In Question 21 of the Moneystepper Q&A Podcast we answered the question: “what stops people from investing”? Today, we present our complete guide highlighting the 10 steps to the best long term investing strategy for UK investors.

I’d recommend that you listen to the podcast episode here:

Question 21: What Stops People From Investing (Moneystepper Q&A Podcast)

We concluded that there was actually several reasons including, but not limited, to:

- Lack of Understanding

- Fear of Fear Itself

- The Media

- Being Overwhelmed

- The Advice Gap

- For Good Reasons

- Due To Better Opportunities

Today, in our best long term investing strategy guide, we address all of these points. This will provide you with a template to long term investing, specifically focussed on stock market investing. It will be applicable for 99% of people in the UK:

The best long term investing strategy guide is broken down into 10 areas you need to consider.

- Understanding What Constitutes An “Investment”.

- The Emergency Fund

- Paying Down Debt IS An Investment

- Diversification

- Passive vs Active Investing

- Stock Market Investing Vehicles

- What To Invest In

- How to react when markets fall?

- Dollar Cost Averaging

- Mixing Investments For Short Term Goals / Emergency Fund

Depending on where you currently stand on your investing journey, some of these sections may be more relevant than others.

However, I’d recommend that everyone reads each section. Even experts will learn something from each of them.

1. Understanding What Constitutes An “Investment”

The official Oxford English Dictionary’s definition of the word investment is:

“The action or process of investing money for profit”

That is helpful. It tells us that investment is an action, not an inaction. It’s also about investing money, and our goal is profit. However, the word “investing” in this sentence still requires more definition.

Again, from the Oxford English Dictionary:

“Put money into financial schemes, shares, property, or a commercial venture with the expectation of achieving a profit.”

Now we’re talking! We now have a definition of some things that constitute investments. Financial schemes, shares, property or a commercial venture. Again, note that investing assumes that we are trying to achieve a profit.

I’m not being particular about this definition for no reason. I’m trying to make a point. Money itself is not an investment. For anyone who does not yet invest, this is a very important lesson to learn.

As the definitions above state, it is only an “investment” when the money is put into action in order to profit.

Money (cash) is not itself an investment. Instead, it should be best viewed as a store of value and a tool for exchanging value.

It is something that you have in the short-term which you need to apply to investments in order to profit.

Whilst it does “hold value” better than many investments (as your return – usually a fixed interest rate – is guaranteed), it’s important to remember that after inflation, cash actually loses relative value over time.

Not convinced? This video might help:

Conclusion: Cash is not an investment.

2. The Emergency Fund

One very useful trait of cash is that it is liquid. In investing, the liquidity of an asset is generally considered how quickly it can be turned into cash. Cash is uniquely liquid because it is already…well…cash!

Why is this important?

The importance of liquidity is more apparent when thinking about an investment that is not very liquid:

Example:

Say that 100% of your money is invested in a house. Then, your car blows up. The mechanic doesn’t take payment in houses, and therefore the only way to pay him is to sell your house for cash, and then use the cash to pay the mechanic.

It is for these instances where cash, whilst not being an investment, is extremely useful. It is a good idea to keep enough money kept in cash, instead of invested, so that you can pay for emergencies when they arise. We call this your “emergency fund”.

It is generally advised that people keep anywhere between 3 and 12 months of budgeted expenses in cash as their emergency fund.

At Moneystepper, we don’t think it is as simple as that – sorry. Instead, your emergency fund amount will be dependent on a huge number of factors, including:

- What you budget for?

- What access you have to other sources of completely liquid finance (e.g. credit card limits)?

- Number and nature of dependents

- Your current net worth

- How liquid your other investments are?

For more reading on how much you should keep in your emergency fund, you can refer to any of the articles below from Moneystepper that will help you more on the subject:

Emergency Fund Articles:

Emergency Funds: An Alternative View

Emergency Funds For People In Debt With A Good Credit Score

Emergency Funds For People In Debt With A Bad Credit Score

Emergency Funds For People Who Are Not In Debt

Cash should also be used when you are saving for a short-term objective and other investments are determined to be too risky. As a crude example, say you need to pay your rent of £500 at the end of the month. If you only had that amount in cash, investing it in anything where the £500 might be worth less than that when your rent is due would be insane.

