It’s time to make your financial dreams a reality. Join the Moneystepper Savings Challenge: a community of ambitious people, all achieving their goals and dreams. We’re becoming financially free, together!

I want to invite you to join the Moneystepper Savings Challenge community on our quest to achieve financial freedom.

Money is the root of all…happiness?!

Time to be controversial for a second. I’m sure you know the phrase “money is the root of all evil”. Well, in some cases, money can be the root of some evil.

There are the Bernie Madoff’s of this world: the former chairman of NASDAQ and fraudulent investment adviser who swindled millions out of investors. And, there are many more like him.

Their crimes all come from the desire for money.

However, these are exceptions to the rule.

Money itself isn’t a root of evil. Money is simply an amplifier.

- If you are already greedy, money will make you greedier.

- If you are already nasty, money will make you nastier.

- If you are already selfish, money will make you even more selfish.

However, and much more importantly, money is also an amplifier of good.

- If you are already generous, money will make you more generous.

- If you are already charitable, money will make you more charitable.

- If you are already happy, money will make you happier.

Just think about Bill Gates. No one can deny that he is wealthy – for a long time the wealthiest man in the world. Does this wealth make him a bad person? Does this wealth make him evil?

Bill Gates and his wife Melinda have so far given away $28 billion, yes billion, via their charitable foundation and more than $8 billion of it to improve global health. Here is one of his missions in the foundation – has money made him evil?

And what about Warren Buffett? He has already donated at least $9.5 billion of his $46 billion fortune. Would you like to give away 20% of everything you own tomorrow? He’s also pledged $30 billion to the Gates Foundation. What’s more, he has pledged to give away at least 99% of his fortune. Does that make him a bad person?

What about Mark Zuckerburg and his wife. In 2012, aged only 28, he gave $500 million to charities.

Another thing about money is that it’s a necessity and a requirement for you to achieve whatever it is that you want.

People often cite that money doesn’t bring happiness, or that they don’t need money to do what they want.

However, what about if you wanted to retire at 50 instead of 65 in order to build schools for underprivileged children? Or, what about if you want to quit work to help your children and look after your grandchildren? Or look after an elderly relative?

All of these goals would be commendable. But, what do all of these goals have in common? The requirement to have sufficient wealth to spend your time following your calling in life, rather than rocking up to your desk every morning to get paid so that you can pay your bills!

People Aren’t Retiring With Freedom

Information from the 2012 ONS survey on retiree income.

That statistic is bad enough by itself, isn’t it?

However, when you break it down, it becomes even worse. Of that £11,321 net income, an equivalent of:

- £5,815 comes from the state pension

- £1,336 comes from other state handouts (benefits and support)

- £127 comes from employment income (people still working)

Only £4,090 of this amount comes from private pensions and investment income.

Assuming that this median person is happy to rely on the state pension staying at this level and the amount of government handouts staying as high (I wouldn’t be), then let’s think what this £11,321 will get you.

It is estimated that the average person spends £3,329 on essential bills every year (gas, electricity, phone, TV and council tax).

I think we’ll also have to assume that this median person also doesn’t have a paid for home. We can estimate another £1,000 a year on mortgage payments (I think this is a gross under-estimate).

Annual average expenditure (as per 2013 data) on food and drink was £3,458, clothing was another £1,175, and healthcare £322.

Therefore, just to put a roof over your head, keep it heated and keep yourself fed, clothed and watered, the annual median expenditure is £9,284.

This leaves our median retiree with a whopping £2,000 a year (or £40 a week) to live the life they dreamed of in retirement!!

These average retirees certainly aren’t achieving what they set out to do in retirement based on these figures, and I’m guessing that you don’t want to be this “median” example.

In the Moneystepper Savings Challenge, our participants are working to not be part of this statistic. Every participant sets financial goals every year to ensure that they will retire with the amount of money they want to. They also set a “higher goal”. This is a much longer term dream, which will only be possible if they are financially free at that time.

