I would say the fact that you can’t have a tax deferred account would be an issue for most people.

Yeah, its a real shame.

However, once you pass the ISA limit for investing, then this could be a great place to look. Their problem is that now the limit has increased to £15,000, not a huge number of people will be investing beyond this amount.

Yea, I second this. Otherwise, seems like a great tool.

It looks and sounds very similar to Nutmeg whom I have an account with. InvestYourWay has a nice UI, will give the demo a go myself. Liking the historical performance charts too. Would it be something you would personally use as an alternative investment strategy?

As the article says, the key factor stopping me is that I cannot invest within a tax-wrapper. I’m currently deciding what to do with my savings that are above my £15k ISA limit and this is definitely part of my options. However, this year it is probably going into property. This is something that I think InvestYourWay need to address to be successful.

Nutmeg is a great alternative. Similar fee structure (although they also have fees for investing in the underlying ETFs which can make them slightly more expensive than IntestYourWay – depending on your investment amount). However, Nutmeg has the huge advantage that you can invest in a stocks and shares ISA account at no additional cost!

Nutmeg are even working on opening a pensions option which would be very interesting for me personally…

However, it is worth pointing out that the same can be done (including re-balancing if you are continually investing into the market) for lower fees and charges by doing this yourself with a low-fee broker and low-fee ETFs. The difference is the effort you are willing to make to manage your own finances.

Actually the mortgage interest rate in US varies. We got a 30 year mortgage this @ 4.125% and the rate is going up at this time. Also there are many personal finance tools that you can use in UK, like Yodlee.

Maybe I misunderstood the US mortgage market. So your 4.125% fixed rate that you pay on your current 30 mortgage could change every year, or is it fixed for the 30 year period?

Thank you for the great article and feedback, I am glad you liked the platform. As we went for a pan-European launch covering 30+ countries the ISAs did not get included in the first release. ISAs are specific to the UK but are still important to us and will be addressed in the near future. It is however worth remembering that savers in the UK still receive their first £11k of profit tax free due to the capital gains tax relief, a relief which few take full advantage of. Also any losses cannot be netted off against other investments, such as property, which means people using ISAs can end up paying more tax during the hard times. ISAs are indeed a fantastic product but it is worth bearing these points in mind.

For us the issue really comes down to one of choice. Nutmeg is a great service but is unfortunately limited in the fact that they only have 10 funds to put people into. So if I’m a 7/10 and you are a 7/10 on the risk scale then we end up with an identical solution, despite the fact that we are different people with different needs and aspirations. Many people are happy with this generalised solution, after all it is what finance companies have done for decades. We just feel that people deserve a personalised service, no matter who they are or how much they are looking to invest.

Great comment Michael, and very good points.

One point that your comment addresses that we didn’t cover in the article is capital gains vs dividends. When we create these “funds” with InvestYourWay, are dividends automatically reinvested. How would this affect people from an income tax perspective if they don’t have their investments in ISAs?

Good point on the amount of choice at Nutmeg vs InvestYourWay. I was very impressed with the “add-ons” offered to allow a little flexibility for those who wanted it within their funds and I hope this comes across in the article.

Keep up the good work!!

It’s a good point. Dividends are automatically re-invested. As we manage each fund individually a large dividend credit would actually cause your fund to rebalance immediately. This is in contrast to waiting for the next rebalance cycle as you might have with a traditional fund manager. The dividends themselves would normally come under income tax though it would of course depend on personal circumstance, local tax rules, etc.