Conclusion: You need to keep a cash emergency fund. The amount you keep in this fund will depend on many factors.

3. Paying Down Debt IS An Investment

This is an extremely important concept to understand. People often make mistakes here at both ends of the spectrum. We’ll show you via two examples:

Example 1:

Imagine that you have £1,000 in cash today earning 1% interest. You also have £1,000 credit card debt on which you pay 25% annual interest. You have two options:

- Do nothing. At the end of the year, your cash is worth £1,010. However, you now owe £1,250 on your debt.

- Pay down the £1,000 debt with your cash. At the end of the year, you have £0 cash, but also £0 debt.

From a mathematical perspective, you are £240 worse off in the first option compared to the second.

Looking back at our definitions of “investing”, in option two you have “put money into a financial scheme (the scheme to pay down your debt), with the expectation of achieving a profit (you have profited £240 compared to the alternative)”.

Therefore, paying down debt should be classified as an investment, and should therefore be considered in the same conversation as all other forms of investment.

However, people also go too far the other way and simply place paying down debt as a higher priority than investing because they consider them to be different things.

Example 2:

Imagine that you have a mortgage on which you pay 2% interest. You also have an employer pension whereby if you invest £1000 in January, your employer will match your £1000 investment. Your total investment will then earn 10% a year.Paying down the debt by £1000 in January will save you £20 in the year (2% on your original investment).

However, if short-term variance is not an issue for you, using your £1000 to invest in your employer’s suggestion would earn you £1000 in the employer match and then an average of £200 in the year (120% on your original investment).

Some argue that by keeping debt rather and investing, you are ignoring risk in the equation. However, as long as you understand the variance involved (we’ll expand on the idea of “variance” a bit later) you would be foolish to ignore all the mathematics due to a non-quantifiable risk.

Conclusion: Always compare “paying down debt” as one of your investment options. On higher interest debt, paying it off will usually be the best investment option, but it’s always important to analyse it against other options.

4. Diversification

Diversification is most appropriately summarised by the old saying: “don’t put all your eggs in one basket”. When it comes to investing, it is a very important idea.

Example:

One type of under diversification is company risk. Let’s say you work for SUCCESSFUL PLC. They pay you your salary. Also, they offer you shares in the company, which can be bought today for 10% of the market value, and then sold after 2 years for the market value. This seems like a great deal. Where else will you be able to get a 1000% return in two years? So, you put all of your money into this scheme.However, the company is then taken over by MISERABLE FAILURE PLC, and the business goes into liquidation in a few months. What happens? You’ve lost all of your invested money AND you’ve lost your job.

This is why diversification is key.

In this section, I want to explore asset class diversification. This is a type of diversification that is completely ignored by many investors (both beginner and expert).

Within each of your investments, you’ll have to consider a huge number of risks. For instance, when investing in stock markets, you’ll need to explore the concepts of market risk, company risk, sector risk, country risk, credit risk, political risk, etc, and how you can diversify against them.

However, look a level above that. Before you start your investing journey, you need to consider “asset-class diversification”.

Your investments (for 99% of people) will generally be split into the three classes from the definition in section 1:

- Property

- Shares

- Commercial Ventures (Small Business)

Most people are usually HUGELY over-invested in one of these specific classes. Most commonly, the over-invested asset class is property.

Example:

Take a first time house buyer. They have decided that, after paying down their debt, they are going to pile all of their savings into a 10% deposit to buy a £300,000 house.They’ve saved £30,000 for the deposit, and another £5,000 to cover the expenses of moving house (legal fees, searches, surveys, new furniture, etc). They have £1,000 left in the bank (for emergencies) and are super happy with their new home.

Let’s take a look at their balance sheet:

- Assets – House – £300,000

- Assets – Cash – £1,000

- Liabilities – Mortgage – £270,000

- Net Worth – £31,000

They now have 967% of their net worth in one asset class.

What happens if they lose their job and can’t pay the mortgage? That’s not good. More problematically, what happens if the housing market falls by 30% in the next 6 months, and then they lose their job?