We aren’t working together in the challenge to save money, to increase our wealth or to “get rich”. It’s bigger than that. We want to achieve our big goals in life. And, we need to make sure our finances are managed in such a way to allow that.

Moneystepper’s Story

If you’ve ever signed up to the newsletter at moneystepper.com, you would have received our free PDF guide of the 10 things I have learned about money from running moneystepper:

The guide concludes that the single most important factor in improving your finances is consistently tracking your finances and taking action as a result.

Let me share with you my own story. It might sound familiar to you!

For years, I thought I was “good with money”. However, despite working hard, despite having a good job and despite being frugal in my spending, my net worth (the principle measure of wealth) never seemed to change.

Three years ago, I started the Moneystepper Savings Challenge. Since I did, my net worth has increased by an average of 60% over the past three years. I put all of this down to the fact that I monitored my personal finances like a business.

I set my “financial dream” and my two annual financial goals, and I recorded my progress against them each month. More importantly still, I published my results on Moneystepper for the community to see. This level of accountability really gave me the push I needed to achieve what I wanted to financially.

It Helped Me, And I Promise That It Will Help You

The Moneystepper Savings Challenge took me from a relatively static financial position to improving my net worth by around 60% each year. This is my performance.

Yours may not be the same. However, whilst we must warn you that you may not achieve as much as I have, it’s equally important for you to know that you might achieve much, much more.

Just take a look at our results from 2015:

The average Moneystepper Savings Challenge participant set a goal to improve their net worth in the year by 25%. The actual average improvement was 40%. Given that global stock markets fell by over 9%, this is a remarkable achievement.

The biggest over-performer set an annual goal of 10% net worth improvement and actually achieved a mind-blowing 118% improvement.

What about the failures? It’s only fair to show you both ends of the challenge. Well, the worst performance in 2015 was a participant who set their goal at 30% and actually achieved 18.7%. Given the fall in global stock markets, and the fact that this participants had several financial emergencies in the year, this shouldn’t be scoffed at!

The performance for the Savings Rate goal (the amount saved as a percentage of their net income) was equally impressive. The average participant aimed to achieve a Savings Rate of 37%. The actual average Savings Rate achieved was 50%. That’s right – the average participant in the challenge saved/invested half of their income every single month.

The highest savings rate achieved was 77%. The lowest was 16%. When the standard advice is that people should try to save 10% of their net income, it’s easy to see that the Moneystepper Savings Challenge participants are over-achievers. And you could be an over-achiever too!