Their revised balance sheet becomes:

- Assets – House – £210,000

- Assets – Cash – £1,000

- Liabilities – Mortgage – £270,000

- Net Worth – (£49,000)

They can’t pay their mortgage. The £1,000 cash quickly runs out. Selling the house would leave them £60,000 short on their mortgage repayment. A nightmare scenario. But, a scenario that many house buyers found themselves in around 2008 and will do again.

Equally, small business owners often plough everything they have into their small business venture with little regard for diversification across asset classes.

Conclusion: Ignore asset class diversification at your peril!

5. Passive vs Active Investing

It’s important to make a distinction when we think about investing between “investing” and “a job”? This sounds silly, but it’s a divide that many investors overlook.

Simply, investing should return profit without it taking up your resource of time. If it takes time, you are effectively trading time for money, which makes it a salary.

There is nothing wrong with it being a salary, as long as you know this is the case.

Example:

Say you spend 5 hours a month managing a property portfolio instead of paying a property manager. However, you save yourself £300 a month in property manager fees. In both scenarios (with or without your property manager), you have a base investment which gives you returns on your investment without any work.However, for the 5 hours work you do a month which saves you the £300, you are effectively working a job which pays you £60 an hour.

This is a very important concept when it comes to investing in the stock market.

Investing can generally be split into three options:

- You can invest passively through market tracking ETFs and index tracking funds (more on those later). These require very, very little time and effort on your behalf and you pay very low fees.

- You can invest actively where you try to pick individual stocks in order to achieve better returns than the market tracking ETFs. Whether this will be successful will depend on whether you can beat the market AND how much beating the market is worth to you for every hour of effort you spend picking stocks. Stock picking is now your job!

- You can pay someone else to pick individual stocks. Professional fund managers “should” have a better chance than you in picking winning stocks. However, as evidence shows, this isn’t necessarily the case. The success of this approach will be whether the fund managers can outperform the market tracking ETFs by more than the fees that you pay them to do so.

At Moneystepper, we are strongly in favour of the first option: passive investing through low-fee market tracking ETFs.

In brief, this is because I don’t think that any individual investors can earn anywhere near minimum wage by actively investing by themselves. The majority will actually lose money. The research also shows that most fund managers take more in fees than they provide in above-market investment returns.

Again, I recommend that you read all of the following articles to learn more:

Stock Market Investing: Passive vs Active Articles:

Why Passive Investing Is Better Than Active Investing

More Arguments For Passive Investing

How Much Effort Should I Spend Trying To Beat The Market? NONE!

Top 10 Best Performing Shares…And Why We Should Ignore Them

Why You Shouldn’t Listen To Stock Tips!

Podcast: Session 22 – Why Choose Passive Investing?

Quiz: Can You Predict Future Stock Market Performance?

You also need to think about passive and active investing when investing in a small business venture.

Example:

Say you put £5,000 into a small business, and after one year you think that will be worth £10,000. A 100% ROI is impressive, but if you’ve spent 20 hours a week growing that business, then all you’ve effectively done is earn a salary far below minimum wage!

Conclusion: In all forms of investing, think about the impact of active vs passive investing and, if you are actively investing, what your equivalent hourly wage is for your work.

6. Stock Market Investing Vehicles

All of the previous sections of our best long term investing strategy guide have looked at the major investing asset classes of stocks, property and small business. The rest of the guide will focus primarily on stock market investing in the UK.

The first thing we need to consider, and that baffles almost all new investors, is where we will be keeping our money that we are investing.

All of this is unnecessarily complex and there are many layers of mixed terminology.

The best way I can explain it is to compare it to how you save money in a bank. Within HSBC (the company acting as a bank) for example:

The same is true for how you invest into the stock market. The bank is most often replaced by an online broker. The online broker will offer different accounts, each which will have different investment options within.

I personally use SVS securities, which would look similar to our HSBC bank example:

However, you may notice that SVS Securities (the online broker) doesn’t offer regular pension accounts.

Your company pension (if it is a defined contribution scheme), your employer will select a broker who offers “pensions” as one of their accounts. Then you’ll have the option to select from the different types of investments within (usually restricted to certain index funds, mutual funds and ETFs).

When it comes to long term stock market investing there are only really two investment vehicles that most people will need to consider: ISAs and Pensions.

If you are wealthy enough that you’ll need to look beyond these two options (which means you’ll need to be investing more than £55.240 in the 2015/16 tax year), then you should be consulting an independent financial advisor to explore further options.

We recommend that your long term market investments are made in these accounts as they are protected from the tax man more than in regular accounts.

In order of preference, I would suggest that you use the following vehicles to invest your long-term investments:

1. Pension Accounts With An Employer Match (up to your employer match maximum)

Most employers will offer employees an incentive whereby if the employee contributes to their pension, the employer will match their contribution up to a certain predefined limit.

For example, if they employee invests 5% of their salary, the employer might match that contribution by also investing 5%.

This would be 100% ROI in the first year. Then, the impact of compound interest will positively hit this contribution in all the following years. This makes a matched pension contribution almost always the winner from a mathematical viewpoint.

Your money (and employer match) goes into the pension account before you are taxed on this amount. When you retire, you’ll be able to withdraw 25% as a tax-free lump sum withdrawal, and you will pay income tax on any remaining withdrawals (either as a lump sum, or as an annuity) that you make.

You need to make sure you consider your investment options within your pension. For instance, it’s no good if you can only invest in one fund which returns an average of 5% a year and you pay 3% annual fees.

Also, you will need to remember that this money will be tied up until you retire (and at the earliest at the age of 55), and so you could be tying this money up for many years. Once your money goes into this account, you’re not touching it for years!

2. A Stocks & Shares ISA (up to the annual limit – £15,240 in 2015/16 tax year)

The next best option in my opinion is your stocks and shares ISA. In this option you are taxed on your income when you earn it (unlike with the pension), but then you are free to withdraw this cash from your ISA at any point you wish in the future without paying taxes. Additionally, your money grows (both capital growth and income from dividends) tax free.

Whether the ISA or pension (without the match) will be a mathematically better decision will depend on your current income tax band, your income tax band in retirement and the impact of the 25% tax-free withdrawal from the pension.

Mathematically, the pension usually works out as a slightly better investment compared to investing in a stocks & shares ISA.

However, there are many non-quantifiable other factors which make the stocks & shares ISA preferable. This is why we have selected it as the second place to put your money after you have exhausted the employer match. Two of the most important reasons are:

- You have access to your money at any time, and you don’t have to wait until you are 55 to withdraw. This gives you much more freedom over how you want to invest your money over other investments classes in the future (e.g. property or small business).

- You are not subject to changes in government policy. Pension law and policy seems to change on an annual basis, so it’s probably safer to have the money “in your hand” (or at least under your control) today.

For a more thorough analysis of ISAs vs Pensions, I would recommend reading the following:

Stock Market Investing: ISAs & Pensions:

Investing in ISA vs Pensions – Which Is Better?

Maximizing Your Annual ISA Contribution

My ISA Allowance – Should I Invest It All At Once?

The Truth Behind ISA Millionaires – Its Easier Than You Think

3. Pension Accounts Without An Employer Match (up to annual limit – £40,000 less what you invested in step 1)

Finally, after you have maximised the ISA investment limit, you’ll want to head back to your pension account, where you can save up to a maximum of £40,000 in total in the tax year (2015/16 limit).

If you need to look beyond these accounts, you may wish to start investing in VCTs or EISs, but this is “expert level” investing and I would recommend that you speak to a professional before getting involved with these.

Conclusion: Your stock market investments should always been protected from taxation. For most people, the investing order should be:

- pension with match

- S&S ISA

- pension without match

7. What To Invest In?

Excellent, we are seven points into the best long term investing strategy guide and we’ve probably only just reached the section you were waiting for.

If you haven’t read all the sections above, you should go back and read them before you continue. Investing without understanding these first six steps would be like using a chainsaw without any knowledge, experience or guidance – not pretty!!

Once you are happy with your asset class diversification (section 4) and your investment vehicle of choice (section 6), we need to determine what you are actually going to invest in when you say investing in “the stock market”

We have already explained in section 5 that we are fans of passive investing, and hence we recommend that investors make their investments in low-fee market tracking ETFs or index funds.

But what are ETFs and Index Funds, and what are the differences?