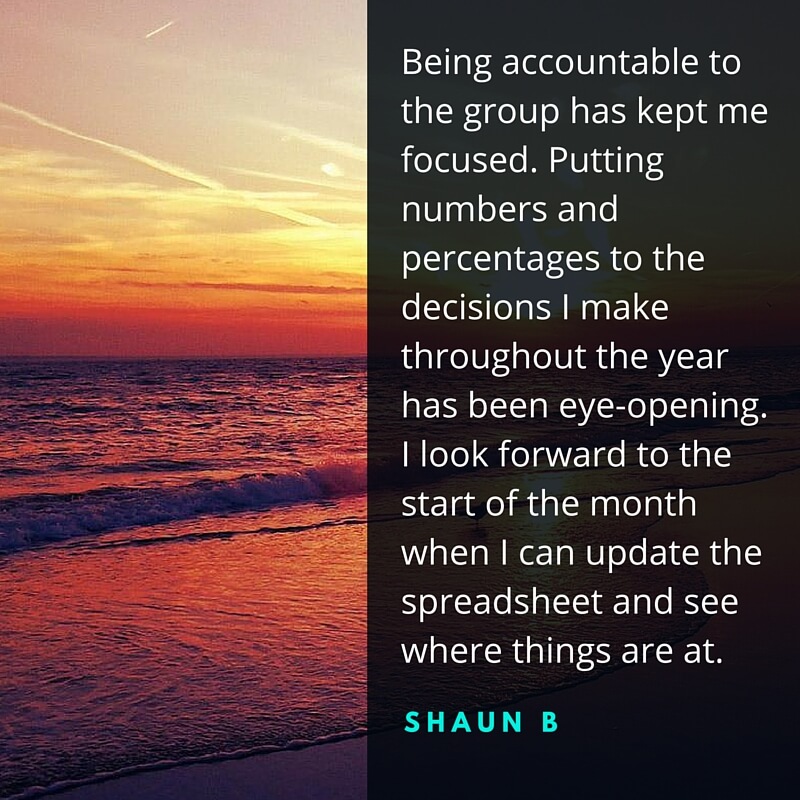

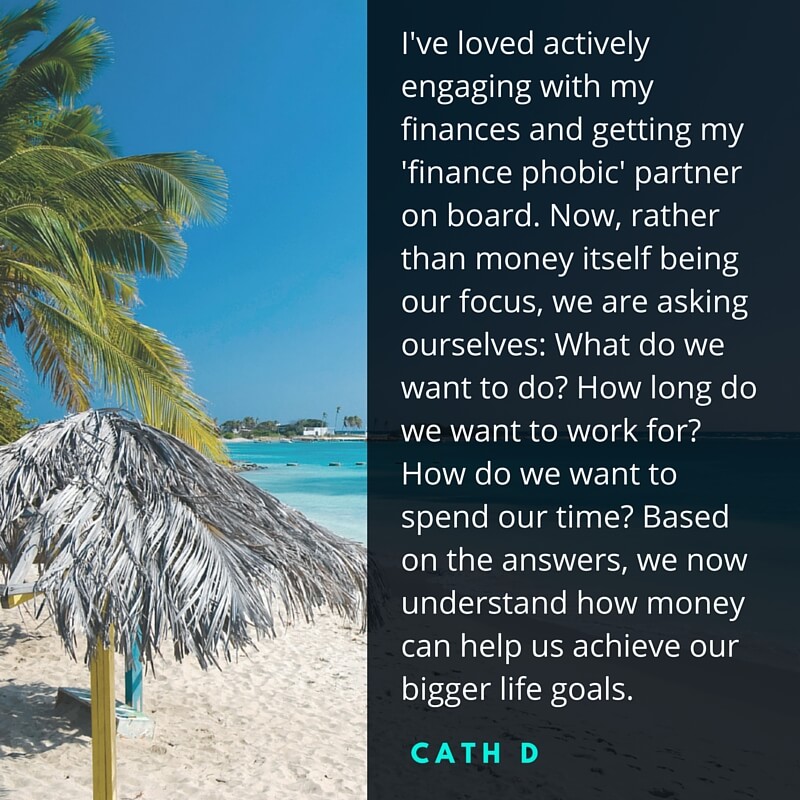

What The Participants Have To Say…

Don’t just look at the figures. Listen to what the current challenge members have to say:

Download The Tracking Template

Do you want to see what all the fuss is about?

Download the Moneystepper Savings Challenge Tracking Template by clicking on the image below.

It’s completely free and will help you set your goals, track your net worth, set your budget and analyse your performance each month:

![]()

And that’s just the start. It also helps you analyse variances in your spending, set and achieve additional financial and non-financial goals, map out your repayment of debts, and understand the awesome power of compound interest.

So, download the Savings Challenge Tracking Template and feel free to use it however you wish. However, make sure that you read and follow the guidance in the template. This will ensure that you get as much value as possible.

Join The Challenge Today

Budgeting is key to achieving financial success. As is tracking your financial goals and analysing your progress against those goals.

However, the real secrets of success are much deeper than just these steps, and joining the Moneystepper Savings Challenge will provide you with much more, including:

- Accountability

- Information

- Comparability

- Education

- Commitment

- Support

- Community

Engaging with, and being accountable to, a community of people who have similar financial objectives has been proven to act as a powerful catalyst on the journey to financial success.

If you join the Moneystepper Savings Challenge, you’ll submit your results from the Tracking Template to us every single month. This is done via a button in the template and only percentage information is shared – you’re personal financial data will never be visible by anyone except yourself.

Participants have commented that this accountability alone has saved them a good chunk of cash every month. Each time a spending decision comes up, they suddenly remember their financial dream and that they’ll have to submit a worse result at the end of the month and this encourages them to make the right financial decision.

Also, the Moneystepper Savings Challenge provides a mountain of education and support. This comes directly from Moneystepper in the form of the Q&A podcast, where you can have any of your questions directly answered, and via the monthly commentary on the results.

You can also constantly engage with other people who are in a similar financial position to yourself and who have similar financial goals. You’ll be included in private Facebook groups where you can ask questions of your fellow participants, and you’ll also see people facing situations which you are in, and often some you didn’t even realise you were facing yourself.

Finally, being involved with a community of people who are trying to achieve the same objective of financial freedom is invaluable.

Take an equivalent example. Say that at the end of next year, you were going to run a marathon. You have two options:

- You can “go it alone”. You will run the race by yourself. You will train by yourself. You won’t educate yourself on good running techniques or good training methods.

- You can join others. You sign up to a running club of people who will be running the same marathon. Some people will be with you running for the first time. Others will be on their third or fourth marathon. You’ll benefit from their experience. You can learn from their mistakes and copy the good practices.

Given the two options, it’s clear which is more likely to lead to you achieving your goal of reaching the marathon finish line in a time that you are happy with. You don’t have to go it alone.

Exactly the same is true for reaching the financial freedom finish line in a time that you are happy with. You don’t have to go it alone.

So, come and join an army of ambitious and determined people, all focussed on reaching financial freedom and being able to carry out their calling in life!

****************************

***************************

If you have any questions or reservations about the challenge (including confidentially and our disclaimers), you can either refer to our Moneystepper Savings Challenge FAQs, or contact us at moneystepper@gmail.com.

I look forward to welcoming you aboard the Moneystepper Savings Challenge and achieving our financial dreams together!

Sounds like a cool challenge! Anything to get people to save more is a good thing.

Yes DC!! First comment, first on board! Let’s bust 2015’s *** together! Let’s do this…

I am coming with you. My 2015 will be better than this year. I am challenged and will do what it takes! Ready to face 2015!

Welcome on board Jayson – really pleased to have you in the group for the journey. Can’t wait to learn from you and complete the 2015 savings challenge together!

I’m in! We are defiantly tightening our budget in this upcoming year. I’m determined to pay off the rest of our debts by the end of 2015.

AND ANOTHER!! Very pleased to have you on board for the 2015 savings challenge Sarah. We’ll see the back of those pesky debts in no time at all!!

I have to give it some thought to make sure I’m 100% committed. I think for me the frustrating things is having variable income and one that’s been not very good since July. So sometimes my savings rate for some months has been 0%. 🙁 But I will think about it, and I’ll post this on my challenge blog and fb page so people can see there is a way to continue with savings challenges!

Tonya – I understand your concerns and I’m in exactly the same boat – I’ll release a podcast episode shortly to explain my goals and my current position. Effectively, my personal savings challenge will be a little different to the last two years as I went self-employed in September and so my income will greatly vary as well.

The trick with the savings challenge is that the goal is annual, but measured monthly. So, just as a random example, if I set my savings goal at 25% for the year, and have the following results, I will still be on course after 3 months for my savings rate:

Jan: Income – $0 ; Expenses – $1,500 ; Savings – ($1,500)

Feb: Income – $0 ; Expenses – $1,500 ; Savings – ($1,500)

Mar: Income – $6,000 ; Expenses – $1,500 ; Savings ; Savings – $4,500

So, year to date in March would be…

Income – $6,000 ; Savings – $1,500

…and therefore I would be on course for the annual goal.