The Investopedia definition for an index fund sums it up nicely:

“An Index Fund is a type of mutual fund with a portfolio constructed to match or track the components of a market index, such as the S&P 500 (or FTSE 100). An index fund provides broad market exposure, low operating expenses and low portfolio turnover”.

Essentially, an investment company will take your money and invest it (together with the money of millions of other investors) in every single stock in the market which they are trying to “copy” in the same proportion which it is in that market.

For instance, in the FTSE 100 index fund, the index fund would hold shares such that the index fund performed in the same way as the FTSE 100. The fees on such funds are extremely low (some as low as 0.05% per year).

An ETF, or exchange traded fund, does exactly the same thing. The only difference is that ETF trade like a normal stock on a stock exchange. Where prices are only calculated once a day for index funds, ETF prices change in real time. Therefore, they have higher liquidity (by a matter of ours) and similar fees.

When you are investing in the long term, it doesn’t really matter whether you choose the index fund that tracks the market or an ETF that does the same thing. The only deciding factor may be what you can get within your investment vehicle (some pension may only allow index funds, whereas some S&S ISAs will only allow you to buy ETFs).

Both ETFs and index funds effectively mitigate company risk, credit risk and sector risk, as if you invest in the whole market, you’ll be investing across a variety of company and sectors.

However, when it comes to choosing the markets which you track, then you’ll need to think about market risk (the risk that the whole market performs badly), country risk (risk that the market country’s economy performs badly and impacts returns), political risk (the risk that political instability will unsettle the markets) and foreign exchange risk (the risk that a certain currency may underperform compared to your base currency).

All of these risks can be mitigated by buying a range of different low-fee index tracking funds or ETFs across different regions. For example, in the UK, Vanguard (who are famous for low fee index tracking) offer the following market tracking ETFs, amongst other options:

- VUSA – S&P 500 ETF (0.07%)

- VFEM – Emerging Markets ETF (0.25%)

- VWRL – All-World ETF (0.25%)

- VUKE – FTSE 100 ETF (0.09%)

- VEUR – FTSE Developed Europe ETF (0.12%)

- VJPN – Japan ETF (0.19%)

- VAPX – Asia Pacific exc. Japan ETF (0.22%)

- VHYL – All-World High Dividend ETF (0.29%)

- VNRT – North America ETF (0.10%)

- VERX – Developed Europe exc. UK ETF (0.12%)

- VMID – FTSE 250 ETF (0.10%)

- VEVE – Developed World ETF (0.18%)

By investing in a collection of these (with the highest % in established markets – UK, US, Europe Developed, etc), you can easily mitigate your risks and ensure that you are appropriately diversified.

Conclusion: Spread your investments across a range of low-fee market tracking index funds or ETFs, with the majority applied to major market indices (UK, US, Developed Europe, etc).

8. How To React When Markets Fall?

So, you’ve invested into the stock markets through diversified low-fee market tracking ETFs. Then, soon after, 2008 happens and global markets tumble. How should you react?

This is an easy question and hence a very short section. How should you react? You shouldn’t. You can’t time the market, so don’t even try. Instead, you should stick to your long term plan and be happy that next time you are investing according to your pre-defined investment plan, you’ll be picking up new investments at a bargain price.

Conclusion: Don’t ever try to time the market – it can’t be done!

9. Dollar Cost Averaging

“Dollar Cost Averaging” is the technical term given to spreading out your investments over time. The idea is that if you had £100,000 today in cash, then you wouldn’t want to invest it all at once. Instead, you may want to invest it in four £25,000 chunks in three month increments.

The idea is that this (whilst slightly reducing your mean result due to markets on average going up), will reduce your variance.