In the results (if this helps), we can add a one-line comment to explain why we are above/below our goal in any one month. I think this would be valuable for everyone in the savings challenge as then they can see that a lot of other people were behind schedule for the same reason as them.

What do you think? Have I convinced you yet? 🙂

Looks very motivating for savers! My current challenge is coming to an end and it would be nice to start a new one for 2015!

I would love for you to join us in this new savings challenge, Adam. The more, the merrier!!

I think this is a great idea. I am not sure I am 100% ready to join, but I do have my own goals and things I want to make happen in 2015.

Kim, thanks for your comment. I would absolutely love for you to join. Is there anything we can do in the savings challenge community to convince you to come along for the ride?

We are in! It will take me a little time to figure out the exact percentages. Mr. Maroon and I are working on finalizing our strategy for 2015, so its coming soon!

Welcome aboard (Mr &) Mrs. Maroon!! If you need any help with understanding the spreadsheet or your percentages, don’t hesitate to send me an email. Looking forward to seeing your final strategy and goals!

I got it all tallied and info is submitted through the form. Thought I’d let you know that you should double check some of your summation cells in the spreadsheet you provided…

Mrs. Maroon – thank you for signing up. I’ve received your submissions!

I checked that spreadsheet so many times, but there’s always something isn’t there!! D’oh!

Thanks so much for letting me know. I’ve updated the spreadsheet for download and contacted everyone who I think has already downloaded and used the spreadsheet.

Hi,

I will be on board, just got to do some sums over the next few days to see what is achievable. Mmmmmm sums

Mr Z

Mr. Zombie – good to have you on board!! 🙂

What a great couple of days you’ve got ahead – everyone loves sums!!

Sounds like a great idea. I’m not sure how applicable it would be to us. My husband is self-employed, so we can’t predict our income from month to month. Also, we’re focused upon debt-reduction rather than savings. I’ll think about it though! Making a commitment and being accountable within a supportive community sounds very effective.

PD – thank you for your comment. I would urge you to look at this again, as we have made the 2015 savings challenge as relevant as we can to everyone, and I think that it would actually be perfect for you.

Firstly, regarding your husband’s variable income, please see my reply to Tonya’s comment. Effectively, the savings rate is a year-to-date running total and therefore it doesn’t matter if income is variable month-to-month. I’m personally in exactly the same boat.

Secondly, for debt-reduction vs savings, we calculate the savings in the “savings-rate” as being all money placed towards savings & investments, but it also includes any payments made to pay down debt above the interest accrued. This insures that people trying to pay down their debt are not “punished” in their savings rate because they are focusing on paying down debt – after all, this is effectively saving at a fixed rate equal to your loan interest!

I really hope you come along on the 2015 savings challenge journey with us – I really think you’ll find it beneficial!

I’m in… but I’ll submit my numbers at another time after I’ve had a chance to play with the template. I’ll admit I don’t quite know how my % will work, because there is a good likelihood I will start the year with a slightly negative net worth, or just ever so positive a number. That means to get to my $29k increase in net worth (say I started with +$500) would be a 5800% increase. Which is hugely misleading, and only gets worse if I end 2014 with only +$200 (145 000%) 🙂 I’ll figure something out I guess. Or I win the award for “the smallest starting point that inflates all her numbers” award 😉

make that second percentage 14,500%… I got a little “zero-happy”

Very good point Alicia. This may look a little silly at first, but here is how the results will work. Your monthly result which is published on moneystepper for each goal will primarily focus on your performance against whatever goal you set.

Let me explain through an example.

Say you start with (as you suggest) $500 and your goal is $29,000. Then your goal is indeed an annual growth of 5,800%. This is the figure you submit for your annual goal!

After three months, for example, your YTD goal would be (3/12 x 5800% = ) 1,449%.