You can see this via the following example which shows the returns if we invest £100,000 on day 1, split into two halves or between four quarters under different stock market performance scenarios:

| Invested All On 01/01 | Split Investments into H1 and H2 | Split Investments into Q1, Q2, Q3 and Q4 | |

| Q1: +5%, Q2: +2%, Q3: -10%, Q4: +3% | £99,282 | £95,991 | £97,383 |

| Q1: -5%, Q2: -2%, Q3: +10%, Q4: -3% | £99,337 | £103,019 | £101,901 |

| Q1: -5%, Q2: +2%, Q3: -10%, Q4: +6% | £88,817 | £93,427 | £92,109 |

| Q1: -8%, Q2: -4%, Q3: +4%, Q4: +2% | £93,690 | £99,885 | £100,902 |

| Q1: +8%, Q2: +6%, Q3: -4%, Q4: +2% | £112,099 | £105,009 | £103,954 |

| Q1: +3%, Q2: +2%, Q3: -2%, Q4: +1% | £103,988 | £101,484 | £101,232 |

| AVERAGE | £99,536 | £99,885 | £99,580 |

| STD DEV | £8,805 | £4,768 | £2,991 |

As you can see from this small sample, whilst the averages are fairly similar, the standard deviation is much lower for the dollar cost averaging over the four quarters compared to over two halves or one lump sum.

You’ll need to find a line between lumping it all in at once, and investing too little at a time (especially when there are per trade transactional fees to pay for buying into an ETF) over too long of a time period.

However, this is a judgement call and there isn’t really a right answer.

Conclusion: If you have a lump sum to invest, spread your investments out over time in order to reduce the variance in your returns.

10. Mixing Investments For Short Term Goals / Emergency Fund

Finally, the last point I want to address in this guide is to revisit the idea of cash being the only good liquid investment for your short-term goals and/or emergency fund.

Example

Let’s say that you have £50k in total investible cash. You are saving for a house deposit of £30k in three years’ time (when you feel you’ll be personally and sociably settled to buy) and you want to keep 6 months’ expenses as an emergency fund, which is another £10k.

Now, the standard guidance would state that your £30k and £10k are for short term goals and so should not be invested in the markets. Therefore, you can put the £10k in the markets. Not a terrible answer. But, in my opinion, it’s also not optimal.

Let’s say that you instead put £48k into the market tracking ETFs that can be liquidated at a 3 days’ notice (the time it takes for your broker to send you the funds once you have sold the investment which you can do instantly) and you keep £2k aside for true emergencies that may need paying within the next 3 days. For all scenarios, we’ll assume that you can earn 1% after tax on your cash.

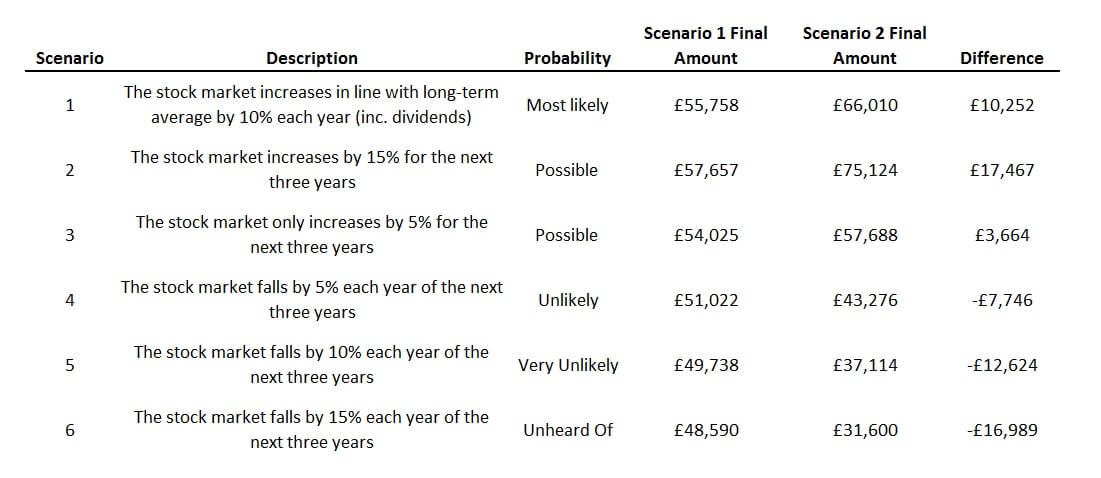

Based on a few scenarios, your results would be as follows:

So, running down these scenarios:

1 – This is the most likely scenario. In the FTSE 250 since 1986 until 2015 (26 different 3 year periods) fell between 5% and 15% growth each year on average over those 3 years on 14 of the 26 occasions. In this scenario, if the emergency was required, the money could be withdrawn to pay for the emergency, and the investor would be in a much better position after 3 years than if they had been more prudent and kept it all in cash.

2 or 3 – These scenarios are both possible, with 4 of the 26 “3 year periods” showing annual growth of over 15% per year, and 3 of the 26 showing annual growth of between 0% and 5%. Effectively, in any period with over 0% annual growth, the market investing strategy would be better, and the figures show that out of the 26 occasions, only 5 occasions out of 26 (less than 20% of the time) was the stock market performance over 3 years negative.

4 – Of those 4 occasions, the market has fallen twice near the scenario 4 example, falling by 4% per year between 2002 and 2004 and 6% per year between 2008 and 2010. And, what happened in this scenario. Well, the stock market investor was clearly worse off than the cash hoarder, but they still had £43k to play with at the end of the period of 5% per annum falls, which covers the house purchase and the emergency fund.

5 – On the other 2 occasions with stock market falls over the 3 year period, the FTSE 250 fell by 12% per year from 2001 to 2003 and by 11% per year from 2007 to 2009. This is similar to scenario 5. This is very unlikely to happen, but in the two instances that it has (around 7.5% of the time) the investor would be left with £37,114. This is still enough for most emergencies, together with the house purchase.

6 – A fall of 15% per year over three years has never happened before, but it theoretically could. However, even in this disaster scenario, the investor still has the £30k for the house, although this wouldn’t be the best idea to use without a supporting emergency fund. The key to think here though is that if global markets fell by 15% per year for three years, then there is no way that house prices would remain at the same level. Hence, the investor may only need £20k for the same deposit on the same house.

I run all of these scenarios to tell you that you need to think about your own personal situation and your risk appetite. On average, if you follow the standard advice in the above situation, you’d be losing out on over £10,000 gains in three years. You can’t afford to do that all your life if you are striving to push towards financial freedom!

Conclusion: If you have a lump sum to invest, spread your investments out over time in order to reduce the variance in your returns.

The Best Long Term Investing Strategy Guide – Conclusion

I hope that our best long term investing strategy guide explains in some detail the process behind long-term stock market investing and how to do it passively and easily.

If you are investing as a tool for obtaining financial freedom, then why not join the Moneystepper Savings Challenge: a community of participants working together to achieve their financial dreams!

![]()

You hit on some good ones. A few of the most important are about paying down debt. Great example on how your net worth can change whether you decide to pay down debt or not. But also, I like the concept of “paying yourself first”. “The Richest Man in Babylon” does a great job discussing this one. Give yourself a little money to save or invest and use the rest to pay down debt. Set your amounts before hand.

I also like the distinction between investing and investing for a salary. Another important one is investing vs. speculating. You have to define what your goals are and how you go about achieving it in the markets . . . then stay disciplined. Otherwise, you’ll be at the mercy of your emotions.

Good write up!

-DP

These are what I felt that hindered from investing. I am glad that I overcame these challenges earlier because in investing time aside from doing our research is really a factor to how much I’d earn.

Congrats. You’ve covered a lot of ground there for a single blog post.

I pretty much agree with you apart from a couple of points:

– non-matched pensions are better than ISAs, though that’s easy for me to say as I’m 55 already; younger people will obviously not be keen on having their money locked away for a long time

– pound cost averaging into the stock market doesn’t really work in the long-run; because the stock market mostly goes up, you’re better off investing money as soon as you have it

Hi Mike,

Thank you for your comments – I agree with both but with important caveats:

1) Non-matched pensions have the advantage of having 25% tax free. However, as you say, they have the downside of locking your money away for a fixed period of time, but also a comparative restriction on what you can invest your money in (for example, you cannot invest in residential buy-to-let property directly through your pension.

2) Whilst putting all the money in today will on average provide better returns, dollar-cost averaging helps you overcome the significant variance in your investment. This is particularly key for people who have a large amount to invest (maybe from a large bonus, inheritance or something similar) and don’t want to risk it all at one arbitrary time for the investment.

Again, both of your points are accurate, but the reasons above are why we suggest ISAs over non-matched pensions and dollar/pound cost averaging for investors.

Thanks again.