Say your real net worth at the end of March was $7,500. Then, your actual improvement would have been 1,500% (which will show in the spreadsheet) and this is the figure you will submit.

These percentages look a little crazy, but the important thing is that your “result” which is shown on moneystepper and that we will focus on will be that you are 3.5% (1500/1449) above your YTD target.

Therefore, this would be the same as someone who has $1m starting point if they were 3.5% above their target.

Does this make sense?

This is totally awesome- accountability and community- recipe for success!

“Totally awesome”! That is exactly the language we want in the 2015 savings challenge community! Welcome on board Stefanie – YOU are totally awesome!! 🙂

This is a cool idea, and it will spark others to increase savings. The competition will help fuel the challenge.

Its not technically designed to be a competition against others, but rather just a competition against yourself.

However, if you want to compete against other people, there’s nothing stopping you! 😉

Do you think you’ll get involved yourself EL?

Great concept! Count me in. I’ve already added my values into the form. I hope you get a good response!

Awesome – submission received! Welcome to the 2015 money saving challenge Thomas, its a pleasure to have you on board!!

Tons of detail and great stuff on the spreadsheet. It will even take all your information and put it into three different graphs so you can see it visually.

Thanks for the motivation. Great idea. I’m in!

Thanks for the compliments Joseph – I’m glad you like them. I hope that this can help you and everyone else who signs up to our 2015 savings challenge!!

Good to have you in the community!

This is awesome, Moneystepper! I will definitely consider this to see if it works into our 2015 goal. Our main goal is to dump debt, but I suppose in the end that would reflect in our net worth, right?

Exactly right Laurie! I would imagine that your goal of reducing your debt is actually a sub-goal of improving your net wealth. That is the eventual goal. However, I would argue that its better to focus on the net wealth because of things like matched retirement contributions. For example, if your goal was only to pay down your debt, then you would place all your earnings you could against debt. However, as our post on pay down debt vs saving for retirement shows, its much more beneficial for your net wealth to match any employer matched pensions before paying down standard consumer debt (student loans, car loans, credit cards, etc).

As I’ve said in other comments, the Savings Rate % is also designed to include debt repayments over and above interest paid so paying down your debt is “rewarded” in your savings rate.

It would be great to have you aboard Laurie!

OK I’m in, let’s do this!

Yes!! Welcome to the 2015 Savings Challenge Emily! Let’s not only do this; let’s DESTROY this!! 😉

I’m in! Hopefully this will push me closer to my ultimate goal of saving 50% of my gross income!

Awesome. Welcome to the money saving challenge Ginger! Just a point to note if you are using the spreadsheet provided. This calculated savings rate based on net income, so you may want to amend your savings goal % when you submit it based on that…

I want to try this savings challenge! I’m going to download your spreadsheet and thanks a lot for this!

Awesome Clarisse!! Looking forward to having you on board with the 2015 Savings Challenge and working together with you in 2015 to achieve our financial goals together!

Thanks for stopping by my blog – you can count me in this challenge! I don’t currently have a goal for my Net Worth but I look at setting one up for this challenge!

Awesome Weenie!! Welcome to the Savings Challenge! Welcome to the Savings Challenge!Can’t wait for you to jump on board and for us to start working towards our financial goals together.

I’m in! Is there a list of participants-to-date posted anywhere?

Cecilia – welcome aboard the 2015 savings challenge!! Great to have you here!

There isn’t a list to date. I will publish the first list in very early January once I have grouped the participants, etc etc…

I’m in MoneyStepper. Really looking forward to this challenge getting underway.

Goodluck throughout 2015,

Mr. Captain Cash

Great to have you involved MCC!! Good luck to you too!

Thanks for the challenge, it’s a great idea. I planning to join very soon, just getting my numbers and goals together so that I can submit the form 🙂

Great Nicola – looking forward to having you on board for the 2015 money savings challenge! Hope you had a great Christmas and that you’re raring to go for 2015!! 🙂

I’d love to do this! Accountability is really going to help me reach my financial goals in 2015. Count me in!

Nice one Chonce! We are honoured to have you on board the savings challenge. Don’t forget to submit your annual goals using the form above…

Thanks for opening the challenge to everyone I have just submitted my goals after much thought and am looking forward to tracking my progress and the progress of all participants.

You are more than welcome Lynx!! As far any money challenge is concerned, the more the merrier in my opinion!!

Awesome stuff!! Welcome to the Savings Challenge Lynx. Received your goals and looking forward to working towards achieving our goals together in 2015.

This is a great idea! I am not in need to join because I have surpassed this stage many years ago and have begun to build my way to wealth. It still amazes me how much a person can accomplish when they set goals and pursue financial freedom.

Hi Michael, and thanks for your comment.

I’m a little surprised by your statement that you are “not in need to join”. There are people in the challenge with a net worth of over £1m.

Surely progressing your net wealth and increasing your savings rate is a reasonable goal however wealthy you are. I’m pretty sure its probably still on Bill Gates’ list of New Year Goals!! 🙂

Count me in! I need something to hold me accountable. I hope I wasn’t too late.

Not at all Vawt! Absolutely chuffed to have you on board. I’ve added you to the Moneystepper Savings Challenge list on twitter and get yourself involved in the facebook group as well:

https://www.facebook.com/groups/496863293787199/

That also goes for anyone who has joined the challenge…

What a great challenge. My goal is to save half my income in 2015. I hope this will help me reach my goal

What an amazing goal Denise! If you are an average income earner (UK), have exactly £0 net worth, and set a savings rate of 50% of net income, and earn 10% return per year on your funds, you’ll be a GBP millionaire (over $1.5m) in 22 years just from this saving alone! That’s pretty cool in my opinion!

Its a pleasure to have you involved in the challenge and I look forward to getting to know you better in the next 12 months!

This may be a silly question but I am trying to get my head around the spreadsheet. How am I supposed to track current accounts, credit cards, and expenses. These things span over months. My initial thought is that a current account should not be on the net wealth tab, and all costs that I incur should be recorded on the savings tab in the month I make the purchase, except work expenses. However this means that any months will not balance.

thoughts ?

D

Hey Dan,

Thanks for your question. The way I do it is to record all things like credit cards and current account on the net worth tab (balance sheet) as these are the amounts you owe at the end of the month.

Then, all expenses/costs that are incurred are noted on the savings tab (P&L) in the month in which they incur. Therefore, in theory, if you have accounted for everything in your P&L in one month, your net worth should increase/decrease by this amount compared to the month before.

Does that make sense? If you want anymore help, send me an email and we can chat over specifics.

Thanks again for getting involved!

That seems to make sense, I’ll see how it works as I work through the year. Thanks

Love the accountability of the group idea, be interested to see how it all works out! Thanks for the link.

You run this every year right? If yes, will be keen to join in 2016.. the one area that will hold me back is overseas European holidays ;), not always a bad thing haha

Great initiative as well good on you Graham :)!

Thanks for your comment Jef. We do indeed run this “every year”, but it isn’t just an annual challenge – it’s always ongoing.

In fact, as we highlight in the post above, it’s always better to get involved with the Moneystepper Savings Challenge today rather than waiting for the start of next year.

Also, going to Europe on holiday is not banned in the challenge! 😉

Instead, it’s very much actively encouraged. The challenge is all about understanding what you need to control and cut back on elsewhere that you don’t care about. This way, your holiday to Europe (which will stay in your memory your whole life) won’t destroy your progress with your net worth and savings rate.

Would love to have you involved Jef. If you have any other questions, fire me an email and we can have a chat about the challenge.

Cheers, Graham.

I am in, looking forward to the challenge.

Great to have you involved in the Moneystepper Savings Challenge Esther! Good luck!! 🙂